Twimbit, in association with F5 Networks, organised the second session of “The Asia Pacific Telecom Summit 2021: The Great Debate – Can new entrants win in financial services?” back in March 2021.

Twimbit spoke with Ganesh Ananthanarayanan, Chief Operating Officer, Airtel Payments Bank, and Suman Gandham, Founder and Chief Executive Officer, Finin Bank, to understand the achievements, vision, and goals of the neobanks. The discussion highlights the growth opportunity for telecoms and neobanks in financial services, India’s neo banking regulatory regime, and the changing trends and demands of consumers.

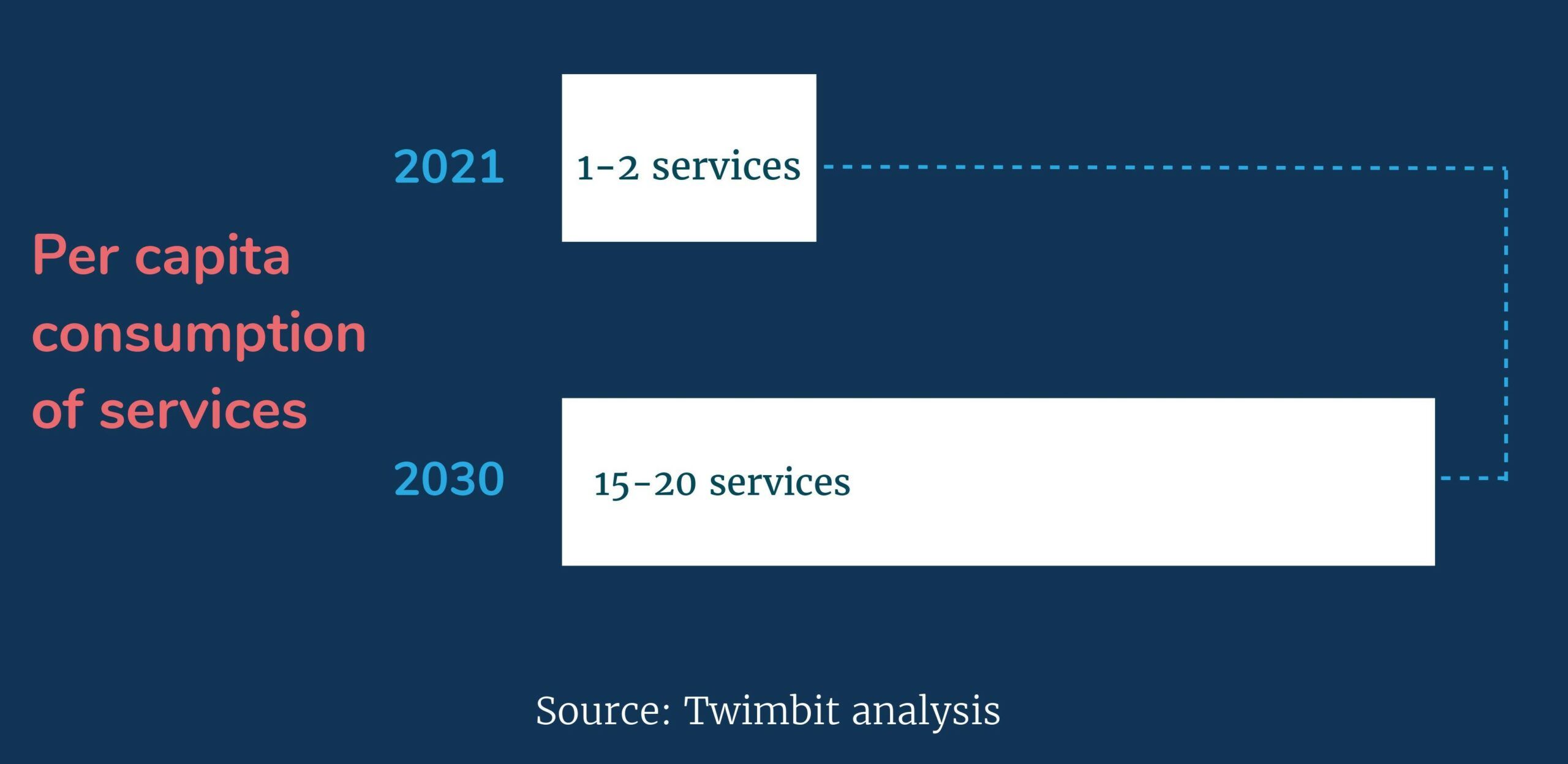

Sizeable opportunity for neobanks and telcos in financial services

Financial inclusion and growing consumer demands exhibit an explosive growth opportunity for neobanks and telcos to win in emerging markets of the Asia Pacific. The exponential rise in mobile and internet adoption is fuelling the demand for digital banking services. Moreover, per capita consumption of financial services may rise to 15-20 services per customer as opposed to 1-2 services in 2021 (Figure 1). New entrants can leverage this opportunity to offer a variety of customised digital services through their digital channels to previously overlooked society segments.

Figure 1: Growth in per capita consumption of financial services

Customer centricity is paramount to drive user and revenue growth

Customers emphasise on hyper-personalisation and are willing to pay an extra amount for simplicity, consistency, and transparency. Telcos have access to a huge amount of data on consumers. Telcos could, therefore, democratise the data available and innovate unique customer-centric solutions to get an even footing with existing market players and differentiate themselves altogether.

We call ourselves the Fitbit of finance. We help our users with better financial habits, so they can save more by automating their savings, building goal-based savings, and smart budgeting. We cover 360 degrees of financial banking for white-collar job holders and freelancers. – Suman Gandham, Founder and CEO

Telcos and neobanks share mutually beneficial synergies

Telcos and neobanks in the Asia Pacific can mutually benefit by collaborating and leveraging each other’s strengths. Neobanks can avail themselves of the telcos’ brand name, the large network of customers, and existing physical infrastructure to gain a foothold in the banking industry. Meanwhile, they can facilitate a simple, insightful, hyper-personalised, and transparent financial services infrastructure by streamlining their business models and deploying the latest technologies to serve the banking needs of customers.

We do rely quite extensively on the telco. I think the most important aspect really is the brand. The relationship (with Bharati Airtel) is working extremely well where we’re able to leverage the strengths of the telco and help the bank scale. Otherwise, getting to [USD] 35 billion dollars in annualised flows and being contribution positive in a three to four-year time frame wouldn’t have been possible without the support of the parent company. – Ganesh Ananthanarayanan, COO, Airtel Payments Bank

Low margin products pave the way for profitability

Service providers use low margin services such as UPI and utility bill payments to drive engagement on the platform, increase product turnover and scalability. The increased customer engagement gives the said service providers an opportunity to cross-sell third party products and services. In addition, low margin products can be used as a launchpad to sell high margin lifestyle financial services, such as insurance, wealth management, and business solutions. This leverage contributes to efficiency gains. Banks should ensure that their customers’ banking experience while using low margin services is simple and engaging, leading to customer stickiness.

Segment-focused scalability is the key to winning in the future

Neobanks are increasingly focusing on creating niche banking solutions that focus on addressing the pain points of individual segments. Financial service providers currently target three broad segments: the low-income rural population, white-collar workers in tier 1 and tier 2 cities, and the student population. A segment-focused customer acquisition approach enables banks to create an enriched and hyper-personalised experience, one that will subsequently increase profitability and enhance micro-segment inclusion.

Regulations are important to build trust and loyalty among customers

In recent years, several neobanks have faced shutdowns, heavy losses, or forced to apologise to their users publicly due to security breaches. They have access to enormous data on customers that could be exploitable when unintended users access it. These breaches call for a more structured and stringent regulatory framework to ensure that financial services providers adhere to protocols and regulations. Having a proper regulatory strategy in place instills trust and confidence in customers, resulting in long-term stickiness.

Organisations could cross the boundary, and it may not be good for the customers. So, I believe that the regulations in India are very centred towards ensuring that the people’s money is protected. I think the regulations are very critical for the success of the banking industry itself. – Ganesh Ananthanarayanan, COO, Airtel Payments Bank