Enterprises are becoming a growth engine for telcos

Enterprise services are emerging as a strong source of revenue growth for most operators analysed under the September 2020 update. Stagnation in consumer business is reflecting onto the growth in total revenues for telecom operators. At the same time, certain factors are helping telcos drive business from enterprises. Teleworking and collaborations have helped operators revive demand for traditional communication services, particularly in IP-VPN and business communication solutions. The sturdy growth in revenues from non-connectivity services, particularly cloud, security, and vertical solutions, marks a clear shift in operator strategies. However, we note pricing pressure in the connectivity segment for certain markets, where smaller providers are challenging incumbents in enterprise connectivity.

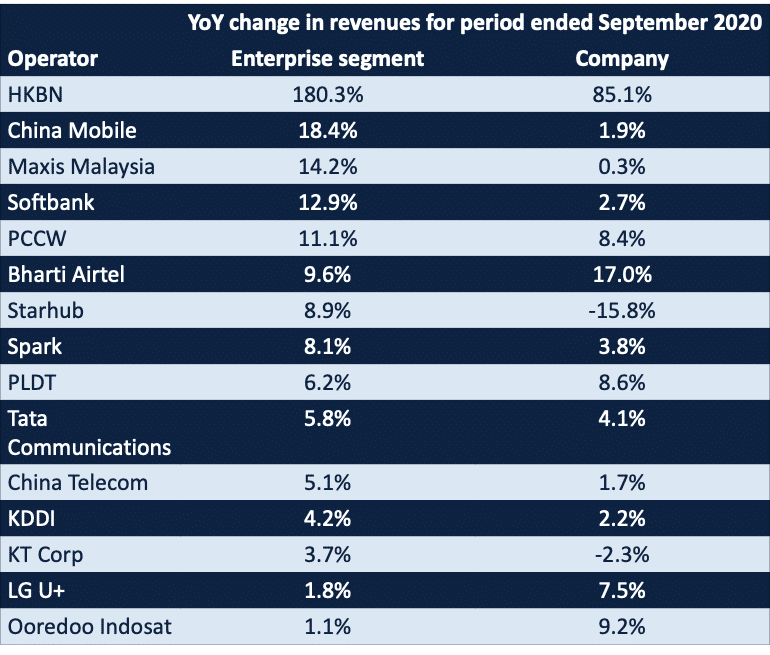

- Around 68% of operators analysed showed better growth in revenues from the enterprise segment compared to growth in telcos total revenues.

Table1: Telcos reporting highest growth in enterprise revenues, *9M 2020

Improvement in enterprises total revenue contribution

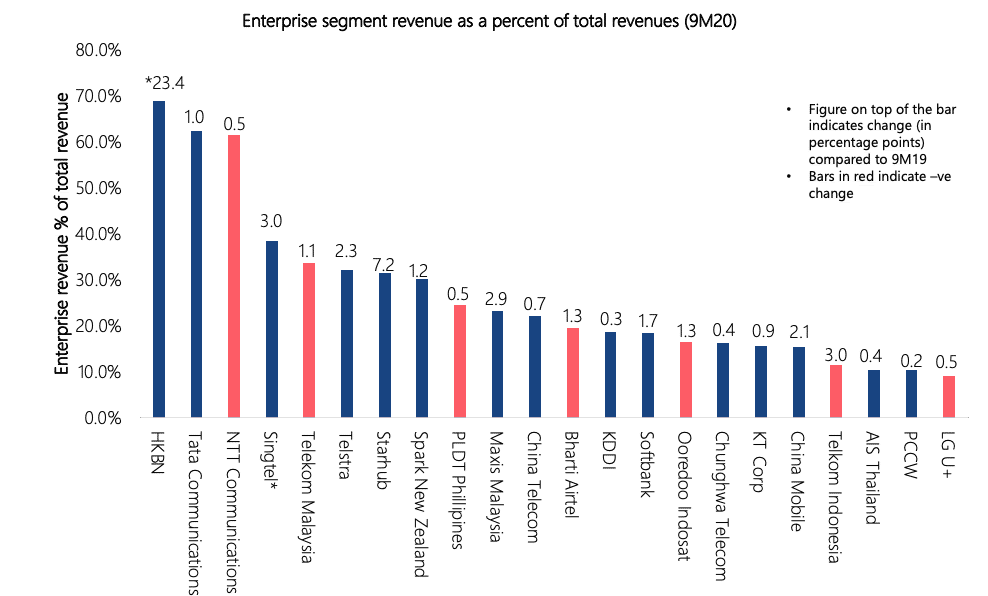

Operators have maintained different approaches in addressing growth from the B2B (business-to-business) segment. This is visible from the vast differences in contribution of enterprises to total revenue. The variation is from 10% to over 60% across operators. However, majority operators recorded an increase in the contribution of enterprises during the first nine months of 2020. Hong Kong based HKBN was particularly exceptional due to the acquisition of Jardine OneSolution Holding (JOS). As a result, contribution of the enterprise segment improved by 23.4 percentage points between 9M 2020 and 9M 2019 for the operator.

- Only a quarter of total operators analysed recorded marginal declines in contribution of enterprise businesses.

Figure1: Enterprise segment revenue as a percent of total revenues, 9M 2020

Cloud, security, and service management emerged as growth categories

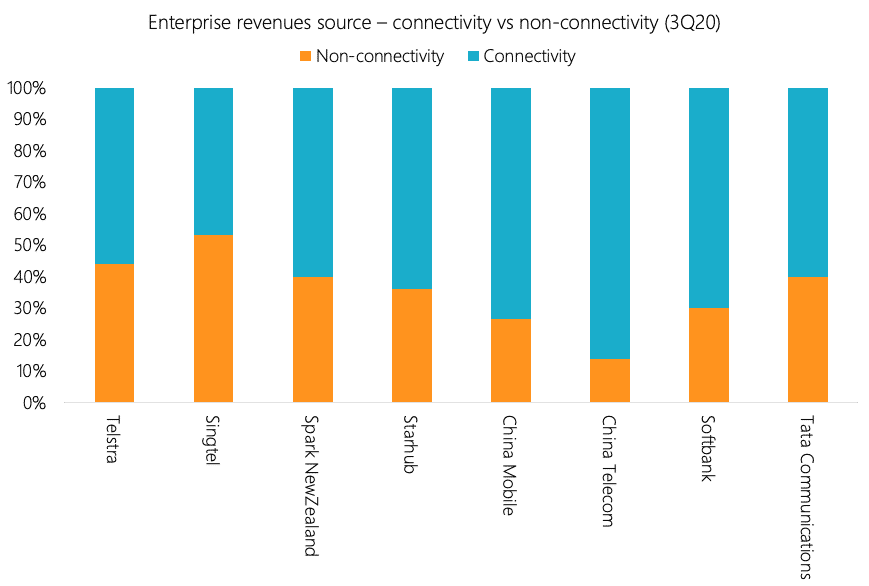

In our analysis, we find that income from non-connectivity services still form a small share of telco enterprise revenues. On average, about 65% of enterprise revenues are from connectivity services. Only a handful of telcos have been able to scale non-connectivity services, in particular cloud, security, and vertical solutions to diverge the risks of shrinking connectivity revenues. Selected operators, as shown in figure 2 who report non-connectivity revenues, have managed to grow in adjacent segments covering cloud, security, and vertical solutions, among others.

Figure 2: Enterprise revenue source – connectivity vs non-connectivity (3Q 2020)

Operators in China grew fastest in cloud revenues

Few operators have started reporting revenues from cloud services. Among those who have disclosed, China Mobile and China Telecom have performed significantly well.

- For China Mobile, cloud revenues increased by more than 500% year-on-year for the first half of 2020.

- China Telecom also reported a modest increase of over 30% Y-o-Y in cloud revenues.

While telco presence is limited due to the aggressive scaling of global cloud giants (Tencent and Alibaba in the case of China), the service segment has slowly grown in its contributions to their enterprise revenues. Chinese operators are winning by addressing new-use cases through the integration of cloud, edge, and networking services.

Table2: Growth in non-connectivity revenues for noted APAC operators

| Operator | Growth in cloud and other non-connectivity services |

| China Mobile | For the first half of 2020, mobile cloud revenues increase to CNY4,460 million (US$693 million). Cloud revenues increased 537% Y-o-Y. |

| China Telecom | Cloud revenues increased to CNY4,657 million (US$723 million) at end June 2020, growing at 30.4% Y-o-Y. |

| Tata Communications | Hosting services grew 13% Y-o-Y for the nine-month period, ending in September 2020. |

| KT Corp | Revenues from cloud and related services such as AI/ML increased 17.0% Y-o-Y. |

| Telstra | Cloud revenues declined 5% Y-o-Y for the first half of 2020. |

| PCCW | Revenue from cloud solutions and infrastructure grew by 21.2% Y-o-Y for first half of the year. |

| Singtel | ICT revenues increased 6.0% Y-o-Y for six months, ending on June 2020. |

| Starhub | Security revenues improved 46% Y-o-Y, driven by acquisitions. |

Digital transformations and teleworking fuel cloud growth for others

Growth in cloud revenues was not limited to China. Many other regional telcos including AIS in Thailand, Softbank in Japan, Spark in New Zealand, and KT Corp in Korea saw cloud revenues expand during the pandemic. Enterprise digital transformations remained a key driver, alongside increased teleworking. Telcos helped enterprises migrate to cloud-based communications and collaboration applications. Transforming traditional businesses to digital natives, for instance dine-in restaurants to on-line food delivery chains, also involved migrating workloads to cloud environments. Telcos have delivered networking services to enterprises; having cloud and security as part of the telco portfolio is helping them position themselves distinctively as end-to-end solutions providers.

Operators continue partnering with public cloud providers

These partnerships are aimed at the co-development of solutions for enterprises.

- Reliance Jio and Microsoft: As part of a strategic investment in Jio Platforms, the deal will see RJIO deploy Microsoft’s Azure platform in its data centres. The operator will develop a range of cloud-based productivity, collaboration, and business applications specific to the needs of Indian enterprises. Reliance Jio is integrating its own solutions with Microsoft’s offerings that are already used by many organizations.

- NTT and Microsoft: The two companies formed a multi-year strategic alliance to bring together NTT’s capabilities in managed services, ICT infrastructure, and cybersecurity with Microsoft’s cloud platform and AI technology. NTT built digital solutions to provide more secure application access between edge and the cloud.

- Telstra and Microsoft: These two partners are collaborating to develop new industry solutions in areas such as asset tracking, supply chain management, telematics, and smart spaces. The alliance is also exploring the implementations of digital twins for Australian businesses.

- Ooredoo Indosat and NetFoundry: Together, the two developed ‘Network-as-a-service’ offering.

IP-VPN and business communications applications also grew

The traditional communications segment includes MPLS WAN, IP-VPNs, ethernet, DIA, leased lines among other enterprise fixed and mobile connectivity services. The segment accounts for over 65% of telco revenues from enterprises. Where operators reported declined in connectivity revenues from business customers, demand for virtual private networks (VPNs) and business communications applications such as unified communication suites remained strong.

Acquisitions aid in building system integration and security capabilities

Telcos continued to gain momentum in the enterprise segment with relevant acquisitions. The year was marked with a few significant ones:

- For instance, Hong Kong’s HKBN acquired JOS to strengthen its capabilities as a fully integrated provider of ICT solutions.

- AIS and Starhub also added similar capabilities as they snapped Fortitude Technology and Strateq respectively.

Starhub has expanded its regional presence to Malaysia, Hong Kong, Thailand, and China with the acquisition. The telco also benefits from Strateq’s experience in developing sector- specific IT solutions for healthcare and oil and gas verticals.

Singtel, Starhub, and Softbank have strengthened their capabilities in delivering security services in an evolving services landscape:

- Softbank’s investments in online cybersecurity firm Cybereason have helped the telco in achieving twice the growth in security revenues.

- Starhub also accelerated cybersecurity business growth through Ensign. As per the company estimates, Ensign holds a 16% share of the local security market in Singapore.

- Starhub has recently collaborated with ADVA to strengthen its managed security services portfolio.