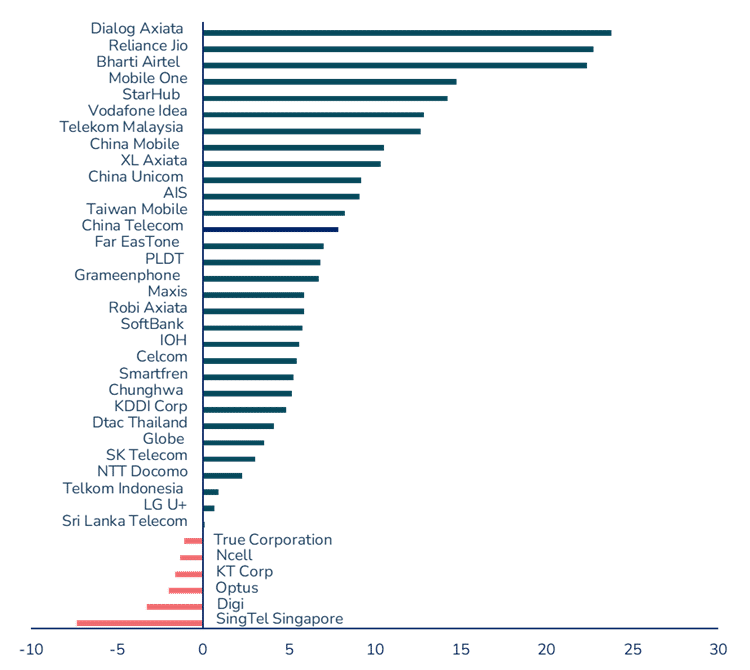

#1 Revenue highlights

- 37 of Asia Pacific’s leading telcos registered a combined revenue growth of 6.7 percent Year-on-Year (YoY) in Q3 2022. Aggregate revenues of these telcos totalled a commendable US$ 140.4 billion in Q3 2022.

- Quarter-on-Quarter (Q3 2022 vs Q2 2022) revenues declined 3.2 percent. This trend has remained consistent over the years. In Q3 2021, we had witnessed a decline of 3.9 percent from Q2 2021.

- 9 out of the 37 telcos achieved double-digit revenue growth. 85 percent of telcos registered a positive YoY revenue growth in Q3 2022 (refer to exhibit 1).

- At an aggregate level, the Asia Pacific telcos added US$ 9.3 billion in new revenues this quarter. China Mobile added the highest net new revenues in the quarter of US$ 3.2 billion on YoY basis.

- Dialog Axiata led with the highest growth rate of 23.8 percent YoY. It also recorded the highest growth in 2021 (YoY). The Sri Lankan telco registered growth across all three segments (mobile, fixed & TV). Rate revision for mobile tariffs was the key revenue driver.

- Indian telcos continued their strong growth trajectory in 2022. The top telcos (Bharti Airtel, Reliance Jio and Vodafone Idea) registered a growth of 17.1 percent in Q3 2022.

- SoftBank recorded the highest revenue change of 6.2 percent on a QoQ basis with net new revenues from Q2 to Q3 of US$ 736 million – an all-time high compared to its previous 6 quarters. Improvement in subscriber numbers and stability in the tariffs were key highlights.

- In what is a notable trend for Singapore, two of the telcos, viz., StarHub and M1 are in the top five fastest growing telcos in Asia Pacific, thanks largely to their growth in the Enterprise business.

- Acquisition of JOS (Singapore and Malaysia) by StarHub, completed on 3 January 2022 has helped establish a regional enterprise services business. Enterprise contributed to 37 percent of StarHub’s total business and grew by 16.3 percent in Q3 2022.

- The enterprise business for M1 grew 34 percent YoY in the first 9 months of 2022 (9M22) to US$ 196 million.

Exhibit 1

Percent revenue change for APAC telcos, Q3 2022

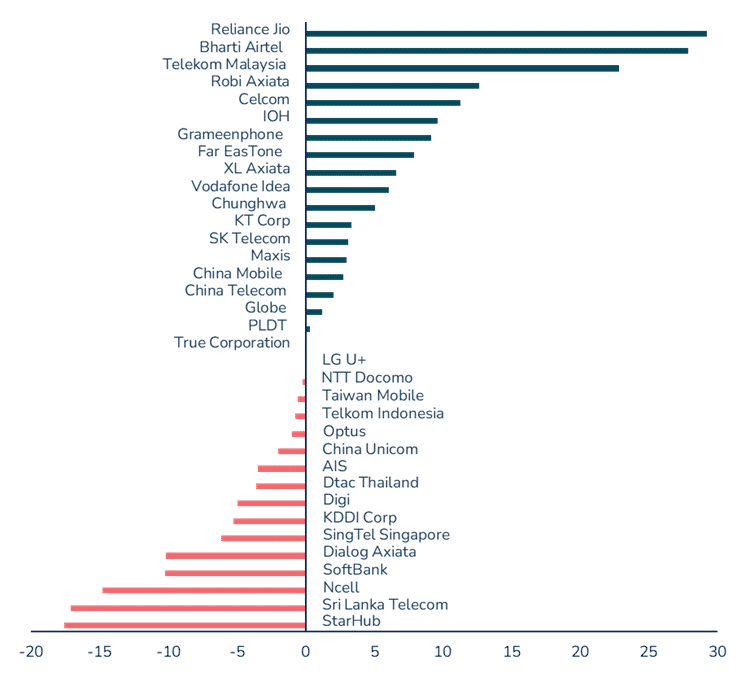

#2 45 percent of the telcos register a decline in earnings (EBITDA), despite notable growth in revenues

(refer to Exhibit 2)

- Indian telcos continue to show strong EBITDA growth. The tariff hikes helped uplift ARPU, positively impacting revenues and profitability

- Both Dialog Axiata and StarHub, which have seen strong revenue growth have posted a decline in EBITDA of 17.6 percent and 10.2 percent respectively. StarHub- OPEX increased by 19.9 percent mainly due to higher staff costs and marketing & promotion expenses.

- Telekom Malaysia combined a double-digit revenue growth with an improvement in EBITDA margin. Strong growth of ICT and bespoke solutions coupled with higher cumulative fixed broadband subscribers have augured well for this dominant incumbent telco in Malaysia. It recently secured a deal with a domestic service provider for comprehensive solutions comprising of co-location and data services. Demand from hyperscalers is expected to drive growth for the wholesale business in the coming years.

- Dialog Axiata- cost as a percentage of revenue increased from 57.6 percent in Q3 2021 to 69.2 percent to Q3 2022 influenced by higher direct expenses

Exhibit 2

% EBITDA change (APAC), Q3 2022

- Robi Axiata witnessed a strong consumption led growth. Data consumption surged from 4.3 GB/subscriber/month in Q3 2021 to 5.7 GB/subscriber/month in Q3 2022. Additionally, the data revenue improved because of higher 4G adoption and usage. 4G data users reached 27.6 million, a net addition of 5.2 million subscribers YoY.

- Celcom benefitted from higher prepaid revenues and contribution from new acquisition in its B2B unit.

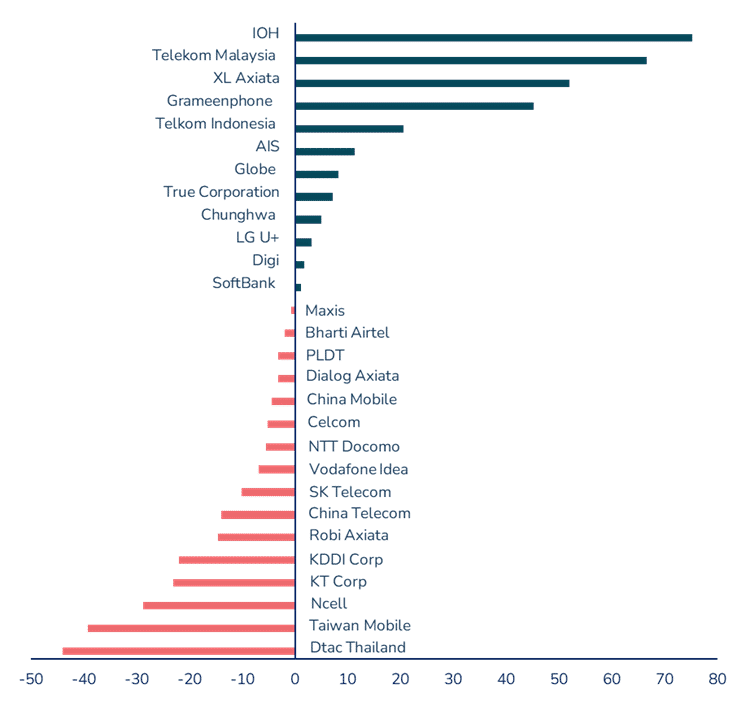

#3 CAPEX spending continues to slowdown

- More than 55 percent of the telcos charted a negative change in their CAPEX in Q3 2022 (refer to exhibit 3). The trend is consistent since the beginning of the year and is expected to continue well into 2023.

- There is growing momentum towards infrastructure sharing. The key markets of China, Japan, South Korea have passed the peak investment phase for 5G.

- 5G led CAPEX spending is expected to increase substantially in two of South Asia’s largest markets, viz., Indonesia and India in 2023.

Exhibit 3

Percent CAPEX change for APAC telcos, Q3 2022

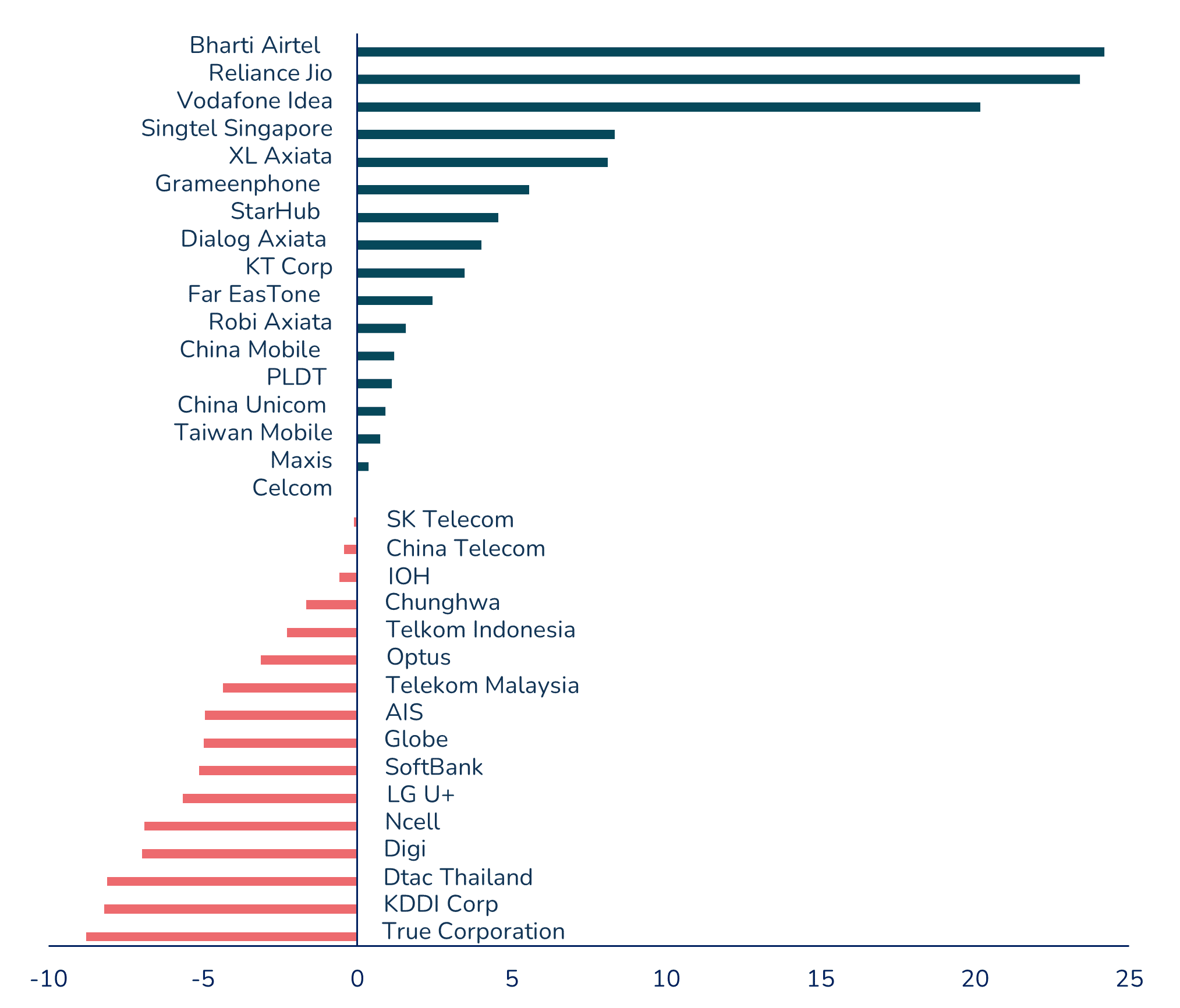

#4 Trends in ARPU

- The Indian market stands out from the rest of the 13 markets in the Asia Pacific region (refer to exhibit 4). Price hike had a direct positive impact on the ARPU for the Indian operators.

- SingTel Singapore reported an increase in ARPU of 8.3 percent, primarily due to the adoption of higher priced 5G plans

- Consumer preference in Thailand to migrate to lower tier data plans continued. All the three telcos registered an ARPU decline.

Exhibit 4

Mobile ARPU percent change for APAC telcos, Q3 2022

#5 Indian and Chinese telcos continue to ace the twimbit’s growth index

twimbit Growth Index benchmarks telcos based on two parameters

- Absolute change in revenue (US$ Q3 2022- US$ Q3 2021)

- Percentage change in revenue (YoY)

Exhibit 5

Net addition and percent revenue change for top 5 telcos, Q3 2022

| Telco | Country | Net new revenues (US$ million) | Percent change (YoY) |

| Reliance Jio | India | 585 | 22.7 |

| China Mobile | China | 3,242 | 10.5 |

| Bharti Airtel | India | 578 | 22.3 |

| China Unicom | China | 1,110 | 9.2 |

| China Telecom | China | 1,299 | 7.9 |

| Top 5 | 6,813 | 9.6 | |

| All APAC | 9,338 | 6.7 |

- The narrative of Indian and Chinese telcos acing growth continued for the third consecutive quarter.

- Chinese telcos have demonstrated exceptional use cases of 5G across industries such as manufacturing, healthcare, ports and gaming. They have set a benchmark for other telcos in the region with diversification into the B2B business and exploring areas like IoT and cloud.

- Besides the tariff revision, Indian telcos, especially Bharti Airtel and Reliance Jio have created a strong product/service eco-system. By integrating a suite of applications and services they have created a compelling proposition to build customer loyalty. Bharti’s relentless focus on improving network quality has helped gained over 11 million customers YoY in the Indian market. Jio’s robust partner eco-system has enabled it to build a strong base for growth beyond core connectivity services.