The financial services industry has experienced tremendous expansion and innovation in recent years. Investments from innovative business models such as neobanks and traditional banks have enthralled the industry. The question is, where do you acquire your wallet share? It’s no longer about product or service differentiation; it’s about owning the customer journey, which super apps, mobility businesses and payment providers contest. And customers want to see real, tangible results and influence. This is where digital ecosystems come in.

A digital ecosystem is a complex web, a network of stakeholders interconnected online, engaging digitally, and creating value for others. It has ties beyond the authority and sphere of influence of a financial institution. Although traditional banks are moving technologically forward and innovating, a major question remains, can banks win in building digital ecosystems?

To break down the topic and its relevance to ASEAN & Indian context, we invited

- Ketan Samani – CDO, China Financial Development Taiwan &

- Gaurav Goel – National Head, Startup/New Economy business, Yes Bank

They share their view of the opportunities and challenges while building ecosystems. Although we encourage you to listen to the engaging conversation in full, we have also presented a quick summary of the session.

.

We cover the following three themes in this session:

- How can banks build ecosystems and keep up with the increasing competition in the financial services industry?

- What are the challenges that banks face while building ecosystems?

- What are the measures of success for an ecosystem?

These are the key takeaways:

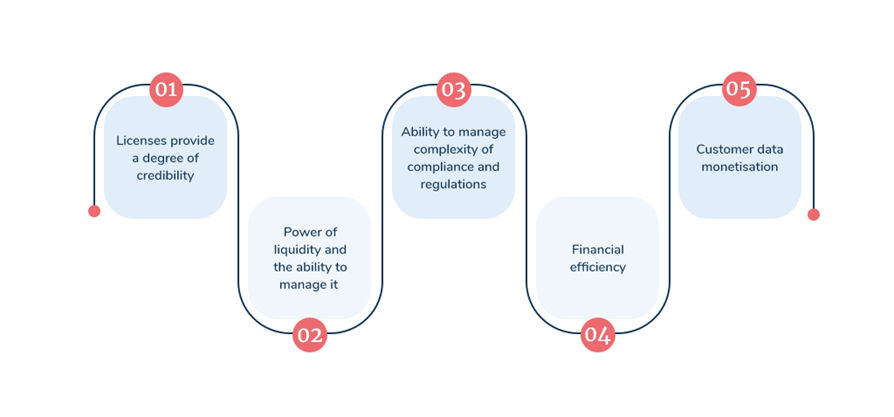

1. Banks bring 5 key values to the table

When it comes to the evolution of the Internet, mobile, and now digital, banks have always lagged behind fintechs. Yet, banks have tried to catch up, providing solutions to customers. If we go back ten years, close to 60% to 80% of banks in ASEAN did not have digital platforms. However, today, around 80% to 85% do. Because of the regulation and cadence in place, the banks are slowly but steadily reaping the benefits of digitalisation. Banks can bring 5 key values to the table, either independently or through partnerships, to develop an ecosystem:

- licenses provide a degree of credibility;

- the power of liquidity and the ability to leverage it;

- ability to manage the complexity of compliance and regulations;

- financial efficiency;

- customer data monetisation

Figure 1: 5 key values to develop an ecosystem strategy

While incumbent banks have lost some ground, they can still create ecosystems and compete with the competition from fintechs and technology platforms.

2. Banking is important; banks aren’t

In an ecosystem, there are three possible basic models. First, banks and financial institutions can be participants. The second possibility is that they are orchestrators. The third would be where they would build the entire ecosystem from scratch.

“Building from scratch” is not the strong suit of banks. From a technological standpoint, fintechs are unquestionably more agile in terms of speed. However, the bank can give other benefits, such as regulatory and compliance expertise, which could be advantageous in agility.

Because the ecosystem era is expanding exponentially, banks face many challenges. One of them includes data. Data is one of the areas in an ecosystem where banks will have to be really cautious when dealing with anyone. This makes data sharing and the purpose of data usage major concerns to focus on.

The other big concerns that persist are – how would banks be able to maintain their advantages while still being able to participate or orchestrate? And how can a bank become the ecosystem’s electricity? – because banking is important, banks aren’t.

3. Becoming an invisible bank

In terms of transactional facilitators, banks are enablers. Still, there are a lot of customer experience related services that occur in an ecosystem that has nothing to do with banking. And banks would have to acknowledge that; otherwise, governance would be difficult due to its complexity.

While banks are getting plugged in, embedded finance is becoming more prominent. In other words, banks are powering the system, but they are not visible. And it is in this way, through embedding finance, banks remain relevant and grow, despite being invisible.

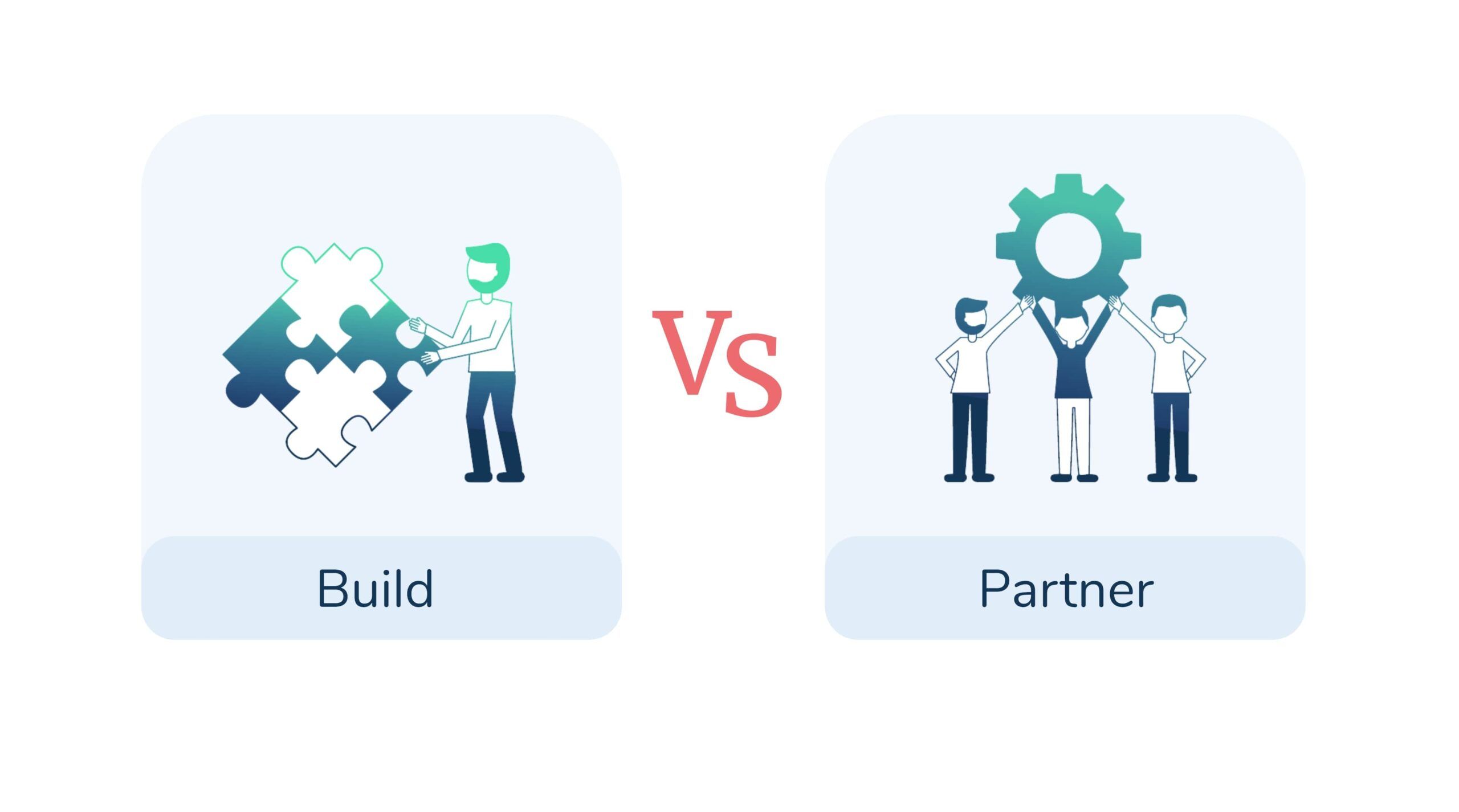

4. Build versus Partner

There are two opportunities for the fintechs and neobanks. First is owning the customer journey and being able to borrow on the balance sheet and lend the money themselves. Therefore, there is a need for a regulatory environment that empowers these new-age models to innovate and manage risks. Second, the fintechs and neobanks become front-end platforms and focus on distribution. They manage the customer experience, interface, and journey but leave the customer data and its assets as the responsibility of the regulated company. Hence, the ownership of the customer lies with the regulated bank.

Figure 2: What should be the bank’s ecosystem approach

However,a fintech’s agility can sometimes work against innovation, especially when there is a point of co-creation. To overcome this challenge, they should set up sandboxes and invite banks to co-create. Sandboxes bring cost-benefit analysis into the picture, reduce the cost and improve the efficacy of the model. If the co-creation journey is started together, the acceleration point can come in at the outset of ideating together. And the differing points of view can be rapidly put aside.

5. Ecosystem strategy plays a strong role in expanding in new geographies

In banking, there are three parties involved:

- the bank,

- the technology infrastructure,

- and a regulator, depending on the marketplace in which one operates.

It is necessary for an ecosystem to flourish across borders and not simply within one country. So being a sole orchestrator is very difficult for a bank. One usually needs to have well-known and well-designed partnerships to work cross-border and in different verticals (Healthcare, Telecoms, Manufacturing, Transport).

The major development is in having embedded financial systems that allow to plug and play with specific rules. It enables the cross-border partner to absorb the limitations, innovate on top of the existing solution and obtain a technological advantage.

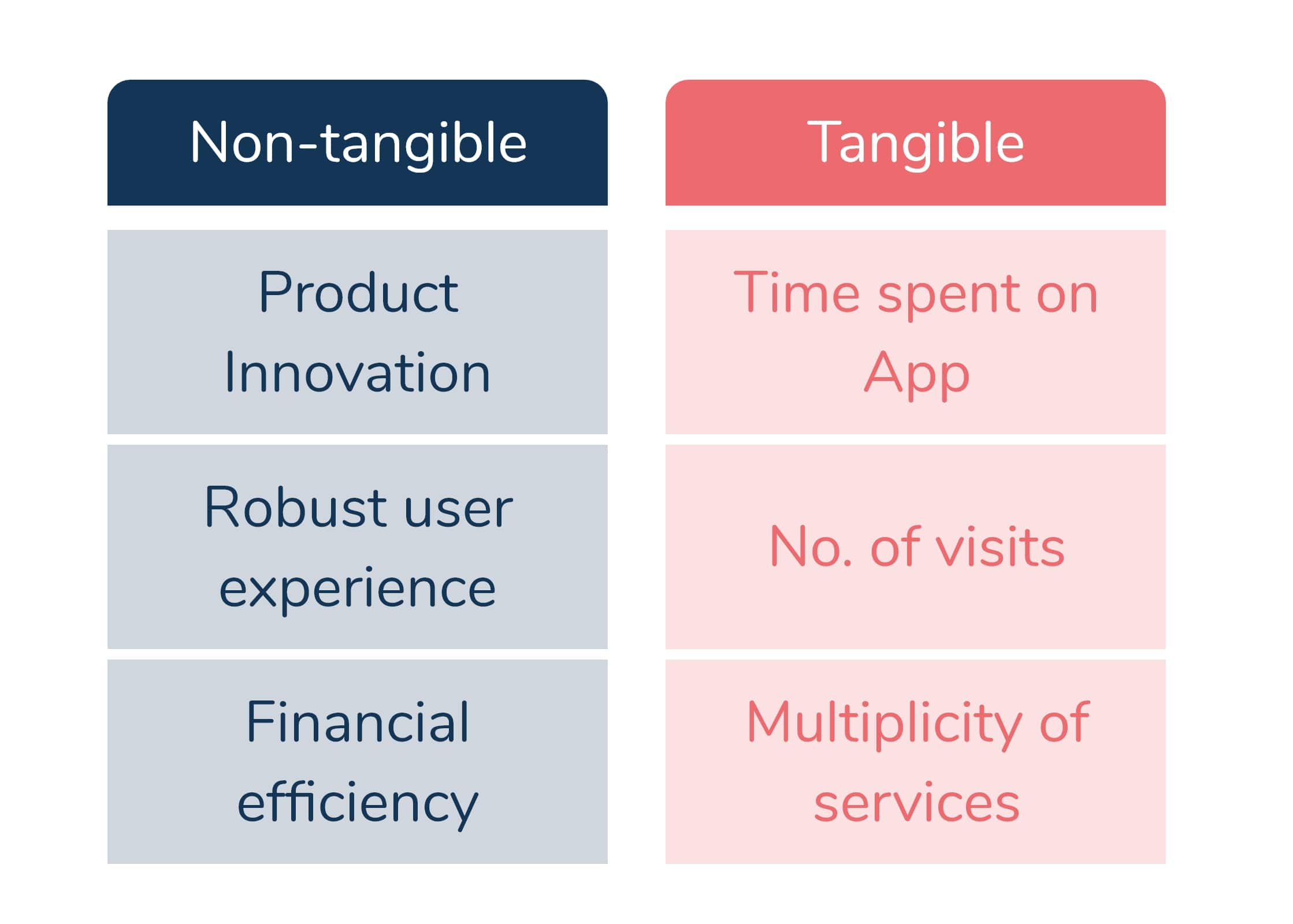

6. Survival of the ecosystem is a good measure of success

It is difficult to predict what measures will lead to ecosystem success. The ecosystem’s survival is a good indicator of success, while its growth demonstrates adaptation.

The ability of an ecosystem to grow and sustain itself is crucial to its survival, which means that if one component of the ecosystem fails, the rest will fail as well – a domino effect.

Other measures of success include product innovation, robust, frictionless and intuitive user experience and other tangible measures, such as:

- How much time is a user spending on a particular app?

- How often is the user visiting and the multiplicity of the services for which the individual is visiting that app?

Figure 3: Digital ecosystem measures of success

Since financial services are becoming more embedded, customers are beginning to take control of their finances. As a result, customers can have complete transparency. Thus, the current financial efficiency of the banks will translate to consumers indirectly through their behaviour.

The other transition that is occurring, from a customer experience standpoint, is that financial institutions are extremely product transactional focused. Still, the consumer utilises the bank to achieve a life goal. As a result, there is a dichotomy. A good surviving ecosystem should allow the consumers to achieve their life goals frictionlessly with the aid of the banking and financial services suite.