The creation of a regulatory framework for digital banks promotes a level playing field by allowing new entrants to credibly compete with existing banks, as well as prevents regulatory arbitrage – Benjamin E. Diokno, Governor of BSP

Regulatory initiative:

Bangko Sentral ng Pilipinas (BSP), the central bank of the Philippines announced that a draft of the regulatory framework governing neobanks was scheduled to be released by September 2020, however, we see it likely to be released by the end of the year or early next year.

Similar to the neo banking regulations in Singapore and Malaysia, the Philippines proposes two types of licences namely, ‘Basic’ and ‘Advanced’. The lawmakers intend to limit the BSP’s granting of licences to just five applicants a year over five years.

- A basic digital bank can accept deposits, grant unsecured loans, collect and pay for account holders, provide remittance and bill payment services, and issue electronic money products. The basic digital banks cater to retail and small and medium-sized enterprises (SMEs).

- An advanced digital bank in addition to delivering basic banking capabilities will also be allowed to issue credit cards and grant secured loans. The advanced digital banks cater to retail and SME segments besides large enterprises and corporate clients.

Snapshots of Philippines’ neobanks:

Currently, ING Bank NV, Maybank, and CIMB offer neo banking services to Filipinos through their respective digital platforms. However, Tonik Digital Bank Inc., a subsidiary of Singapore-based Tonik Financial received approval from the BSP in March 2020 which enables the bank to offer services such as retail banking, deposits, and consumer loans, digitally.

Table 1: Profile of the Philippines’ neobanks

| Name | Year | CEO |

| Tonik | 2018 | Greg Krasnov |

| Robocash | Yet to launch | Sergey Sedov |

| OCTO by CIMB* | 2019 | Vijay Manoharan |

| Komo by EWBC* | 2020 | Tony Moncupa |

| ING* | 2018 | Hans B. Sicat |

| Maybank2U MOVE (Mobile Optimized Virtual Experience)* | 2018 | Choong Wai Hong |

| Eon by Union Bank* | 2017 | Edwin Bautista |

| OFBank* | 2020 | Leila Martin |

Note: Annual revenue for the neobanks are unavailable

Table 2: Learning list of the Philippines’ neobanks funding capital

| Name | Tonik |

| Total funds | US$ 27 Million |

| Series A | US$ 21 Million (Jun 2020) |

| Venture round | US$ 6 Million (Feb 2020) |

| Name | Robocash |

| Total funds raised- Pre-IPO round | US$ 5 Million (June 2020) |

In-depth neobank analysis on the 5-building block framework

Customer centricity:

- Through fintech partnerships, the operational neobanks in the Philippines offer cutting-edge, customer-centric services through their mobile application by using UI-UX design to create user-friendly tools and offer their customers real-time notification alert.

- 57% of banks offer virtual assistance to their customers.

- Moreover, 71% of banks offer hyper-personalised services.

- Only 29% of banks offer services such as gamified money management tools, goal setting for spend and save, and spending and budgeting analytics.

Figure 1: Philippines’ neobanks represent all customer centricity parameters

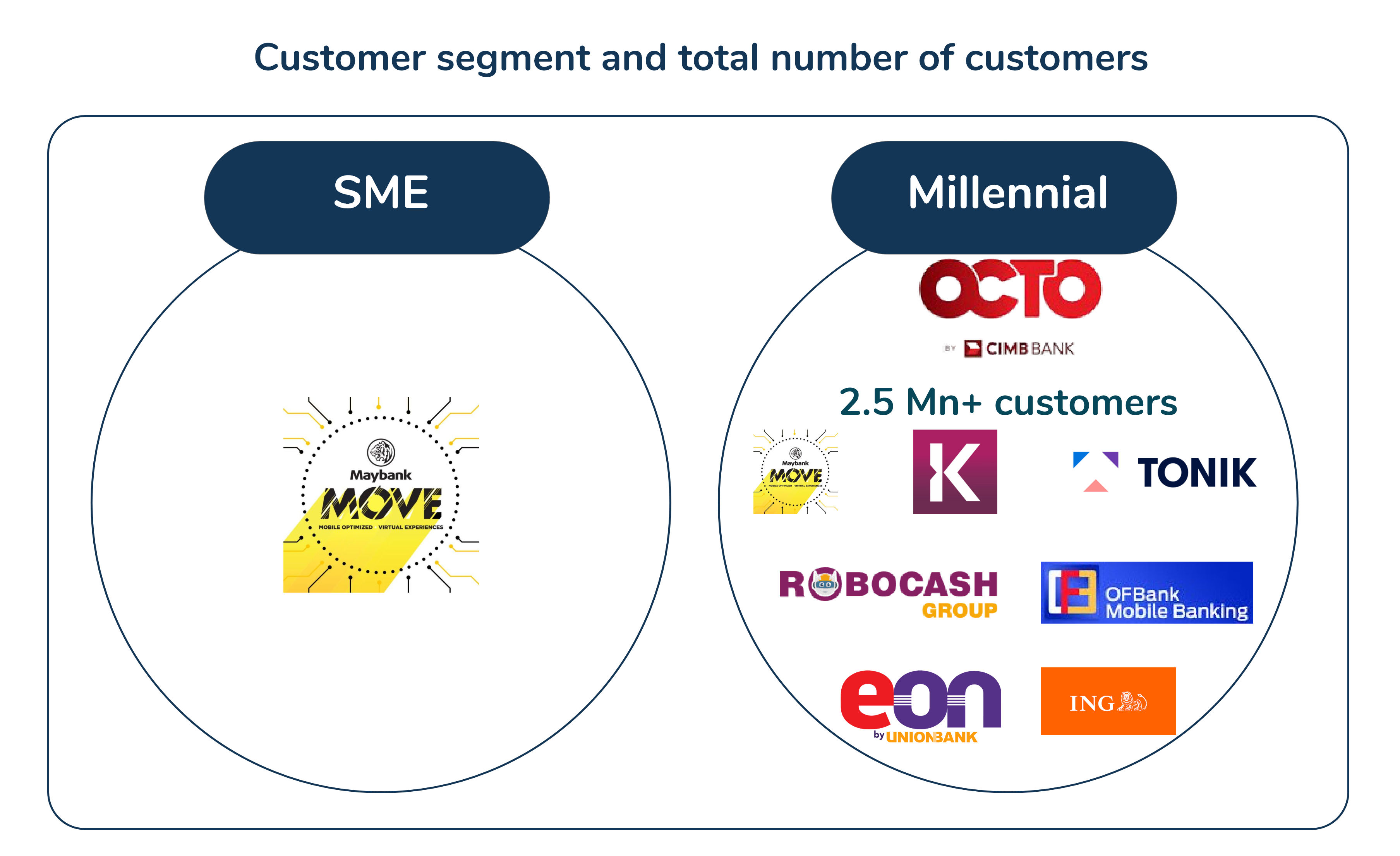

Customer reach:

- All the neobanks in the Philippines primarily focus on serving the millennial generation and the unbanked population.

- Maybank2U MOVE serves the SMEs in addition to its retail customers.

Figure 2: Customer segment and the total number of customers

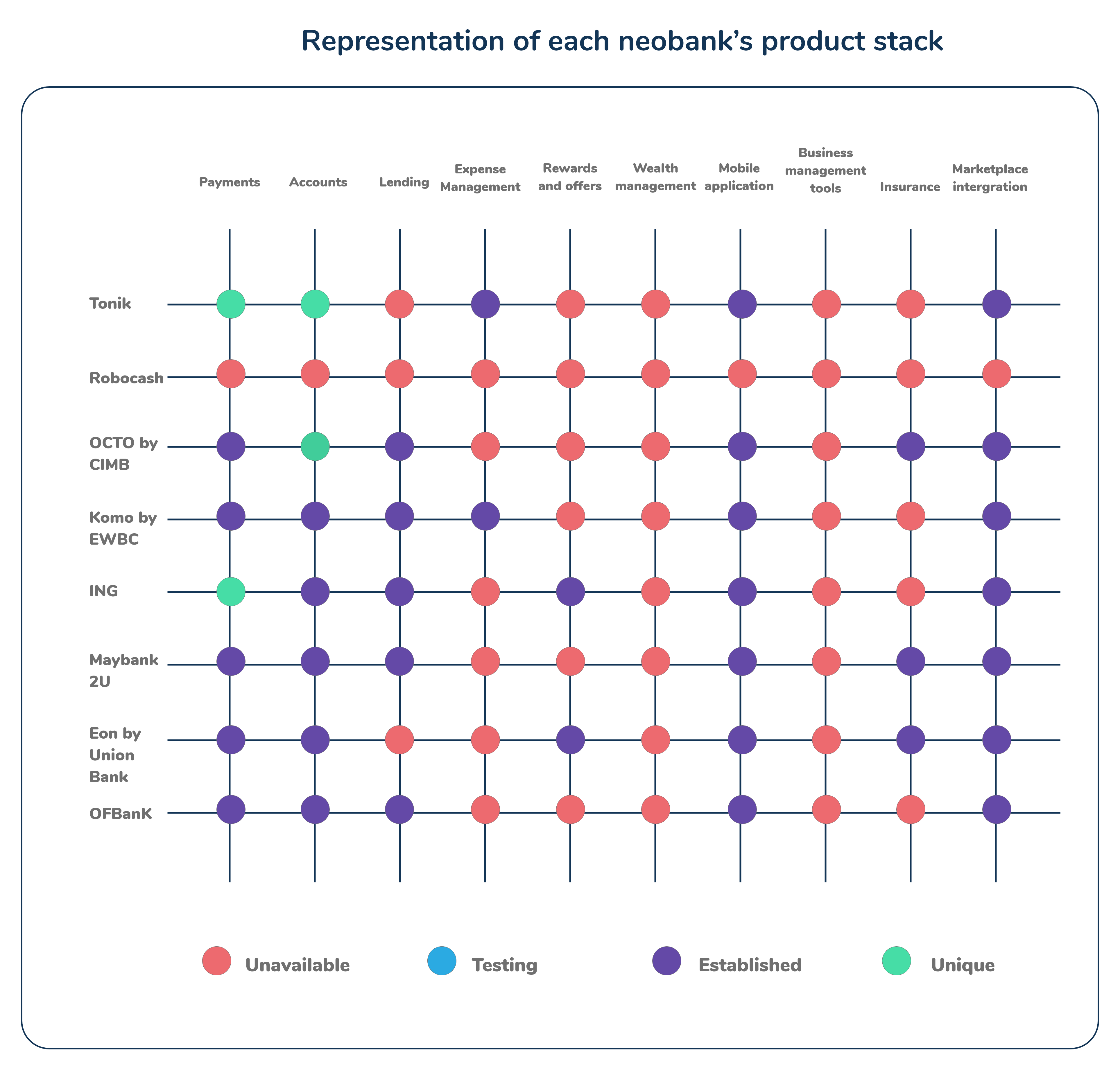

Product stack (Banking solutions):

- All 4 banks have 50% or more products catering to the customer journey.

- OCTO by CIMB offers unique account options such as UpSave Account, Fast & Fast Plus Account, GSave Account, and Personal Loan.

- ING Bank offers its customers virtual cards.

Methodology

Each neobank product stack is a representation of 4 key parameters across 11 product types

- Unavailable: Does not have a product type in their stack

- Testing: The product is currently in the pilot-testing phase, not live to all customers

- Established: The product is a part of their stack and fully available for customers

- Unique: A unique offering within a product type which is exclusively provided by the neobank

Figure 3: Representation of each neobank’s product stack

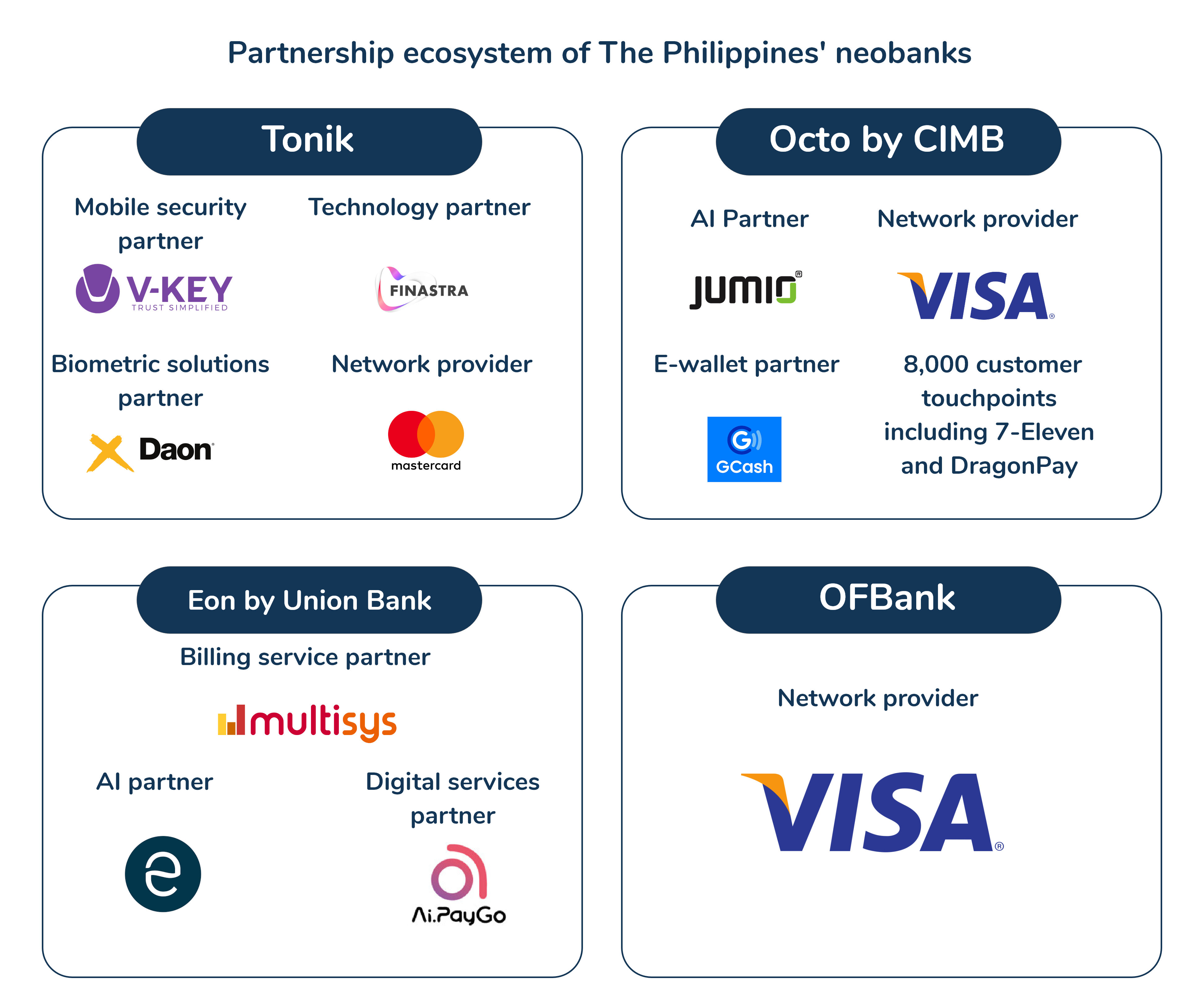

Partner ecosystems:

- Philippines neobanks’ technology partnerships focus on:

- AI infrastructure

- Biometric solutions

- Financial service infrastructure

- Other types of partnerships include insurance partners, network partners, and e-wallet partners.

Figure 4: Partnership ecosystem of Philippine’s neobanks

Open banking:

- As a part of BSP’s 3-year digital payments transformation agenda, the central bank is preparing a regulatory framework to hedge banking customers from potential risks and fraudulent activities.

- This will encourage banks and non-bank players to share information and enable greater transparency by giving customers greater autonomy over their data.

- Tonik, Octo, ING, and Maybank2U use their API developer portal. TONIK has also partnered with Finastra for stack development.

Table 3: API Developers for Philippines’ neobanks

| Name | Sandbox/Developer |

| Tonik | Tonik API, Finastra (For stack development) |

| OCTO by CIMB | CIMBNiaga API |

| ING | ING developer |

| Maybank2U MOVE | Maybank Sandbox |

Philippine neobanks’ outlook:

- 7 in 10 unbanked adults in the Philippines have a mobile phone, this represents an untapped opportunity for enhancing neo banking in the country.

- Philippines neobanks will be able to serve the unbanked population of nearly 46% by leveraging the growing use of internet technology and mobile phones.

- New technological capabilities ensuring easier payments and lending can enhance financial inclusion.

- Banks can accelerate their growth through fintech partnerships by co-creating features that are customised to the needs of every customer and enable smoother neo banking functions.

- Furthermore, the neobanks in the Philippines will not see 100% digitalisation in the next few years. The reason for this is that Filipinos still prefer face-to-face interaction. Traditional banks can offer offline services along with their online services at no additional costs since they already have physical branches. As a result, traditional banks have a distinct advantage over purely digital banks.

Annexure:

Table 4: List of neobank’s investors

| Name of bank | Investors |

| Tonik | Point72 Ventures, Insignia Ventures Partners, Credence Partners |

Endnotes

We have sourced information pertaining to the funding value, round, customer base, revenue, and product information from Crunchbase, Owler, respective company’s annual reports, and their websites.

Akshita Maruthavanan, Research Intern, contributed to this research by assisting in writing, conducting preliminary analysis and conceptualising the topic.