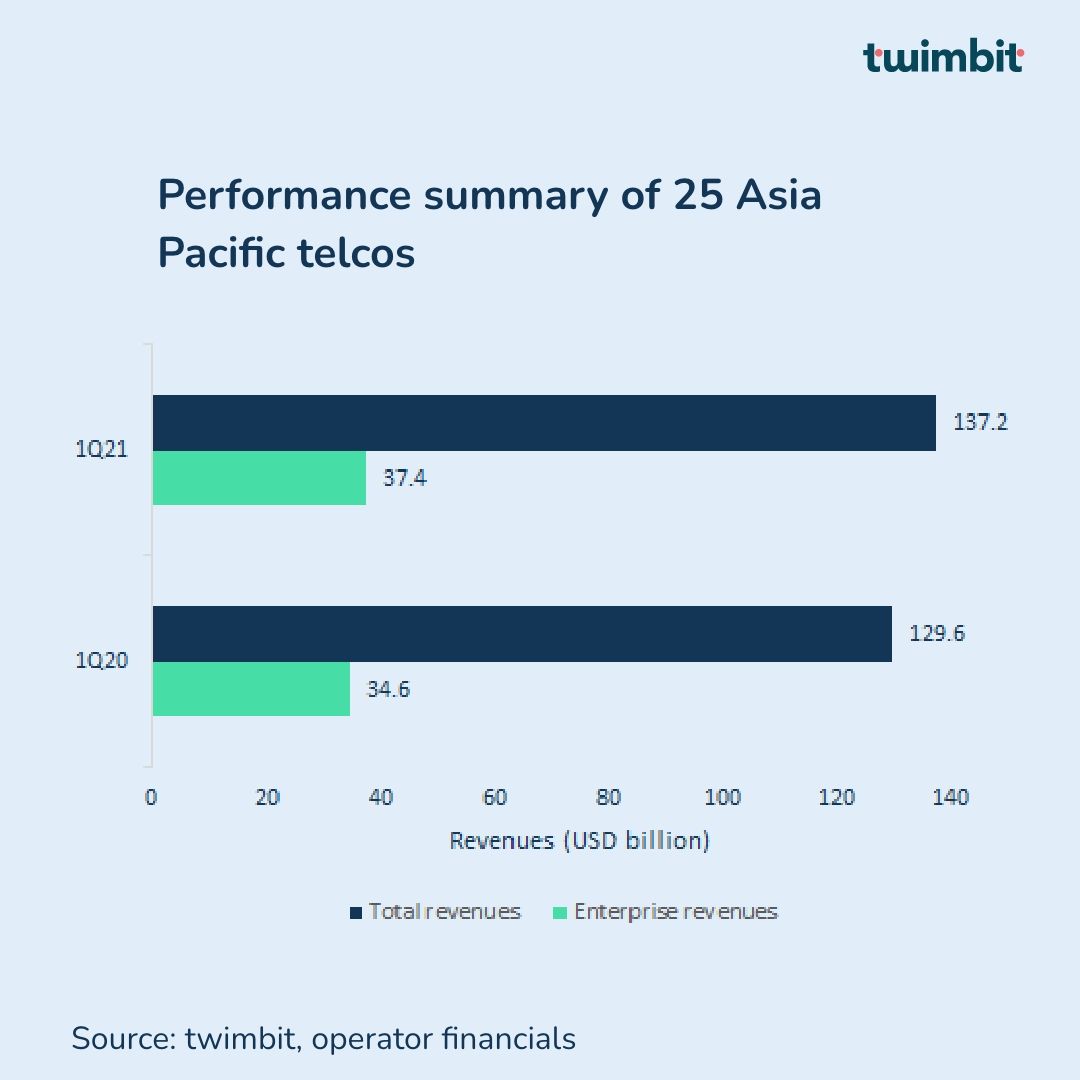

In this report, we analyse the growth, performance, and scale of enterprise business for 25 telecom operators in the Asia Pacific region during the first quarter of 2021. Overall, the operators recorded a better performance in 1Q2021 compared to 1Q2020, suppressed due to the pandemic’s onset.

Operators with enterprise business segments recorded USD 37.4 billion in revenues from business customers in this particular quarter. This translated to 8.1% YoY growth in revenues from these services. The growing focus of telcos on the enterprise business helped improve their average share of enterprise to total revenue from 26.6% in 1Q2020 to 27.7% in 1Q2021.

Figure 1 shows the 1Q2021 enterprise performance summary for these 25 APAC operators

Below are the highlights for telecom enterprise business in the Asia Pacific in 1Q2021

#1 Improvement in the enterprise’s total revenue contribution

- Overall, in 1Q2021, the 25 operators added net new USD 7.3 billion in revenues. The enterprise segment contributed USD 2.8 billion, driving about 37% of the net revenue increase.

- 76% of the total net new revenues of US$2.8 billion were from two leading operators. China Mobile contributed USD 1.1 million, and Nippon Telegraph and Telephone Corporation (NTT) added another USD 0.9 billion.

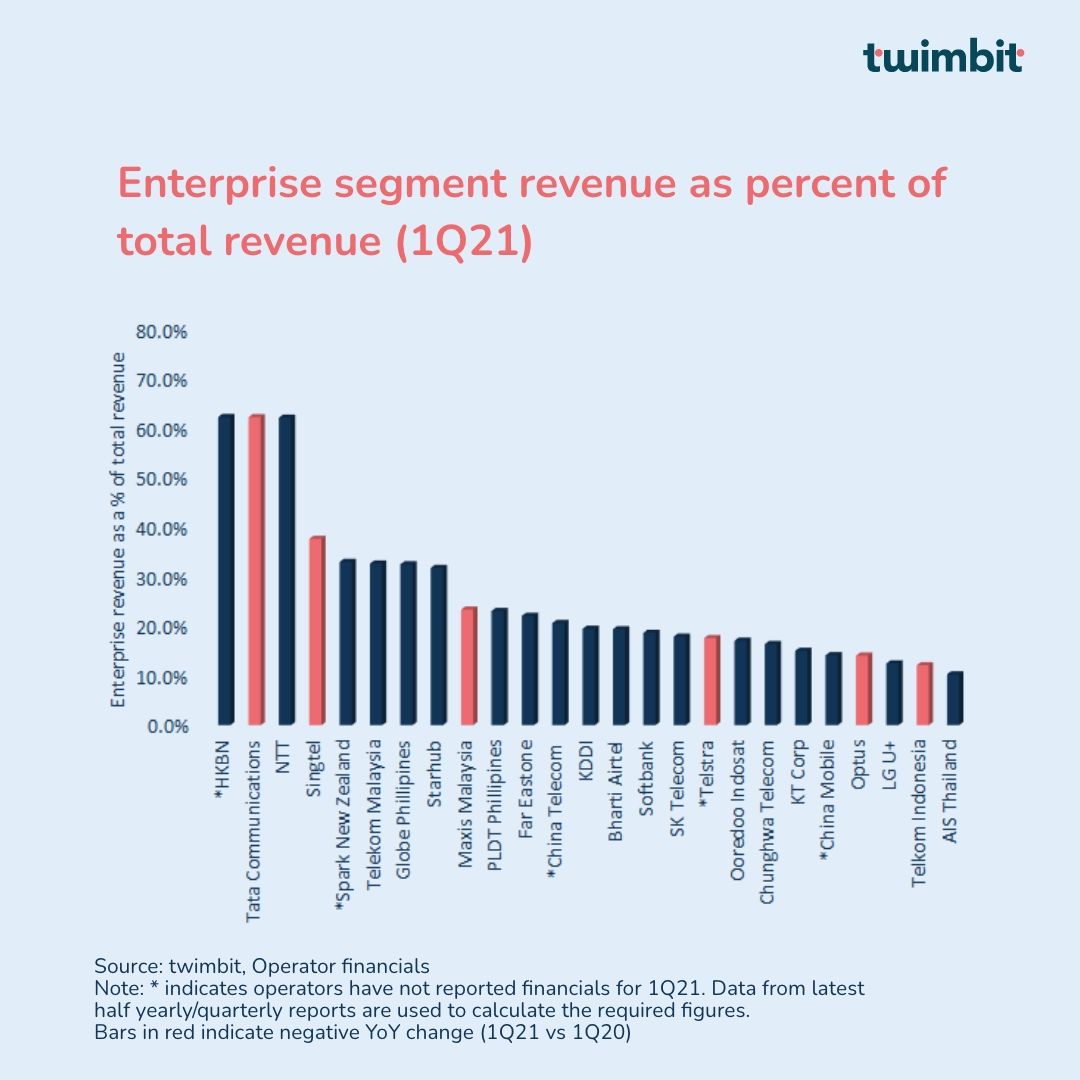

- Enterprise contribution to total revenues among the operators vary significantly, from 10% to 62%, with HKBN, Tata Communications and NTT Comms sitting at the higher end, as shown below in Figure 2.

- Tata Communications and HKBN continued to expand their enterprise portfolio by collaborating with global companies like Google Cloud, Cisco, PwC Hong Kong, Fuji Xerox, and many others. The focus of these collaborations is expanding services in areas including cloud, cyber security and IoT.

- AIS Thailand has a relatively weak enterprise business. The YoY growth of the enterprise segment was 3.1%, due to price competition, coupled with impact of seasonal ICT projects.

Figure 2 shows enterprise revenues as a per cent of total revenues for 1Q2021

#2 Higher growth in enterprise revenues compared to total revenues for top performers

Digital transformation of enterprise customers has been the driving factor of higher growth in enterprise revenues. Telcos have launched new offerings and solutions for their corporate customers in the digital space through various partnerships and collaborations.

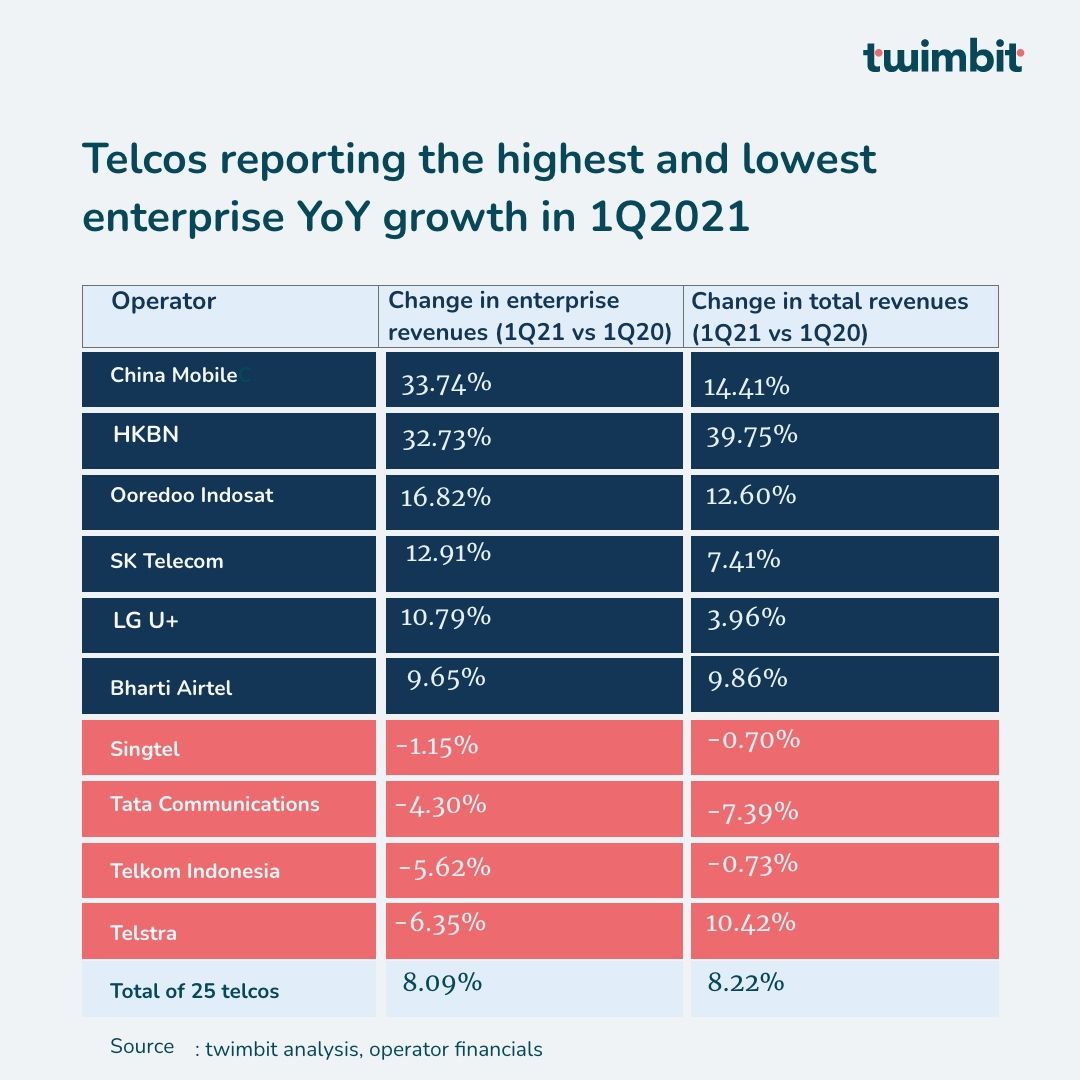

We noted that China Mobile, Ooredoo Indosat, and LG U+ showed an excellent turnaround in their enterprise business in 1Q2021.

Table 1: Telcos reporting the highest and lowest enterprise YoY growth in 1Q2021

- The major driver for the 34% enterprise revenue growth for China Mobile is private cloud offerings. The revenue scaled up substantially for DICT (Data Information and Communications) services, coupled with mobile cloud, which increased at around 270% YoY in 1Q2021. In addition to this, China Mobile has also focused on upgrading its “Network + Cloud +DICT” services by strengthening its partnership with over 20 global leading cloud service providers to offer integrated solutions to its enterprise customers. The move enabled the telco to expand globally through mCloud.

- HKBN managed to add new enterprise customers and collaborated with various companies like Microsoft Hong Kong to deploy Microsoft’s suite of applications, cloud platform Azure, and an all-in-one business management solution, particularly for SMEs.

- Ooredoo Indosat launched dedicated mobile and fixed plans targeting the underpenetrated SME market and SOHOs. It also recently launched the Enterprise Edge service in collaboration with VMware, a managed service to boost cloud adoption.

#3 Partnerships and collaborations are driving growth for telecom operators

Telecom operators are expanding their enterprise partner ecosystem to run joint operations, expand the reach and reduce costs by offering enterprises innovative solutions such as cloud, IoT and mobility.

- AIS

- AIS Business collaborated with IBM Services to launch Open-Source Support Service on Local Cloud, enabling organisations of all sizes to scale up and innovate, coupled with addressing data privacy challenges.

- HKBN

- HKBN entered into a strategic partnership with Achiever Technology Limited and introduced Remote HR solutions for SMEs to migrate their HR processes to the cloud, optimising costs and increasing accuracy.

- To tap the underpenetrated SME market, HKBN also joined forces with Microsoft Hongkong and PwC Hong Kong to offer them a bundled suite of Microsoft applications and cybersecurity solutions.

- Singtel and Optus

- Singtel and Optus collaborated with AWS to expand their 5G ecosystems for enterprises to develop low-latency 5G solutions such as robotics, drones, AI, etc., on their Multi-access Edge Compute (MEC) infrastructures. These MEC will leverage AWS Outposts, a solution that allows Singtel to operate a full suite of AWS tools and services on its premises.

- SK Telecom

- SKT collaborated with AWS to launch SKT 5GX Edge for their enterprise customers to build innovative services in ML, IoT, etc.

- Maxis

- Maxis partnered with PETRONAS Dagangan to offer converged business solutions in security and sustainability to enable its enterprise customers to optimise cost and increase efficiency.

#4 Few large incumbent operators continue to see a decline in the enterprise business

- Telstra participates in a domestically saturated market. Telstra Enterprise revenue decreased by 6.35 per cent, largely due to declines in domestic revenues from Data & IP and legacy fixed products, which increased international enterprise revenues could not offset.

- Telkom Indonesia witnessed a decline in its enterprise business revenues as the company was in the process of eliminating products and services with lower margins to ensure business sustainability.

- The enterprise revenues for Tata Communications witnessed a YoY decline because of a dip in the enterprise voice revenues, coupled with challenges posed by COVID-19. These factors resulted in longer deal conversion time and execution cycles post 1Q2020.

- The enterprise revenue for Singtel noted a reduction of two per cent in constant currency terms due to intense price competition and decline in legacy voice revenue, because of weak business conditions during COVID-19.

The 1Q 2021 performance review of Asian Telecoms operators is also available here for a read.