Regulatory initiatives

The Financial Services Commission (FSC) under the Banking Act grants a preliminary license to operate Internet-Only (neobanks) banks in South Korea. The FSC grants the banking license on three significant grounds:

- Innovativeness: To create a new wave of competitiveness in the banking sector

- Inclusiveness: To help financial customers enjoy numerous benefits such as banking at lower transaction cost, convenient banking services, ease of access to loans

- Stability: To promote the creation of jobs in IT, banking, and fintech domains

The primary benefit is that non-banking financial companies (NBFCs) can hold up to 34% stake in the neobank.

Snapshot of South Korea’s neobanks

Table 1: Profile for South Korea’s neobanks

| Name | Founding Year | CEO |

| Kay (K) bank | 2015 | Shim Sung-Hoon |

| Kakao bank | 2016 | Alex Ryu |

| Toss | 2015 | Seunggun Lee |

Note: The annual revenue is not stated as it is an undisclosed amount since the banks are privately held

Table 2: Learning list of South Korea’s neobanks funding capital

| Name | Toss |

| Total funds raised | US $434.2 Million |

| Series A | US $4.5 Million (July 2015) |

| Series B | US $23.7 Million (April 2016) |

| Series C | US $48 Million (March 2017) |

| Series D | US $40 Million (June 2018) |

| Series E | US $80 Million (Dec 2018) |

| Series F | US $64 Million (Aug 2019) |

| Secondary Market | (Nov 2019) |

| Series F | (Feb 2020) |

| Venture Round | (Aug 2020) |

| Series G | US $173 Million (Aug 2020) |

In-depth neobank analysis on the 5-building block framework

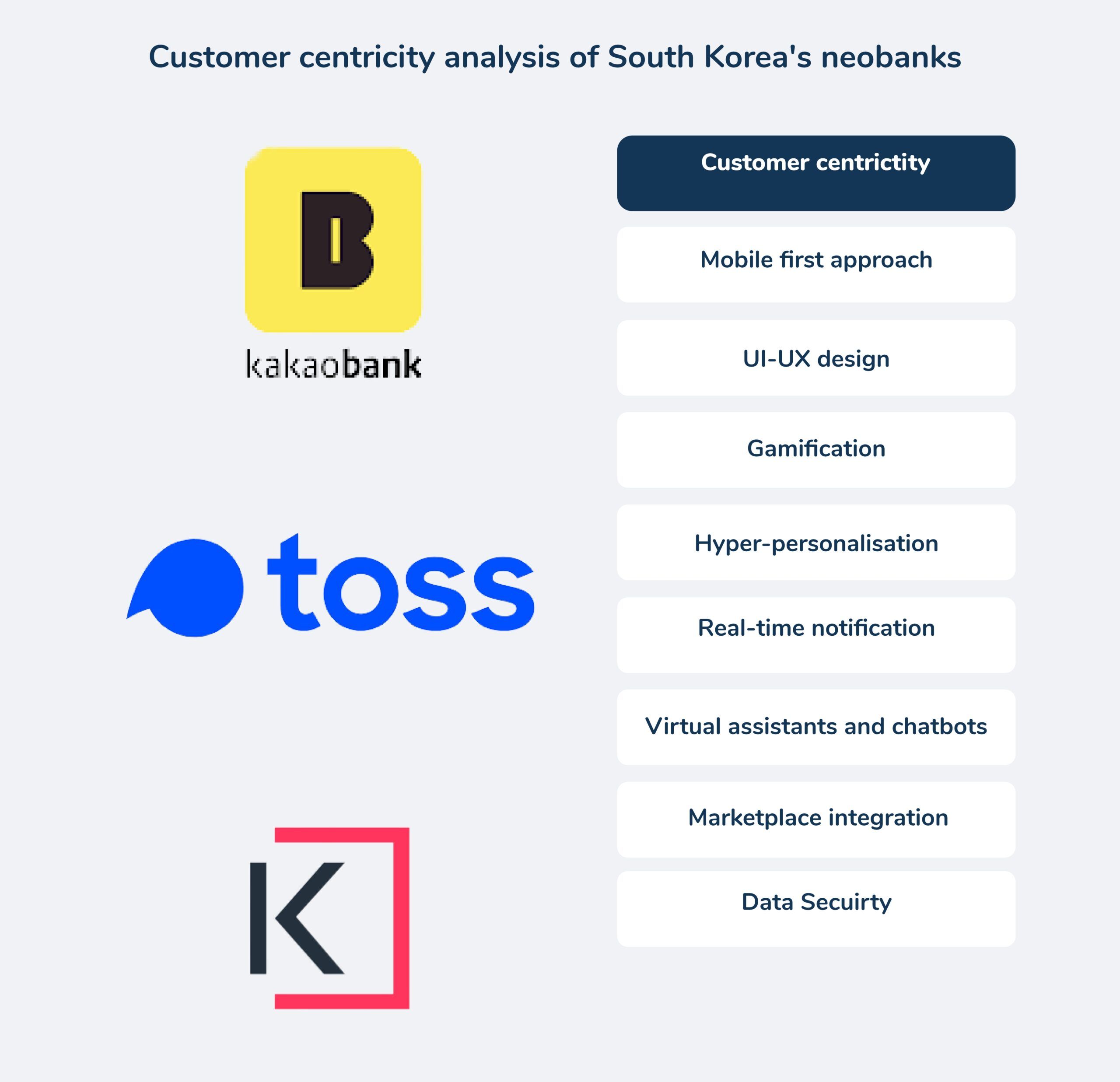

Customer Centricity

- 100% of the neobanks in South Korea showcase a mobile-first approach.

- Kakao Bank and Toss offer hyper-personalised money management tools.

Figure 1: South Koreas’ neobanks fulfil all customer centricity parameters

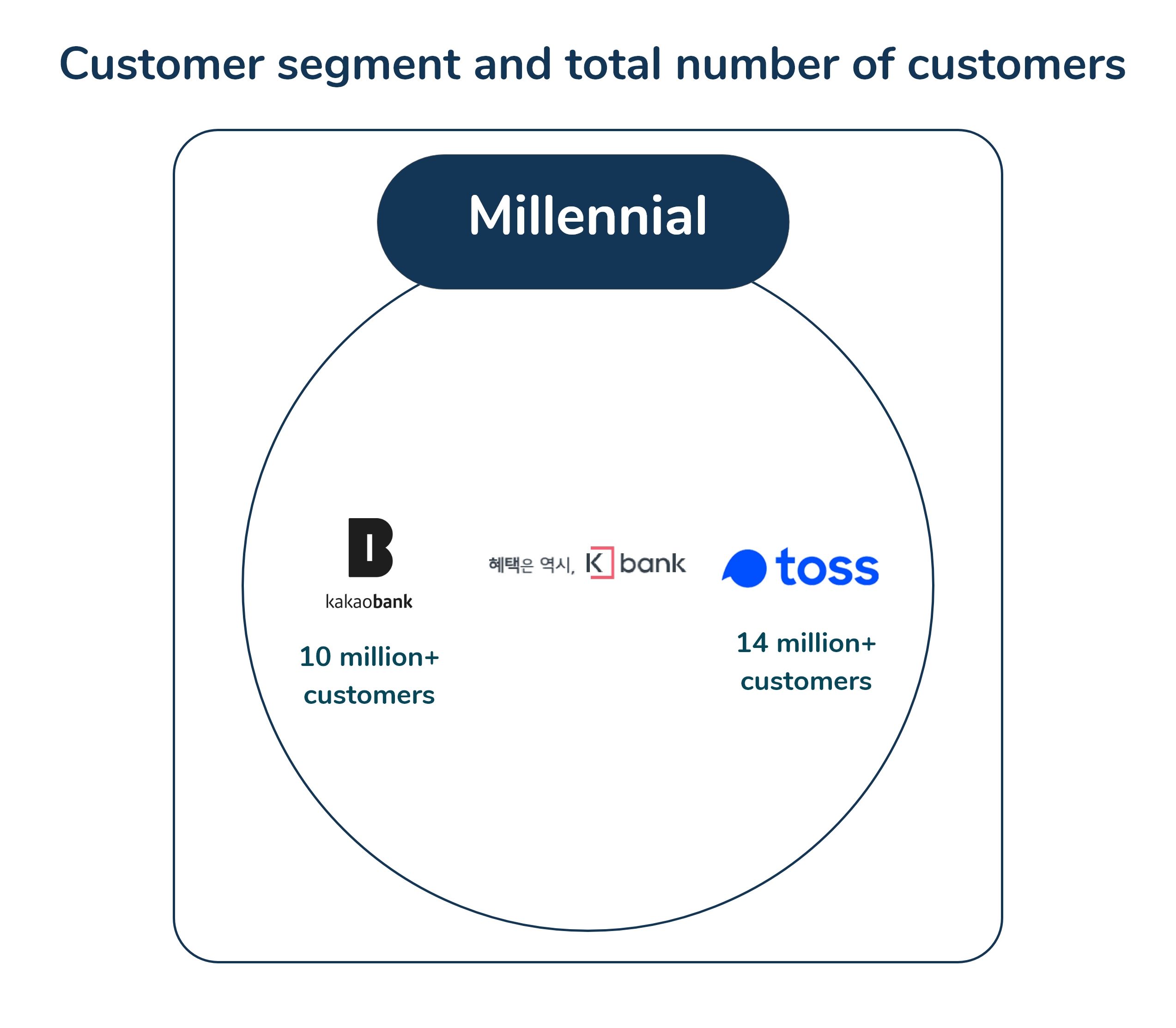

Customer Reach

- All 3 neobanks in South Korea are geared towards the Millennial and Gen Z population.

- Toss serves approximately 1/4th of the entire population of South Korea.

Figure 2: Representation of each neobanks’ customer reach

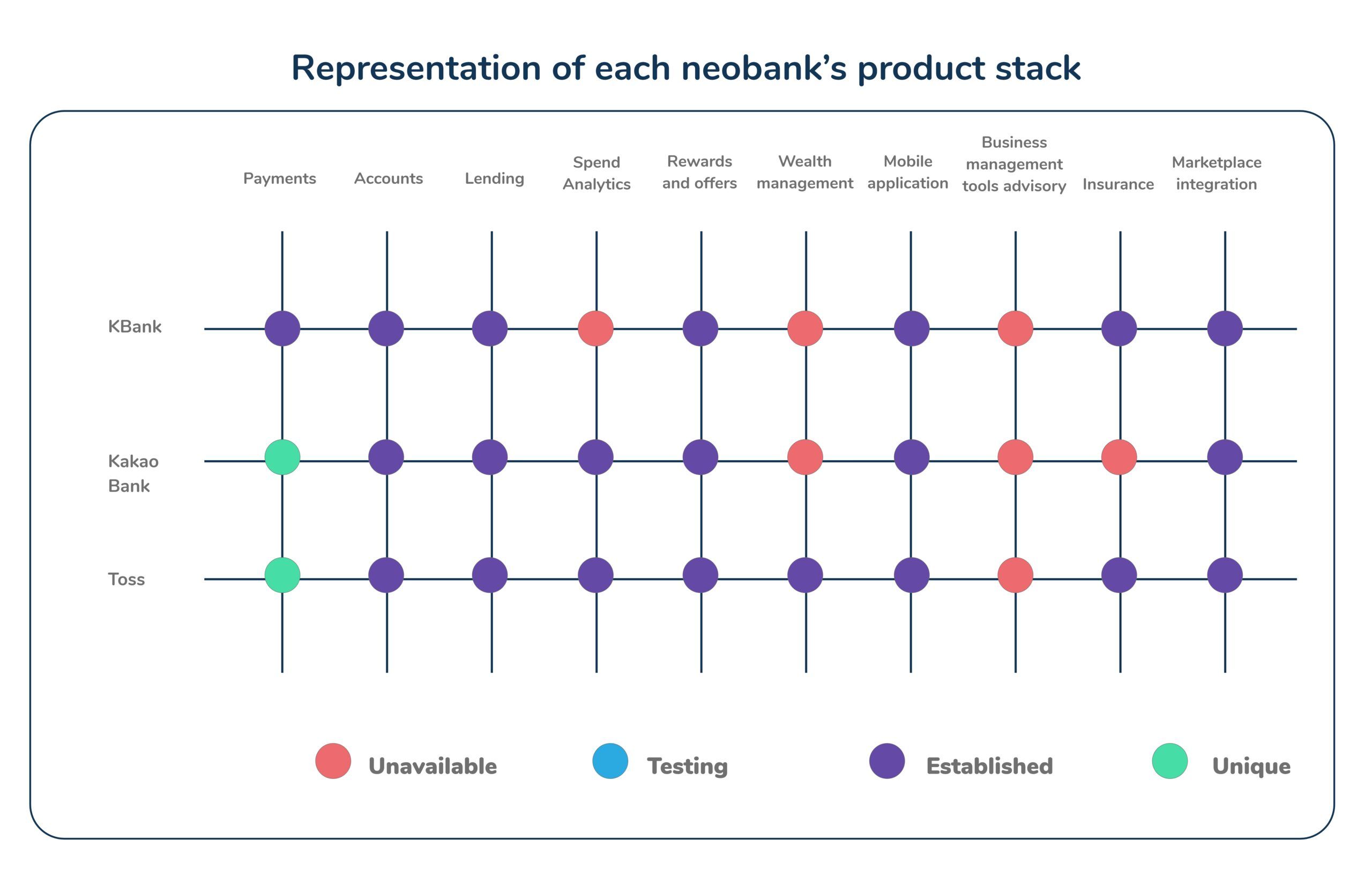

Product Stack

- South Korean neobanks have 70% or more products catering to their customer journeys.

- Kakao Bank and Toss have unique payment options such as split payments and recurring payments.

Methodology

Each virtual bank product stack is a representation of 4 key parameters across 10 product types:

- Unavailable: Does not have a product type in their stack

- Testing: The product is currently in pilot-testing phase, not live to all customers

- Established: The product is a part of their stack and fully available for customers

- Unique: A unique offering within a product type which is exclusively provided by the virtual banks

Figure 3: Representation of each neobank’s product stack

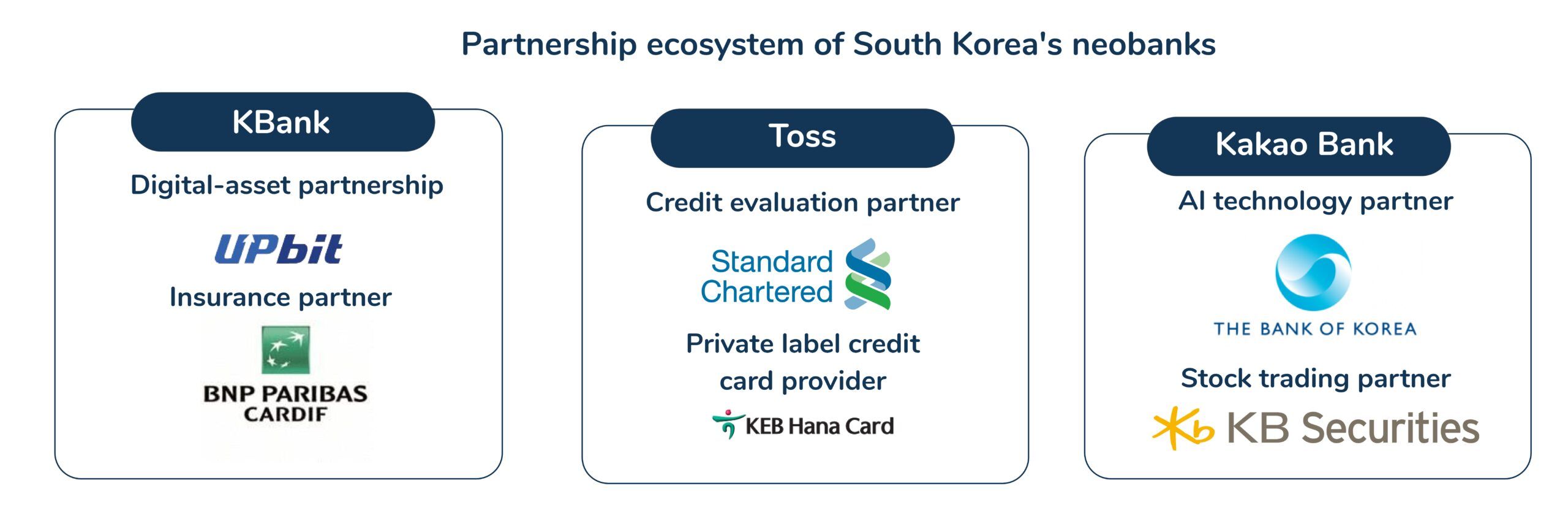

Partnership Ecosystem

- The types of partnerships include:

- Digital-asset/ cryptocurrency partners

- Technology partner

- Credit card provider

- Credit evaluation partner

- KBank and Toss have partnerships with insurance providers to provide an in-app service.

Figure 4: Representation of each neobank’s partnership ecosystem

Open banking

A pilot program consisting of 10 traditional banks was conducted in 2019 by Korea’s Financial Services Commission (FSC). The initial 10 banks included banks such as Woori Bank, NH Nonghyup, KB Kookmin Bank, Shinhan Bank and KEB Hana Bank.

After a successful pilot which saw as many as 5.51 million accounts being registered on the single mobile application, 8 more banks have been invited to join the initiative, including Kakao bank and K bank. The purpose of the open banking initiative is to help customers manage all accounts through a single application.

South Korea’s neobanks’ outlook

South Korea’s financial regulators have taken a conservative approach to digital banking, issuing a limited number of licenses and outright rejecting the rest of the applicants. The only three banks to get a license till now have been: Kakao Bank, K Bank, and Toss.

- Kakao bank and Toss serve 13 million and 16 million customers respectively. Even though the number of neobanks in South Korea is less, they have tapped into the market well. We can say so because they serve around 1/4th of the Korean population

- Kakao bank and Toss’ success has proved that Korea is a successful market for neobanks. On the other hand, K bank is struggling to maintain its customer base

- This indicates that even though South Korea is profitable for neobanks, it’s not easy to attract customers. Especially when nearly 1/4th of the population is each served by Toss and Kakao bank

Annexure

Table 3: List of investors in South Korea’s neobanks

| Name of the bank | Investor |

| K bank | KT Corporation |

| Kakao bank | Korea Investment Holdings, Kakao Corp |

| Toss | Altos Ventures, Goodwater Capital, GIC, Sequoia Capital China, Kleiner Perkins, Ribbit Capital, Aspex Management |

End notes

We have sourced information pertaining to the funding value, round, customer base, revenue, and product information from Crunchbase, Owler, respective company’s annual reports, and their websites.

Aman Jindal, Business Research Analyst Intern, contributed to this research by assisting in writing, conducting preliminary analysis, and conceptualising the topic.