Building completely virtual operating models is no easy feat, as it involves high regulatory, security, and reputational risks. However, disruptive technologies have become an enabling resource that helps neobanks build a nimble and secure infrastructure. This infrastructure allows unprecedented resilience and agility for neobanks to easily test and deploy services on their platforms. A well-defined technology stack enables the democratisation of data and innovation towards frictionless customer experiences. It also plays a significant role in reducing the monthly cost to serve from an average of USD 15 – 20 to USD 1 – 3 per customer, consequently attracting the mass population by offering low-cost solutions. The digital bank of the future, be it an incumbent or a neobank, will have to transform itself with continuous technological evolution. By doing so, digital banks must maintain the central focus of incrementally improving their customer’s quality of life.

Technologies mentioned in Figure 1 will have the greatest impact on the banking and financial services industry in the next ten years by transforming their nature of services and how they are delivered and consumed.

Figure 1: Rise in technology investment by 2030

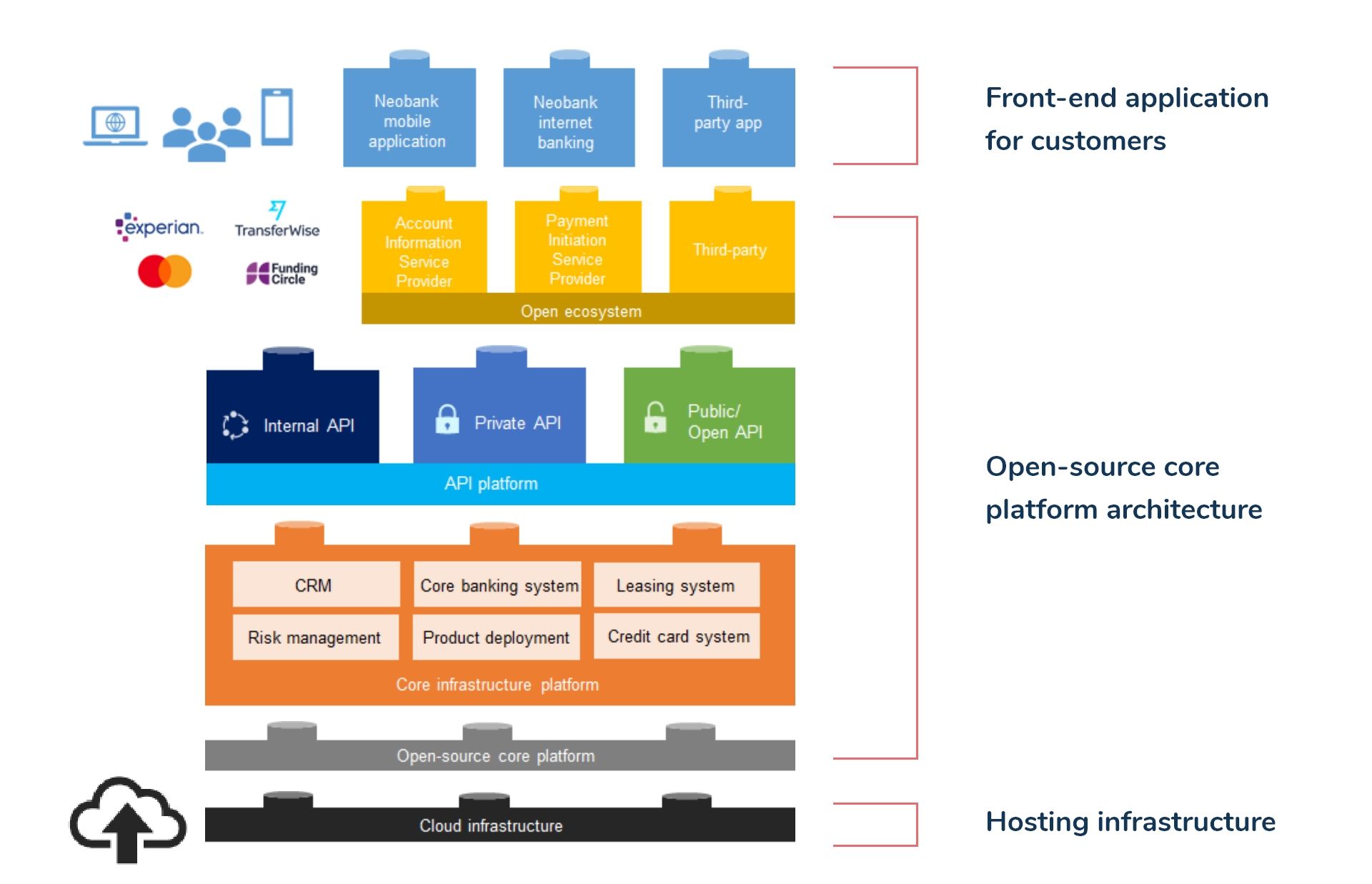

In this article, we deconstruct the current technology stack (see Figure 2) of a neobank and identify technologies that will shape the future of banking.

Figure 2: Technology stack of a neobank today

3 key layers of the technology stack in a neobank

1. Hosting infrastructure

With neobanks entering the market, adopting a cloud infrastructure is imperative for a scalable platform-based operating model. As neobanks operate in a highly regulated and data-sensitive environment, hosting all services on a public cloud is not entirely possible. Instead, most neobanks, whether they are spin-offs, digital platforms, or standalone license holders, prefer a hybrid cloud infrastructure. A hybrid cloud set-up allows neobanks to store and operate in the public cloud for third-party integration and the private cloud to store and develop its services.

A digital-only platform hosted on the cloud enables developers to have an agile environment to create, test, deploy and cancel services within short timeframes. Also known as cloud computing, this environment is crucial in building future-proof platforms; ones that allow neobanks to continuously assess their customer journeys and deliver a superior platform experience.

There is a significant opportunity to reduce capital expenditure (CAPEX) and operational expenditure (OPEX) with the adoption of cloud-native solutions. Neobanks do not incur any CAPEX for maintaining on-premises servers as all the data and services are stored and hosted on their in-house or third-party cloud infrastructure. Additionally, as cloud-native solutions such as software-as-a-service and platform-as-a-service create a favourable developer environment with high-yielding tools and common development languages, OPEX is considerably marginalised.

In the future, neobanks can reduce the load on its private cloud, consequently lowering the cost burden of an in-house platform data storage and maintenance by creating strong security governance measures on the public cloud. This strategy will further gain momentum with the regulatory relaxation on maintaining in-house storage capabilities.

- Success story

- Virgin Money Australia

- Australia’s Bank of Queensland adopts a modern cloud-native, cloud-agnostic, and API-first technology for its neobank Virgin Money Australia (VMA) to accelerate growth and offer differentiated customer experiences. The bank aims to consolidate its retail banking products on a single platform, creating a centralised digital-first experience for its customers.

“Our approach here is that we are not trying to fix the old. What we’re doing is building a new digital bank.” – George Frazis, CEO, Bank of Queensland

2. Open-source core platform architecture

A well-established core platform based on open third-party integration principles is a critical future-proofing strategy for neobanks. Most neobanks are built on the containerised methodology to easily scale, manage, and deploy applications that help them build interactivity and frictionless experiences in the front-end user interface. A key reason for neobanks’ success is the robust platformification strategy they implement to handle the high volume of transactions and function without interruption. Platformification has helped neobanks overcome the challenges incumbents faced with digital banking, such as inviting regulatory scrutiny, customer contempt, and significant revenue loss.

Winning neobanks need a multi-experience digital platform that enables hyperconnectivity across multiple touchpoints and makes banking invisible by seamlessly embedding customer journeys. Additionally, a platform-based approach unlocks potential partnerships between fintechs, third-party developers, and eCommerce players to create an integrated marketplace for financial solutions. A future-proof platform of tomorrow will help neobanks in:

- Setting up robust Know Your Customer (KYC) digital identity mechanics such as biometrics, facial recognition and gesture management using blockchain technology

- Solving critical cybersecurity issues using next-gen cryptography (financial data encoded with quantum cryptography), creating a far more secure environment than current levels of digital security to safeguard sensitive customer information

- Detecting fraudulent activities by recognising behavioural patterns, leading to proactive fraud risk management using Artificial Intelligence (AI)

- Assessing a multitude of variables at lightspeed to create a comprehensive customer profile through machine learning

- Using a combination of quantum computing and blockchain technology to build a hack-proof technology for managing multiple permutations on the modalities (touch, voice, gesture)

- Adopting 5G to substantially increase the speed of computing, developing, and deploying applications on the front-end. This adoption will also help in improving the overall performance of the platform, both in supporting backend architecture and front-end customer interface. Benefits include approving loans in less than a minute and reducing processing costs to less than USD 1.

- Automating decisions using cognitive process automation that sets pre-programmed rules such as the seamless approval of loans and mortgages

- Offering a comprehensive product portfolio through third-party integrations

- Success story

- Judo bank Australia

- Judo Bank Australia is a unicorn neobank and among the first few banks to obtain a full Australian Deposit-Taking Institution (ADI) license. The bank’s foundation is on a solid core banking platform with modern and legacy-free technologies, processes, and systems. Judo Bank grants distressed SMEs in Australia digital-only and easy processing credit lines. AI, open application programming interfaces (APIs) and cognitive automation form the basis of its core platform architecture in accessing creditworthiness, defining eligibility and processing loan applications. With a strong digital platform, Judo Bank has had triumphant success in the SME market by distributing loans worth USD 1.23 Billion and bagged the unicorn status in less than three years of operation.

“We don’t do digital transformation – we do digital. We have built an architecture that focuses entirely on a digital business model that enables human relationships. There is nothing to transform; we started on a blank sheet of paper and took a do-it-once, do-it-right approach.” – Alex Twigg, Co-founder, Judo Bank

3. Front-end application for customer

Customer experience is paramount for any industry’s success, and this is especially true for the banking and financial services industry, where customers demand flexibility, hyper-personalisation, and a broader choice of products to support their unique needs. Neobanks’ profitability and sustainability are largely dependent on delivering superior customer experiences. A major reason for the growing popularity of neobanks is their ability to shift the mindset about banking radically from one that is a serious, standardised affair to a fun, gamified and interactive experience. Humanised experiences are pivotal to a neobank’s strategy with the goal of transforming customers’ lives. Disruptive technology infrastructure including AI, biometrics, 5G, Augmented and Virtual Realities (AR/VR), and quantum computing act as key drivers for achieving cost efficiencies, increasing profitability as well as tapping unbanked and unserved customer segments. Neobanks of tomorrow aiming to build state-of-art customer experiences as the front-end interface should:

- Enhance the use of chatbots and virtual assistants to solve daily customer queries, such as information on the portfolio, transaction history, credit card payments, loan eligibility calculation and approval management

- Empower AI-based assistants to assess monthly spending on each category to adjust savings and spending patterns

- Integrate automated alerts and rewards for falling behind or meeting monthly financial goals

- Create immersive experiences using AR/VR, where the customer can feel, participate, and touch its banking activities throughout the journey inflexions. Gamification of banking activities is now a critical aspect of building resonation in customer experiences.

- Build algorithms and data models for continuously assessing transactional data and information in supporting the customer’s decision-making process through contextualised insights

- Enable multiple forms of digital identity recognition methods such as fingerprint sensors, facial recognition, retinal scanning, and voice recognition to support the customer’s comfort and avoid any fraudulent identity threats. Different biometrics strategies help neobanks support differently-abled customers in accessing and conducting banking operations

- Success story

- TMRW by UOB

- TMRW is a digital spin-off of UOB, catering to the quirky, social media-dependent millennial population of Indonesia and Thailand. The bank delivers a gamified customer experience with the adoption of unique-personified emojis. This emoticon-led approach translates into an in-app game, namely ‘City of TMRW,’ which helps customers meet their savings goals in a fun, competitive, and gamified way. TMRW combines unique user interfaces with niche features that excel against their competitive counterparts. It also has a data-driven insight mechanism to help customers understand their transaction patterns and apply strategies to improve finances

“The next generation of Indonesia’s changemakers are mobile and want on-the-go digital services that enable them to achieve their aspirations. With TMRW, we hope to help them meet their financial goals and to support them as they build a better tomorrow.” – Kevin Lam, President and Director, UOB Indonesia

Conclusion

The neobanks of the future will become ubiquitous and invisible enablers across devices and applications to conduct banking on a day-to-day basis. Rising technologies will impact neo banking in the following ways:

- By 2030, consumers will interact with their bank through robo-personal assistants, facial recognition, and wearable devices, reducing human intervention to as low as 10-15% in a year.

- Cognitive data analytics, machine learning, and AI will enable neobanks to switch from being just a financial service provider to a proactive enabler of unique-personified needs.

- Internet of Things (IoT) will play a significant role in acquiring customer data to enhance and offer personalised products. This solution enables neobanks to continuously enhance its user interface with a humanised experience.

- Innovative cybersecurity through AI and machine learning algorithms will detect frauds and anomalies in real-time to protect core platforms and sensitive customer information.

- Blockchain technology will empower digital currencies and create a secure environment for managing transactional data with defined audit trails.

- Quantum computing will become an integral part of processing a vast volume of data generated on multiple devices and wearables, enhancing customer experience on a real-time basis.

- 5G will provide super-fast connectivity and performance with the potential to process data at the rate of one gigabyte per second, improving both the core platform infrastructure and front-end user applications.

Endnotes

Sourav Kumar, Research Intern, contributed to the research in conducting preliminary literature review, creating infographics, and conceptualising the article.