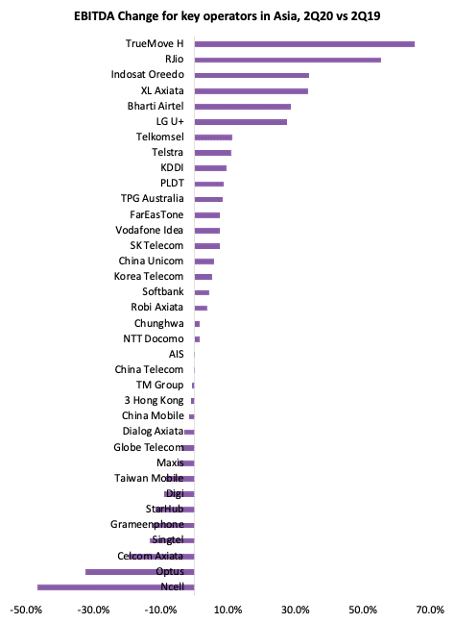

Telecoms as an industry has taken center stage during Covid-19. It has become a critical guage of the ability for many to work from home, stay connected with family and be the conduit for the consumption of a multitude of digital services. A vast majority of the service providers has however seen an impact on their revenue and profitability. A few have weathered this storm well and are likely to emerge stronger in the post Covid-19 era.

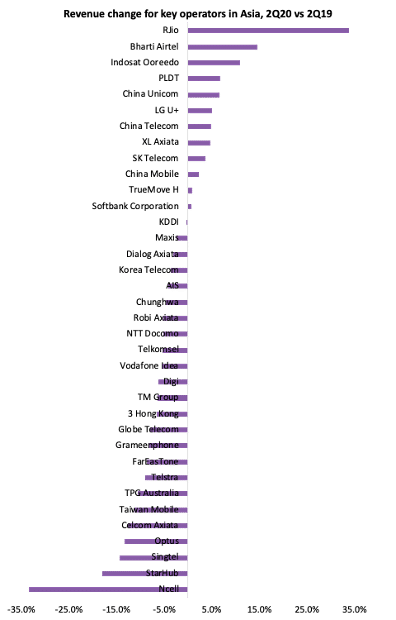

Top five revenue gainers

Revenue growth for service providers in the region remained suppressed for the second quarter, that ended in June, 2020. Operators in the region’s largest markets, India and China, showed resilience to the Covid-19 impact as they reported robust increase in service revenues. The following operators have emerged as top revenue gainers:

| Operator | Change in revenue (2Q20 vs 2Q19) | Growth drivers |

| Reliance Jio | 33.7% | 1. ARPU improvements 2. Industry wide effort to improve pricing discipline |

| Bharti Airtel | 14.6% | 1. ARPU growth with a focus on acquiring and retaining quality subscribers |

| Indosat Ooredoo | 10.9% | 1. Improved ARPU 2. Turnaround strategy with focus on strengthening data business |

| PLDT | 6.7% | 1. Diversified business – mobile, fixed broadband, and enterprise helped in hedging COVID-19 risks |

| China Unicom | 6.6% | 1. Fixed-line service segment 2. Innovation in enterprise service bundling – cloud + networks + applications |

Key takeaways from 2Q20 results

Enterprise units performed better during crisis

Our study across 36 telecoms service providers assessed in the 15 countries of the Asia Pacific reveals that compared to the consumer business segment, the enterprise business units have performed better and been more resilient. The demand for integrated solutions that combine enterprise-grade connectivity, collaboration tools, and security services was driven by work from home requirements necessitated by Covid-19.

| Operator | Change in revenue (2Q20 vs 2Q19) | Change in enterprise revenues (2Q20 vs 2Q19) |

| Maxis | -2.4% | 84.0% |

| China Mobile | 2.2% | 18.4% |

| Bharti Airtel | 14.6% | 9.2% |

| Spark New Zealand* | 3.8% | 8.1% |

| PLDT | 6.7% | 7.4% |

| KDDI | -0.3% | 5.8% |

| China Telecom | 4.9% | 5.1% |

| KT Corp | -4.0% | 2.5% |

| StarHub | -17.9% | 1.7% |

| Chunghwa Telecom | -5.0% | 0.1% |

| Singtel (Singapore) | -15.2% | -4.4% |

| Telstra* | -9.0% | -4.7% |

Strong digital business helped telecoms restrict revenue declines:

Telecoms service providers that have led the transformation towards data and digital-led businesses have registered better growth than did their counterparts. The increase both in the consumption of data and other digital services has supported the revenue growth. The simplification of mobile plans and the tools for digital customer engagement have helped the successful operators make most of the consumer demand and needs. Case in point are the Indonesian operators. Among its peers, incumbent Telkomsel faced declines in service revenues during 2Q20. For both XL and Ooredoo, digital services account for the majority of revenues, with non-voice representing 92% and 85% of total mobile revenues respectively. Comparatively, Telkomsel still earns around 30% of its revenue from legacy voice and SMS services.

Operator 5G and digital transformation plans stayed relevant during the pandemic:

Even during these uncertain times, operators have continued their efforts to introduce and scale 5G services. It has spurred innovation by identifying new use cases in areas such as healthcare, manufacturing, autonomous vehicles, and smart building management. As the physical stores remained shut, the digital-focused operators were better placed to support their customers during the various stages of the lockdown. For most operators, focus shifted to delivering digital first experience by introducing prepaid and postpaid activations through digital channels and contactless payments.

Business model innovations during COVID19

- Reliance Jio’s digitalized distribution channel: Jio reconfigured its retail channel by launching an app for peer-to-peer recharges. The launch of the Jio Associate program allowed their associates to provide recharge services to customers within their respective locality. Withintwo months of the launch, Jio had acquired 1.2 million associates who utilized JioPOS Lite app to offer recharge services to the others.

- Spark New Zealand’s innovation in customer experience: To improve the experience for customers shopping online, Spark introduced a virtual shopping store that looked and felt like its physical stores. The idea was to deliver a richer and more engaging experience akin to the physical stores when customers shop online. The users can browse interactive 3D models of key products, view product demos or overviews, chat with the retail team, all while experiencing the products online. The customers can complete the purchase online and can either collect products from the stores or ask for them to be shipped. Spark converted most of their stores to no-contact distribution centers.

- HKBN’s unique approach to corporate social responsibility: The operator took a unique approach to support its enterprise clients who were struggling to make payments for using HKBN’s telecoms and technology services. It introduced a ‘Barter and Bundle’ plan that allowed its enterprise customers to offset part of their payments for HKBN’s connectivity services with their own products or services.