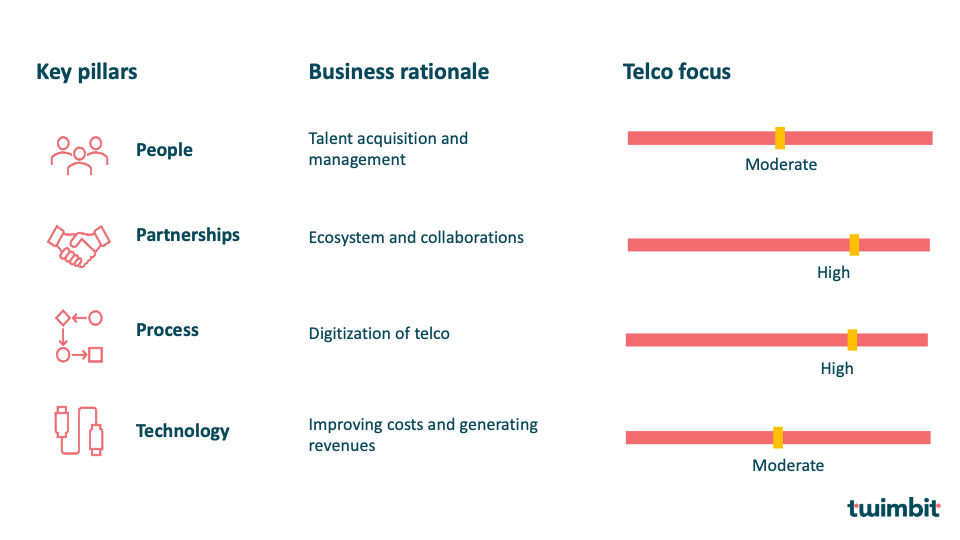

People

Service providers to build teams with diverse skill sets

Telecom operators aiming to expand themselves beyond connectivity will also need to address any existing skill gaps required for becoming more IT and technology centric. In our view, digital telcos will need teams that can think and execute differently from the traditional businesses. There are multiple ways telcos may achieve this. Joint ventures, acquisitions, and partnerships are a way of bringing people from diverse backgrounds under a common roof. Others will continue with a bolder approach, reshuffling leadership positions that may be occupied by executives from very different industries.

Talent management will mean merging deep telco knowledge with emerging tech

Talent management will involve overcoming two key challenges. Service providers will have to work much harder to attract the brightest talent which sees working with tech giants more fulfilling and rewarding. This is a must for operators, if they are to drive internal and external innovation. At the same time, ensuring a core team with deep telco knowledge, which has an understanding on emerging tech, will be imperative. The service providers therefore will focus on convergence of telecoms knowledge with emerging tech within their core teams.

Building in-house capabilities while relying on partner skills

Operators will invest to expand the skills available to them in-house. This is aimed at improving telco capabilities in delivering system integration (SI) or project-based work and position better in the B2B segment. Although operators have relied on partner capabilities, enterprise shift towards multi-vendor arrangements (with cloud, security, etc) will require service providers to build in-house capabilities in delivering or orchestrating solutions from diverse ecosystems.

Partnerships

Multi-cloud adoption among enterprises will continue to drive telco partnerships

Telco partnerships with cloud providers has gained momentum. Where hyperscalers are taking the lead on shifting enterprise applications and workloads to cloud environments, telcos are also benefiting. Growth in partnerships between telcos and hyperscalers is fueled by 5G use cases. For instance, achieving low latency for certain applications will move compute close to (network or device) edge. While service providers can deliver edge capabilities along with 5G connectivity, it would demand close collaboration between cloud and edge providers. These collaborations will be essential for ensuring that applications are deployed and run seamlessly across the distributed multi-cloud environments.

Driving innovation through collaboration

Collaborations are needed across the telco value chain as well as in cross-industry integrations. There is opportunity to harness partnerships to drive new 5G use cases as telcos alone do not possess all vertical-industry knowledge for developing specific applications.

Building scale with digital

Profitable digital businesses require scale. Partnering with other telcos and non-telco firms to scale own digital services is important. Adopting open architecture with API integration capabilities will help telcos achieve this.

Processes

Telcos will focus on integrating themselves better in the digital ecosystem

Telcos have tried digital transformation for many years. The transition, however, is not easy. They are constrained due to the existing business and operating models, infrastructure capabilities, and capital structure fundamentally different from those of the webscalers and digital natives. However, telcos will continue experimenting in this area. Many are now warming up to partnerships with super app providers. There will be focus on opening telco architecture to work more with digital service companies in areas such as health-tech, e-commerce, digital banking/financial services, and education, leading to a convergence between the two.

Softwarization of own processes and networks is also a priority

For telcos, a huge chunk of costs is associated with their legacy systems (OSS/BSS), infrastructure, and back-office processes. While telcos have been in a cycle of transformations, they have made little progress on bringing agility and scalability to internal processes and systems. Operators have already seen part of networks that were earlier hardwired to software-based abstractions. Technologies such as software defined networking (SDN), Virtual network functions (VNF), and network function virtualization (NFV) are already part of telco networks. We expect to see service provider efforts towards softwarization of network and processes to continue, particularly in a world where technologies such as 5G, cloud, AI, and IoT are changing existing business and operating models.

Technology

As-a-service models to gain importance with virtualization and cloudification of network infrastructure

The drive to virtualization and cloud with 5G will lead to changes in service provider business models. Particularly of interest to service providers and developing fast is network-as-a-service. The ability to transition existing network functions to virtualized network functions eliminates the need for legacy approaches to network equipment deployment. With virtualization, service providers can create specific network capabilities in a cloud environment for enterprises that do not wish to deploy their own network infrastructure. This brings a fundamental shift in the business model which moves from capex-heavy to opex-based.

Capex and opex rationalization with open network technologies

Telco strategies are focused on both capex and opex rationalization with the adoption of open technologies. Most discussed is the use of open RAN (radio access network) solutions with a promise of cost savings for service providers. Meanwhile, 5G means heightened capital expenditure (capex), which is also necessary for renewed revenue growth. The impact of open technologies on cost savings is still not established, however, and the introduction of new suppliers means diversity and competition in the vendor landscape.

Automation in service provider networks

Most telcos are already incorporating artificial intelligence (AI) driven automation into networks. Increasing complexity of telecommunication networks with 5G will further strengthen the role of AI in future networks.

AI systems and infrastructure investments are being made with the focus on building self-optimizing networks (SONs), predictive maintenance of telecom infrastructure, and optimizing telco capital expenditure. Using AI for network planning is finding great potential by allowing telcos to rationalize investments in network expansion and capacity enhancements.Service providers are implementing AI for fixing network and traffic anomalies to improve network performance and management.

Other major areas where AI is finding relevant implementations is customer service and experience. Conversational AI platforms, or virtual assistants, are been successfully used for handing the increasing number of customer support calls to service centers. Using AI, operators are introducing self-service capabilities to help customers install, set-up, debug, and operate their own devices.