Telcos are seeking growth beyond their core (connectivity services). They are exploring opportunities in adjacencies (non-connectivity). The Asia Pacific region, with its diversity, offers a fascinating view of the varying strategies adopted by telcos amidst the growing confidence that they can win in establishing digital businesses. This insight provides you with a perspective on which Asia Pacific telco’s are leading the way. We recognize and benchmark the Top 10 telco’s to ace growth in non-connectivity.

Our methodology

- We studied 40 telcos across 15 key markets that provide consistent, detailed updates on their business progress. 24 out of the 40 telcos had made progress in establishing and reporting their non-connectivity business revenues.

- Next, we defined non-connectivity as services excluding voice, fixed-line, broadband, and enterprise connectivity (IP-VPN, SD-WAN, etc.). It is broadly classified into four pillars — enterprise, content & media, e-commerce, and others.

- Finally, we identified the top 10 telcos to ace non-connectivity revenues in 2021. Since all the telco’s compete in different geographic markets with varying scale, we benchmarked them across three variables, viz., growth, absolute new revenue added and % of non-connectivity to total revenue mix.

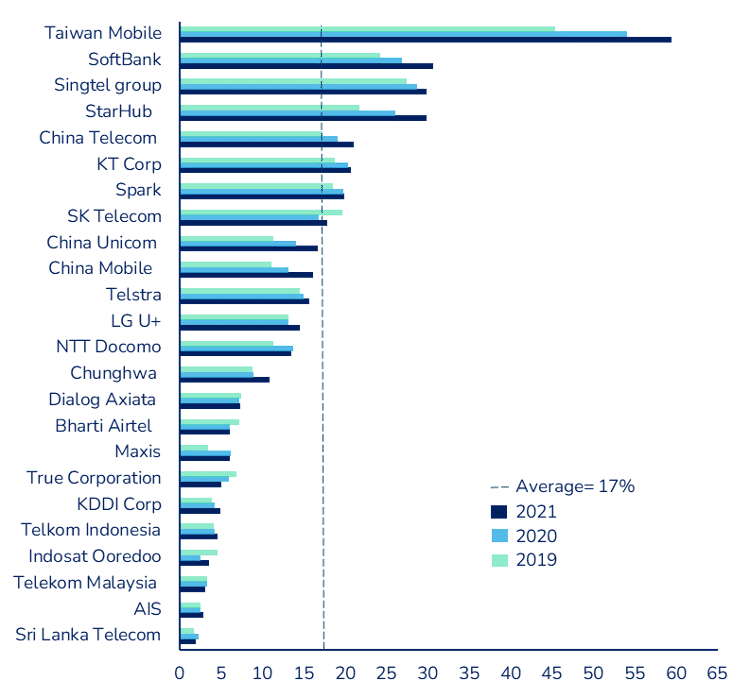

Figure 1: % of non-connectivity revenues to total revenue

twimbit 4 pillars of non-connectivity services

We classified non-connectivity services into 4 distinct categories, defining them as ‘twimbit’s 4 pillars of non-connectivity services’

| E-commerce Being early to market is a necessary prerequisite for success in this category. We have observed a tailwind in operators having their online portals to facilitate commerce. Many telcos are also using their stores to enhance the e-commerce trading volume. |

| Enterprise non-connectivity (Cloud, managed services, IoT, cyber security) The Enterprise business represents the must-win segment for most service providers, especially with the advent of 5G. A detailed twimbit study on the enterprise segment is available here. |

| Content and Media (IPTV, pay TV, content leasing, OTT services) Bundling content with broadband connectivity has helped telcos across the board. Many telcos have invested in developing and scaling localised content. Partnerships with Netflix, Amazon Prime and Disney has been extensively pursued across the region. |

| Others (Financial services, digital marketing, analytics, telehealth, education) Payments represent a new ongoing opportunity (top 5 telcos to ace financial services). Whereas gaming, digital marketing, and other non-connectivity areas have seen some success in specific markets. |

twimbit’s Top 10 operators to ace non-connectivity revenues

The objective – identify the top 10 operators who have excelled in providing services beyond connectivity. To arrive at the top 10, we scored them on three parameters, giving each parameter equal weightage (33%).

- Absolute change in revenue from non-connectivity services between 2020 to 2021.

- Percentage change in non-connectivity revenues from 2020 to 2021.

- Revenue from non-connectivity services as a percentage of the total in 2021.

Table 1: Overview of non-connectivity revenues for APAC telcos, 2021 vs 2020

| Rank | Telco | FY 2021 USD million | FY 2020 USD million | Absolute change $ million | % change Y-o-Y | Non-connectivity % of total (2021) |

| 1 | SoftBank* | 15,698.0 | 12,481.6 | 3,216.3 | 25.8 | 30.6 |

| 1 | Taiwan Mobile | 3,341.1 | 2,586.2 | 754.8 | 29.2 | 59.4 |

| 2 | China Mobile | 20,544.2 | 15,155.7 | 5,388.5 | 35.6 | 16.2 |

| 3 | China Telecom | 13,915.2 | 11,298.9 | 2,616.3 | 23.2 | 21.1 |

| 4 | China Unicom | 8,220.0 | 6,408.0 | 1,812.0 | 28.3 | 16.7 |

| 5 | StarHub | 450.4 | 392.2 | 58.2 | 14.8 | 29.8 |

| 6 | SK Telecom | 2,602.2 | 2,352.5 | 249.7 | 10.6 | 17.9 |

| 7 | Chunghwa | 823.0 | 671.4 | 151.6 | 22.6 | 10.9 |

| 8 | Singtel group* | 3,441.0 | 3,317.4 | 123.6 | 3.7 | 29.9 |

| 9 | LG U+ | 1,742.3 | 1,543.6 | 198.6 | 12.9 | 14.5 |

| All APAC total | 87,263.4 | 72,263.9 | 14,999.4 | Avg. 20.8 | Avg. 17.0 | |

| Top 10 total | 70,777.4 | 56,207.6 | 14,569.6 | Avg. 25.9 | Avg. 20.4 |

Key takeaways

#1 Non-connectivity revenue grew 3.2X more than overall industry revenue growth

- 20.8% growth in non-connectivity revenue in 2021 (YoY) compared to 6.5% overall revenue growth.

- Only 13.7% growth of non-connectivity revenues in 2020.

- 12 telcos generated over a billion dollars each from non-connectivity business, with:

- Taiwan Mobile achieving the highest contribution to the total business at 59.4%,

- China Mobile added the highest new revenue of USD 5.3 billion, growing at 35.6%.

#2 Growth from new geographies as e-commerce & OTT are easily scalable beyond domestic boundaries

- Network-based services are often limited to the domestic market as regulations and licensing requirements were needed to compete. Digital services, on the other hand can have a global reach. Telcos are making way to new markets by introducing services like OTT, e-commerce, payments, etc.

- Momo by Taiwan Mobile is the second largest e-commerce platform in Taiwan. It contributed 56.6% to total revenues in 2021. After capturing the domestic market, it moved to other countries in South East Asia (SEA). In 2014, Thailand became the first stop via a joint venture with TVD. They established TVD Shopping Co., the second-largest TV shopping channel in Thailand. Momo has also developed businesses in Malaysia, the Philippines and Vietnam.

Figure 2: Revenue breakdown of Taiwan Mobile

- PCCW launched Viu, an OTT video service in Hong Kong, in 2015. It expanded significantly and is now available in 16 markets across Asia, Africa and the Middle East. It has over 58 million monthly active users and noted a tremendous growth of 58% in paid subscribers, reaching 8.4 million in 2021.

#3 SoftBank is building its growth prospects as a SUPER APP

Telcos are leveraging the existing assets to strengthen their offerings. These include the subscriber base, consumer insights, brand strength to build SUPERAPPS. This is seen as a growth strategy by many. See below a discussion on if SUPERAPPS are a way to winning wallet share for telcos.

A SUPERAPP is defined as one that offers at least 3 to 4 unrelated services originating from different business segments.

Here is an example of a SoftBank-owned LINE app that literally leaves no services uncovered.

In March 2021, SoftBank integrated its Yahoo Japan business with LINE corporation. The new business ‘Yahoo Japan/LINE’ comes under Z Holdings, a subsidiary of SoftBank. Together, ‘Yahoo Japan / LINE’ offers over 200 services and is now the largest Internet company in Japan.

LINE originally launched as a chat app in Japan in 2011. Progressively, it turned into a social media platform attracting 68% of Japan’s population. As of today, LINE is both the biggest social app in Japan and the most popular social network in Thailand. The volume of content on the app is unimaginable, and there is little that LINE does not include. Here is a non-exhaustive list of services offered by LINE:

- Voice & video calling

- E-commerce & indoor shopping malls

- Payment & other financial services

- Food delivery & pickup facilities

- Gaming, news, music & much more

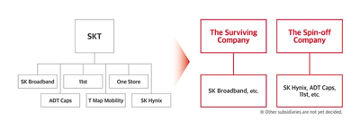

#4 SK Telecom organises for a successful digital business

Every business segment invites unique opportunities and challenges. Taking advantage of overlapping assets and yet having a separate vision for each segment are two sides of the same coin.

Non-connectivity businesses for SK Telcom (media, security and commerce) have been growing briskly. In fact, it summed up to 24% of SKT’s total operating income in 2020.

In 2021, SK Telecom announced a new organisational structure separating its traditional and growth businesses, rebranding itself as an “AI & Digital Infrastructure Service” company, with the spin-off company as “ICT Investment Company”.

The objective of separation is clear, the surviving company will solidify its position as a premier telecommunications firm. On the other hand, the spin off company will indulge in diverse investment activities in the semiconductor industry, both domestic and overseas.

#5 Enterprise business has emerged as growth engine

Telcos have made decent progress in the overall enterprise segment (inclusive of connectivity services). A twimbit analysis of 25 telcos reveals that the average enterprise share to total revenue was 27.7% in 2021.

Enterprise is the largest and the most important opportunity for telcos to prioritise. Services like cloud, IoT, security, and managed applications are the future growth avenues. Telcos in Singapore have done well in growing the enterprise business portfolio.

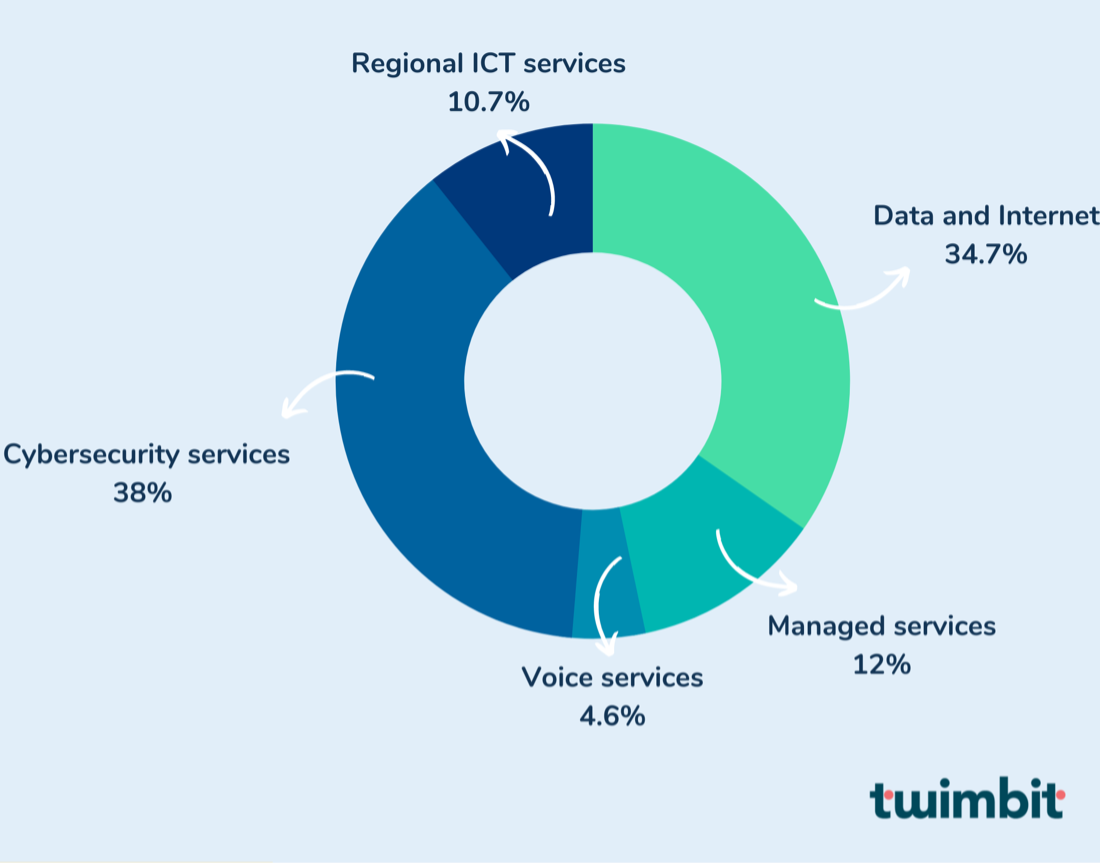

Figure 3: Enterprise revenue mix for StarHub 2021

This report considers only the non-connectivity services from the enterprise segment. In the case of StarHub, we considered its managed services, cybersecurity services, and regional ICT services.

StarHub in March 2020 bought a majority stake (88%) in ‘Strateq’, a Malaysian-based data firm. This has helped grow regional ICT services by 128% (YoY). Additionally, the cybersecurity segment also performed well in the overseas market, growing by 21% (YoY)

A non-exhaustive list of services provided by Strateq includes:

- Healthcare information systems

- Retail fuel IT managed services

- Payment solutions

- Cloud and data analytics solutions

- Data centre services

- IT infrastructure projects

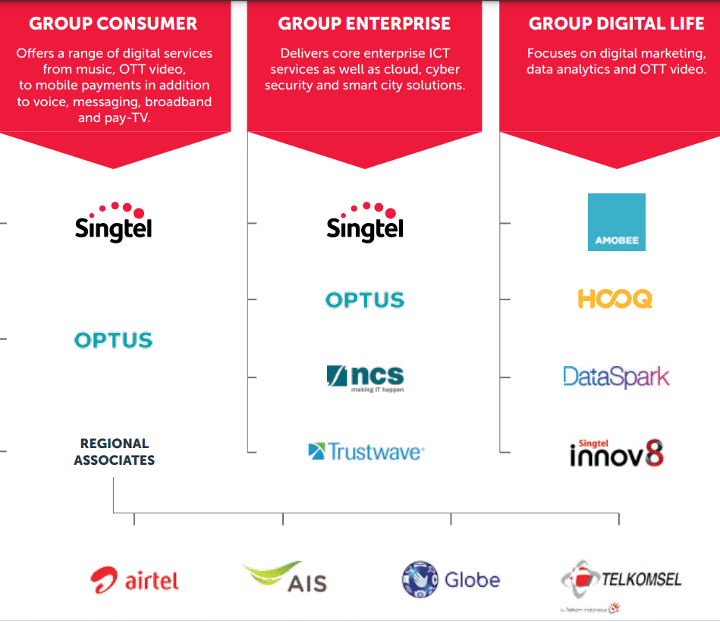

SingTel comes out as one of the most well-diversified telcos in the region. After witnessing a brief hiatus, the group enterprise and digital business are gaining momentum.

Figure 4: Business diversification of SingTel

#6 Building new growth businesses on top of data and data analytics

Telcos use data from customer interactions to provide corporate clients with big data services, business insights, and data consultancy. The result — is rich information on which to create precise consumer profiles, behaviour forecasts, and hundreds of microsegments, allowing for more focused marketing and lower customer acquisition costs.

Telkomsel runs 50-plus analytical models every month to identify the most efficient way to build a relationship with its customers. It has created a data analytics business that caters to a wide range of consumers in retail, finance, and even telecommunications. Few of the services include predictive customer insights, credit scoring, predictive analytics, geological insights, etc.