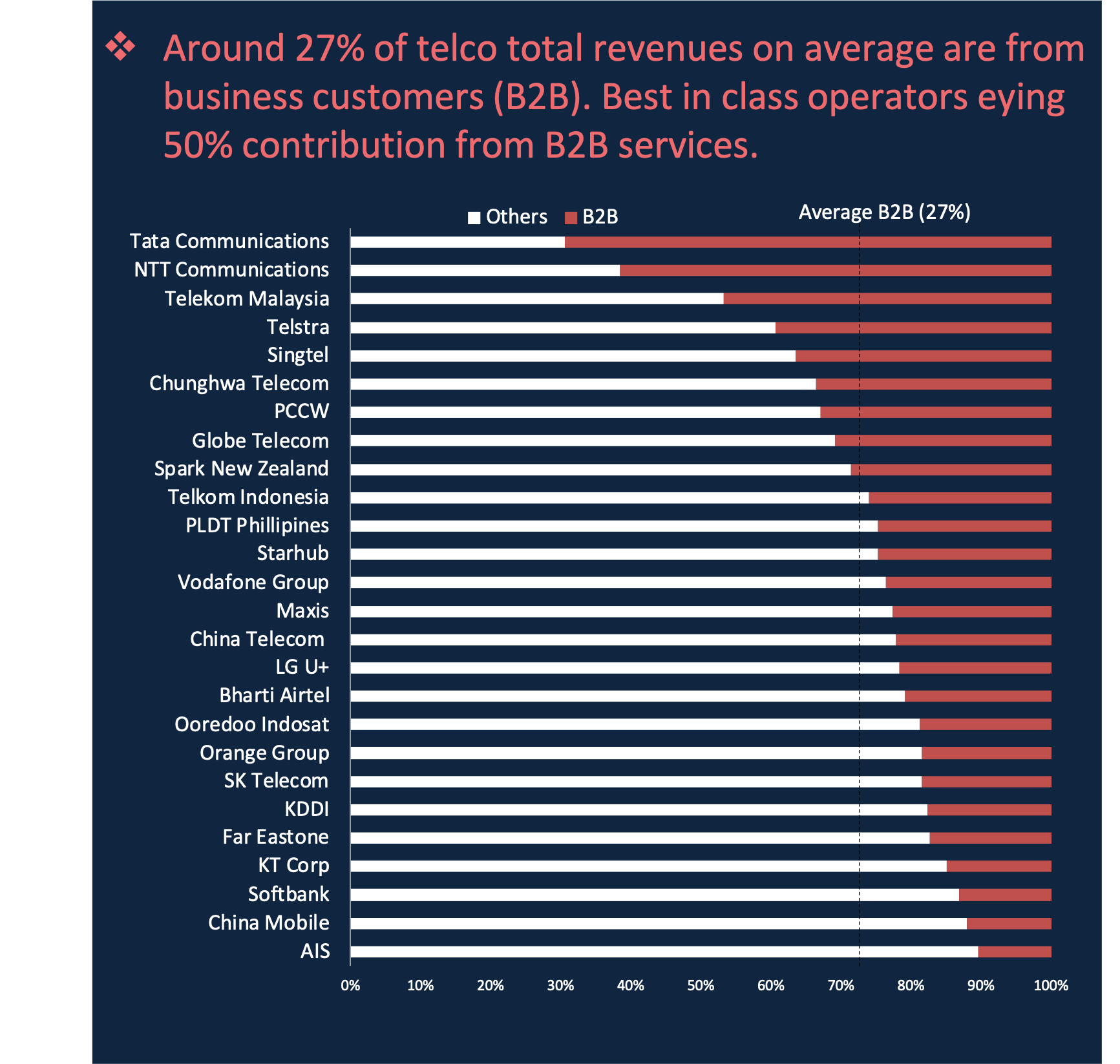

1. Tighten focus on B2B segment contribution

Contribution of enterprise business to telco revenues is much higher for tier1 operators such as Tata Communications, Singtel, Telstra, NTT Comms, and Telekom Malaysia, owing to their ability to address the networking and connectivity needs of multinationals. Many others are finding themselves strong footed in the small and medium enterprise (SME) and SoHo (small office and home office) segments.

As digitization continues to gather pace with COVID-19, businesses and institutions of all shapes and sizes are experimenting with digital technologies. This will continue on, as organizations keep up with government mandates on social distancing, remote working, and remote learning.

For service providers, serving SME/SMB segment is a sweet spot with the scale that it brings. Building scale is necessary in the B2B segment where margins have typically remained low compared to consumer business. Where best in class operators will eye increasing the contribution from B2B services to over 50% in the coming years, others must also tighten their focus on growing enterprise segments in 2021.

5G enabled technologies offer the brightest spot

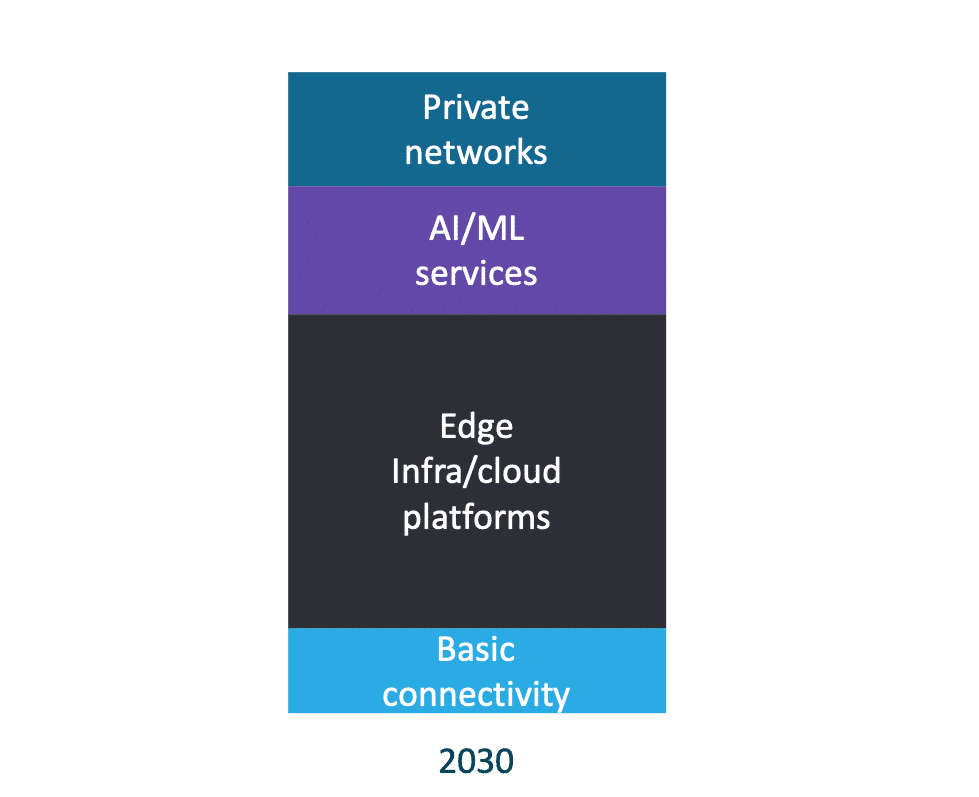

5G will play an important role in the rapid expansion and adoption of digital transformation technologies in the post pandemic world. A study from Nokia Bell Labs further explores this opportunity for telecom service providers. According to estimates, 5G and related technologies, which include edge cloud infrastructure, private networks, augmented intelligence, automation, sensing, and robotics, will present a $4.5 trillion opportunity by 2030.

- $4.5 trillion in IT spending by 2030 with 5G and related technologies

- Edge infrastructure and cloud platforms account for 50% of 5G enabled technology spending

- Other major contributors are private networks and AI & ML services

Building enterprise digital services with public cloud and security

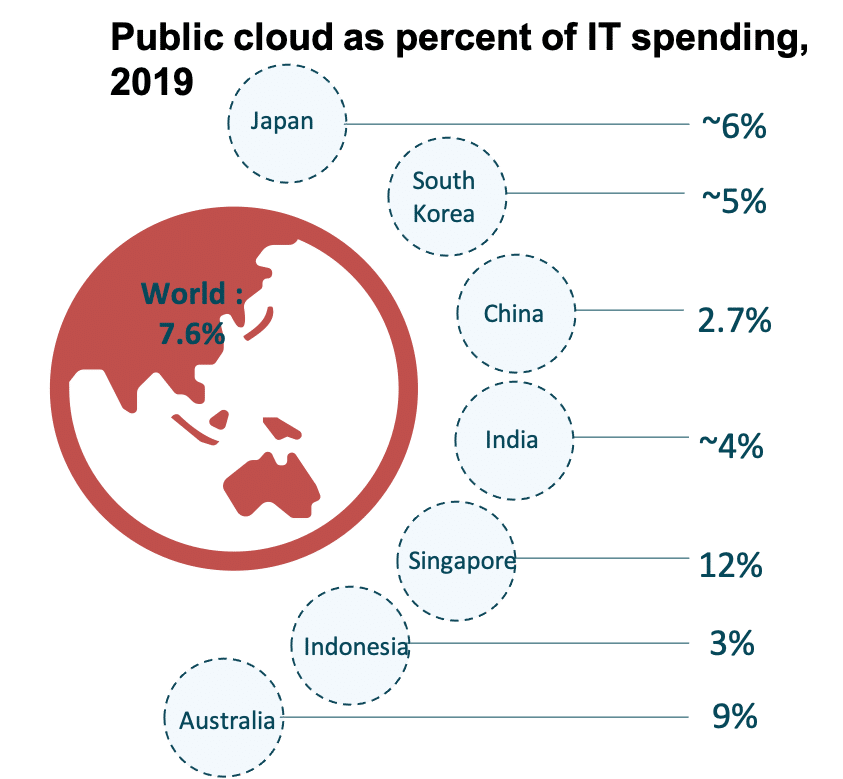

When compared to the world average, the percentage of IT spending on Public cloud in emerging Asia is much lower. Twimbit forecasts Public Cloud market in South East Asian markets – including Singapore, Malaysia, Thailand, and Indonesia – to demonstrate double digital growth in the coming years. Public cloud giants, Amazon, Google, and Microsoft, have already dominated Asian markets, leaving fewer opportunities for local providers to scale up. Increasing adoption of multi-cloud and hybrid-cloud environments is likely to benefit telco’s pivot to cloud.

Managing multi and hybrid cloud environments for enterprises – Telcos can enable enterprises to manage multiple clouds using a single control pane or platform for cloud orchestration.

Professional and managed services is another area where telcos can support enterprises with their cloud journey. Opportunities would arise for service providers that can offer more modular service packages, easier procurement & delivery.

Security is another focus area for telcos

Technologies of remote work made it possible for organizations to continue business as usual without many disruptions. While IT teams responded quickly and enabled businesses to adapt to the radically changed realities, securing this transformation is emerging as a top priority. IT transformations led by COVID-19 have long term implications for enterprise security needs and changes in their security strategy.

- Securing endpoints: vastly expanded access means not only include thousands of new endpoints but also the increased number of IT services and third-party applications.

- Securing networks: home networks became natural extension to business networks. They must offer similar level of risk assurance compared to an organization’s on-premise networks.

- Securing targeted applications: use of cloud-based applications to support digital workspace moved user identity and access management outside enterprise environments.

- New approaches emerging insecurity architecture: security solutions to manage resource authorization alongside privilege management, network access, and policy management.

2. Addressing growth from adjacencies

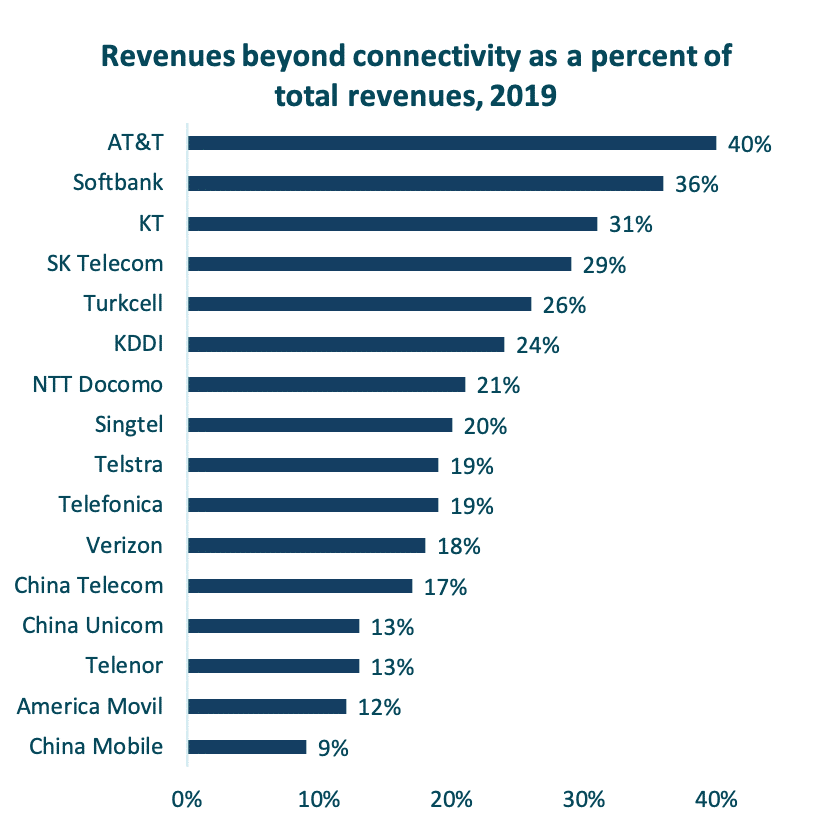

Only 22% of telco revenues are generated from non-connectivity services

Fast commoditization of data and voice is impacting revenue growth from connectivity services. Globally, telcos have been trying to offset loss in core revenues by addressing opportunities in adjacent markets. The quest to improve shareholder will renew over the next decade, pushing service providers to build secondary growth engines.

Telcos are building new growth engines across 5 categories

- Content (eSports, Cloud gaming, VoD, music): Content is a cornerstone to telco expanded service offerings. Historically, pay-TV remains a key component of telcos quad and triple play offers. Changing content viewing and consumption behavior has several implications for the content strategies for telcos, which is now shifting towards soft and hard content bundles by partnering with OTTs.

- Commerce: There are many examples where telcos have pivoted to commerce for additional growth. SK Telecom, RJIO are notable examples of telcos utilizing core infrastructure to build strong commerce platforms. There are multiple avenues for scaling into a commerce platform. For instance, SK Telecom’s commerce subsidiary 11Street onboarded Amazon as an equity partner.

- Analytics/ Mobility/ location-based services: Data driven analytics is another focus area. Singtel’s DataSpark leverages location data to offer mobility intelligence as a service. Another example is SK Telecom’s T-Map business that formed joint venture with Uber to scale mobility-as-a-service offering.

- Mobile money and payments: Mobile money is the most popular digital offering from telcos (including carrier billing). Depending on local regulations, operators have either acquired specialist licenses or partnered with BFSIs to venture into payments business. Globe’s Gcash, Airtel’s Payment banks, and Veon’s JazzCash, and Viettel’s ViettelPay are some examples.

- Fintech/Digital banking: Telcos are expanding beyond the simpler mobile wallet and mobile money services to address the financial needs of underbanked and unbanked population. Traditionally focused on B2C, some telcos are now expanding to B2B banking and financial services. BT Radianz is an early mover. Locally, Chunghwa Telecoms collaboration with Next Bank makes for a relevant example.

3. Digital experience is enabling growth from millennials

MNOs delivering enhanced CX with digital sub-brands

Operators are helping customers curate, bundle, and integrate digital and entertainment services. Telcos are working to provide a personalized and uniform customer experience with the goal of becoming the customer’s digital lifestyle partners.

Digital experience is important particularly as telcos try to engage with younger consumers. A starting point for traditional telcos is introducing digital sub-brands. This reduces the stress for a complete overhaul of a telco’s existing technology stack.

The new sub-brand can be launched using cloud-based agile systems that can be designed to deliver better customer experience. Separating the brands also allows the parent operator to build new talent, particularly by hiring experts from outside the telco industry.

4. Telcos with in-house engineering capabilities are finding more growth avenues

Service providers who have been successful at addressing business challenges – in areas such as 5G, digital services, and telco digital transformation are leveraging their learnings and expertise to solve similar issues for other network operators. Engineering driven telcos, that have access to the right resources and capabilities, such as Rakuten and Reliance Jio, are taking their 5G cloud platforms to other telcos.

- Rakuten, for instance, has been setting up alliances with channel partners. In addition to being resellers, these channel partners will offer system integration and deployment services for its Rakuten communications platform (RCP).

- A similar strategy was adopted by NTT DoCoMo. Its subsidiary business DoCoMo Digital leverages expertise and knowhow in building successful digital businesses in mobile commerce. It deploys direct carrier billing payment solutions for other telcos and merchants.

5. Strengthening telco role as aggregators

While telcos may not venture into content production, invariably all must pursue innovative packaging and bundling of content. Asian subscribers typically accesses multiple OTT services. Price sensitivity means consumers are also open to more flexible packaging options. Telco value creation lies in building platforms with billing capabilities that can offer intuitive curation, personalization, and flexible pricing models.

Our next article discusses 2021 priorities for telcos – people, partnerships, processes, and technology.