COVID-19 impact on telecoms – resilience in business performance?

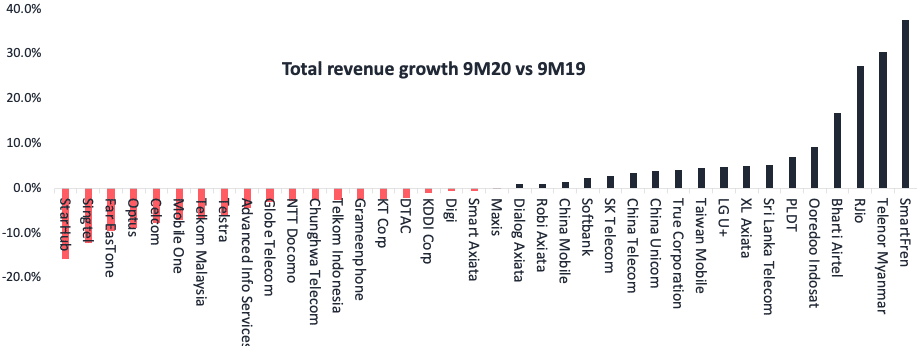

APAC telcos proved resilient but not immune to the COVID-19 impact. The effects of COVID-19 were varied based on a country’s success at containing the virus. Pressure continued to build as high-margin roaming services hit rock-bottom, as did revenues from overage charges and device sales. Retail stores closures slowed down new subscription additions. At the same time, stay-at-home policies, remote working, and online schooling made broadband the lifeline for households and communities. Data usage remained at least 30% higher compared to pre-COVID lockdowns. Strong performance of emerging markets and China kept the momentum going for APAC operators.

Core vs non-core services for telecom operators

The discussions on core vs non-core telecoms services and assets continued through 2020. Structural separation continued, splitting telecom operators into two entities: an infrastructure operator and the customer-facing business. The measures count as steps towards addressing financial pressure faced by operators in the face of 5G and the need for heavy investments in fiber infrastructure.

There are many examples from APAC, including Reliance Jio and Bharti Airtel, who carved out tower and fiber businesses to establish separate investment funds. Others include Telkomsel, XL Axiata, Optus, and Telstra. For many, 5G is a trigger point as it is likely to drive up network ownership costs with densification and fiberization of networks. The idea of having a much leaner consumer-facing business and establishing two separate (and independent) asset classes is driving the restructuring decisions.

Service provider race to being self-sufficient

In the 5G era, operators are focusing efforts where they matter most. It is softwarization of network functions to achieve agility and efficiency in network architectures. New age telecoms service providers, the likes of Rakuten and Reliance Jio, are driven by engineering. Their vision for a telco supports building 5G core and RAN functions within the telco community.

Access to the right resources, for instance Rancore and Radisys in case of Reliance Jio and Rakuten’s investments in Altiostar, is helping them achieve this vision. However, most other South East Asian telecoms operators lack the required internal capabilities for driving such innovations. They will continue to rely on technology partners, which may also be another telecoms service provider.

Hyperscalers – compete vs co-operate

With businesses facing COVID-19 led interruptions, hyperscalers – the large public cloud providers – really stood out. Each reported strong growth momentum during 3Q20. Microsoft, Google, and Amazon recorded YoY cloud revenue increases of 31%, 45%, and 29% respectively for the quarter ending September 2020. Where hyperscalers locked horns to dominate the cloud opportunity, an interesting development was that of the increasing focus on telco partnerships.

- There are twofold benefits – an opportunity for cloud providers to grow revenues from the telecoms vertical and also to leverage on each other’s infrastructure. For telecoms service providers increasingly betting on edge services to strengthen growth from 5G B2B use cases, cloud providers can bring the required scale to help them reduce overall infrastructure costs.

- However, many questions remain unanswered. Questions include maturity of telco edge infrastructures, clarity on scalable use cases, and the nature and the role of these partnerships in driving service provider revenues.

Ensuring network resilience with shifting traffic patterns

When most of APAC was locked down in early 2020, the impact on service providers was drastic. Data traffic surges were accompanied by shifts in traffic patterns. There was no distinction between peak and off-peak traffic as demand for data remained consistent throughout the day and the week. Service providers noted a massive shift in traffic demand moving from central locations hosting offices to residential areas. The pandemic highlighted the importance of building scalable, resilient, and automated network infrastructure everywhere.

Capex and opex dilemma

Telecom networks remained resilient, sustaining traffic increase between 20% and 100%. However, operators were faced with decisions to augment network capacities resulting in bringing forward some capex investments. Governments, regulators, and other stakeholders supported these spikes with a range of measures such as temporary allocation of additional spectrum and switching to standard definition for video transmission.

5G progress – COVID-19 disrupted supply chains

Delayed device launches (iPhone) impacted 5G momentum as operators are now resetting customer expectations of 5G. Smartphone shipments declined globally and across the region. While the first few months were impacted by disrupted supply chains, continued trends in the latter half of the year reflected weakened consumer confidence and the pandemic’s impact on spending. In some countries, volatility in supply chains also impacted network rollouts and delayed 5G spectrum auction.

Heavy regulations & government interventions

An on-going debate regarding the security of telecommunication infrastructure encouraged governments globally to intervene with the rollouts of next generation 5G networks. Clean network policies set by many governments limited vendors that are classified as low risk on network security. Governments even introduced regulations and framework on slowly phasing-out any existing network equipment from the high-risk vendors.

Huawei and increased geopolitical issues

As a result, industry noted an introduction of new suppliers and open RAN solutions to supply chains. For instance, many challengers, including vendors from Japan, reinforced efforts to expand their global footprints. In countries such as India, discussions led to increased focused on building self-reliance in technology. The focus includes both building networking equipment manufacturing and testing capabilities.

In the next article, we are discussing Top 5 opportunities on a telco CEO’s list in 2021.