Vietnam has many favourable conditions for neobanks to develop and rapidly scale up. One of which is a large population of almost 100 million with very high adoption of smartphones and the internet -Nguyễn Thiện Tâm, Digital Strategy Director, OCB

Regulatory initiative

While most traditional banks are exploring opportunities to venture into the neo banking domain by providing innovative banking solutions through digital platforms to serve the unbanked Vietnamese population of approximately 40%*, the State bank of Vietnam, is still at the backdrop of forming digital banking policies. However, the country has seen a rise in the number of innovative digital banking services of intermediary e-banking services provided such as e-wallet services and online payment gateways following non-cash regulations. Moreover, traditional banks are also committed to providing innovative digital banking solutions to its customers.

One of the factors largely impacting the local fintech growth include an unprepared regulatory framework. Due to the tight neo banking regulation, the fintech activities have been limited and Vietnam remains an unlikely home base of choice for fintech firms.

Snapshot of Vietnam’s neobanks:

To embrace the virtual banking revolution in APAC, Vietnam’s Viet Nam Prosperity Joint Stock Commercial Bank (VP Bank) and Global Online Financial Solution launched the first bank without branches named “Timo” in 2015. Timo, an abbreviation to “Time & Money”, is a digital banking platform offering non-traditional banking experience to its customers by inviting them to hybrid coffee shop-banking centres and helping the customers onboard on its digital banking platform. In 2020, Timo partnered with Viet Capital Bank to offer neo banking services to its customers.

Moreover, Vietnam Maritime Commercial Joint Stock Bank (MSB) is planning to adopt Mambu’s cloud-native banking platform to launch Vietnam’s first digital-only bank by the end of 2020 under its proprietary banking licence.

Table 1: Profile of Vietnam’s neobanks

| Name | Year | CEO | Total Funds |

| Timo | 2015 | Claude Spiese | US$4.5 Mn |

| YOLO by VPBank* | 2018 | Shameek Bhargava | – |

In-depth neobank analysis on the 5-building block framework

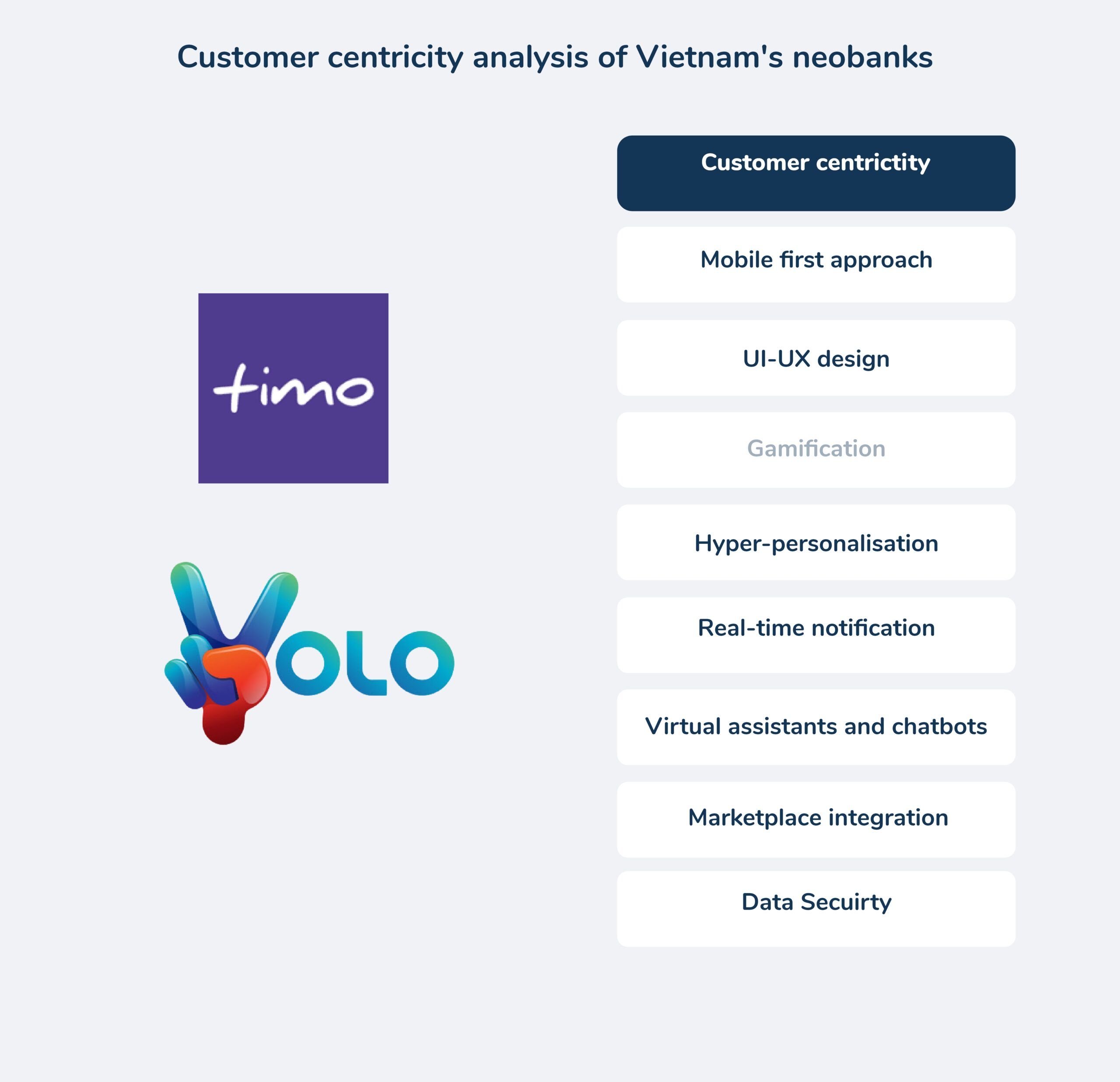

Customer centricity:

- All banks follow a mobile-first approach and employ UI-UX design to create lucrative and user-friendly tools and offer real-time notification alert.

- Both the banks offer hyper-personalised services such as spending and budgeting analytics.

- Furthermore, neither of the banks offer gamified money management tools.

Figure 1: Vietnam’s neobanks represent all customer centricity parameters

Customer reach:

- Timo and Yolo primarily focus on serving the millennial generation.

Figure 2: Customer segment and the total number of customers

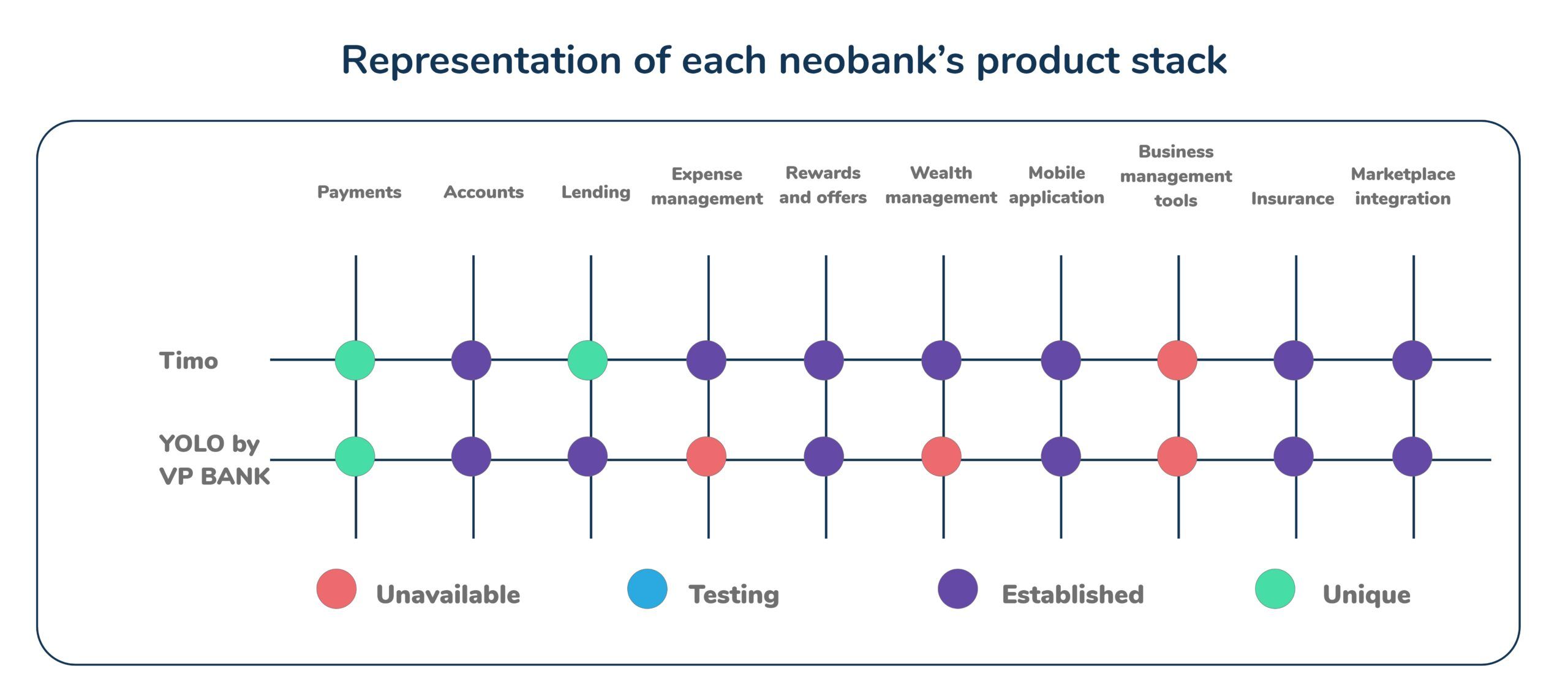

Product stack (Banking solutions):

- 70% or more products catering to the customer journey

- Both YOLO and Timo offer unique payment services such as split payments and virtual cards.

Methodology

Each neobank product stack is a representation of 4 key parameters across 11 product types

- Unavailable: Does not have a product type in their stack

- Testing: The product is currently in the pilot-testing phase, not live to all customers

- Established: The product is a part of their stack and fully available for customers

- Unique: A unique offering within a product type which is exclusively provided by the neobank

Figure 3: Representation of each neobank’s product stack

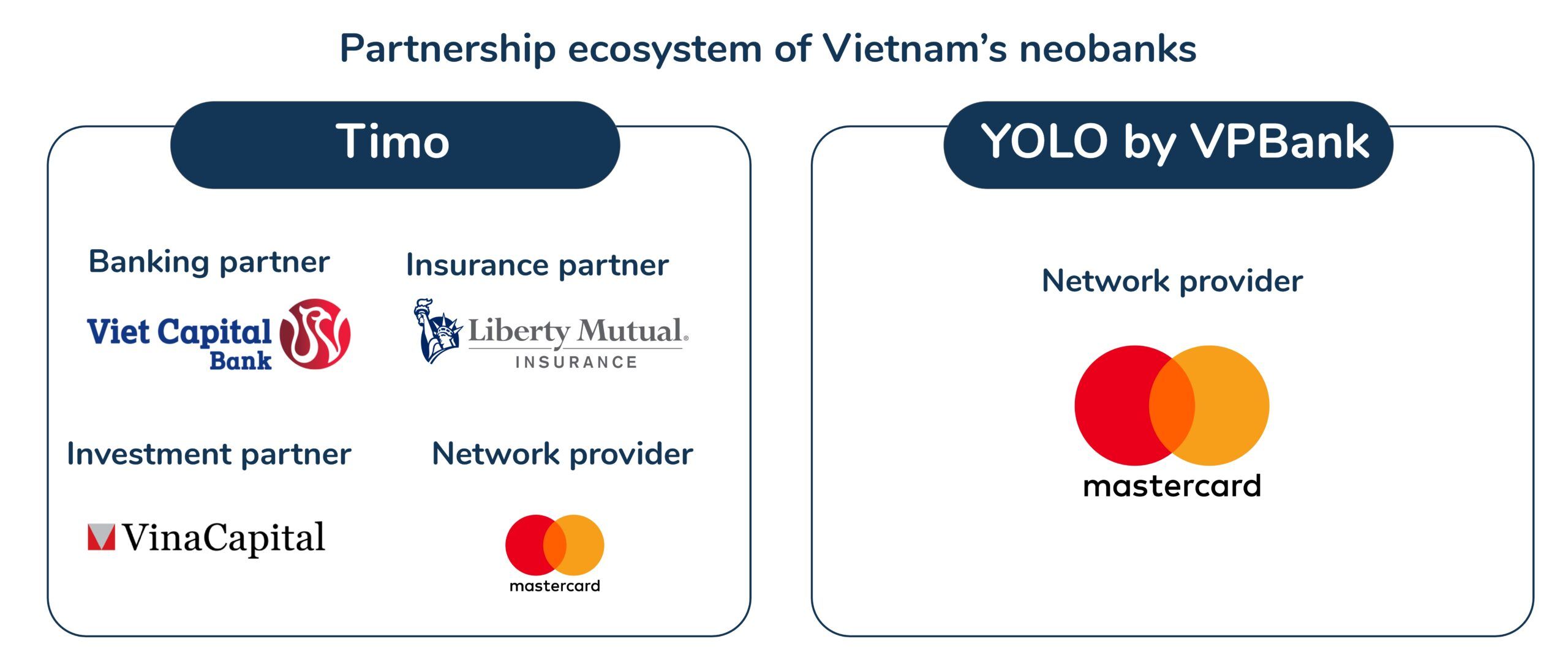

Partner ecosystems:

- Since the State Bank of Vietnam does not allow the complete digitalisation of banks, Timo has partnered with Viet Capital Bank to offer banking services to its customers.

Figure 4: Partnership ecosystem of Vietnam’s neobanks

Open banking:

- The Vietnamese banking regulatory authorities in December 2019, announced that it will issue a regulatory framework for the application of 4.0 technologies such as e-KYC, Open API, big data, artificial intelligence, blockchain, and cloud computing among others, in the banking industry by 2025 to build a strong Open Banking ecosystem.

- Both Timo and YOLO have built their developer portal for third-party API integration.

Table 2: API Developers for Vietnam’s neobanks

| Name | Sandbox/Developer |

| Timo | API for TiMo |

| YOLO by VPBank | VPBank Developers |

Vietnam neobanks’ outlook:

- By employing intelligent automation in account origination, a 50% growth in new accounts by the top 8 traditional banks is expected. This is likely to pose a threat to Vietnam’s neobanks.

- Banks can partner with fintech companies and other non-bank players including telecom and technology giants to accelerate digital innovation in the banking sector. This will enable them to provide enriched and personalised services such as improved data security, spend analytics, and gamification. The joint-stock banks are expected to win a major part of the market share.

- The market for neobanks in Vietnam is still at its nascent stage. In the upcoming years, we will witness a rise in the number of digital platforms in which non-bank players partner with traditional banks to provide neo banking services to their customers.

Endnotes

We have sourced information pertaining to the funding value, round, customer base, revenue, and product information from Crunchbase, Owler, respective company’s annual reports, and their websites.

*World Bank’s financial inclusion 2017 report

Akshita Maruthavanan, Research Intern, contributed to this research by assisting in writing, conducting preliminary analysis and conceptualising the topic.