Summary:

Enterprise business accounted for 19.1% of the total telco revenues across 25 leading telcos in Asia Pacific for the year 2021. Telco’s have prioritized the enterprise business growth and this is now beginning to reflect in the financial performance of the leading companies. While in 2021 enterprise business accounted for 19.1% of the total revenues, we are quite bullish that it will account for between 30 to 32 percent of the total by the end of the decade. Three key factors will drive this growth:

- 5G as a key catalyst for new enterprise propositions

- inorganic growth driven by acquisitions in adjacencies such as cybersecurity, cloud and managed services

- increased success in growing the SME business segment.

For the purposes of the analysis, we further segmented the telco enterprise business into two distinct categories, viz.,

- Connectivity: includes voice, fixed-line, data communications (including leased lines, IP-VPN, SD-WAN, etc) provided explicitly to enterprise customers.

- Non-connectivity: includes cloud, managed services (collaboration, contact centers, other IT services and applications), IoT, cyber-security, etc.

The assessment of these 25 service providers reveal the following 6 highlights.

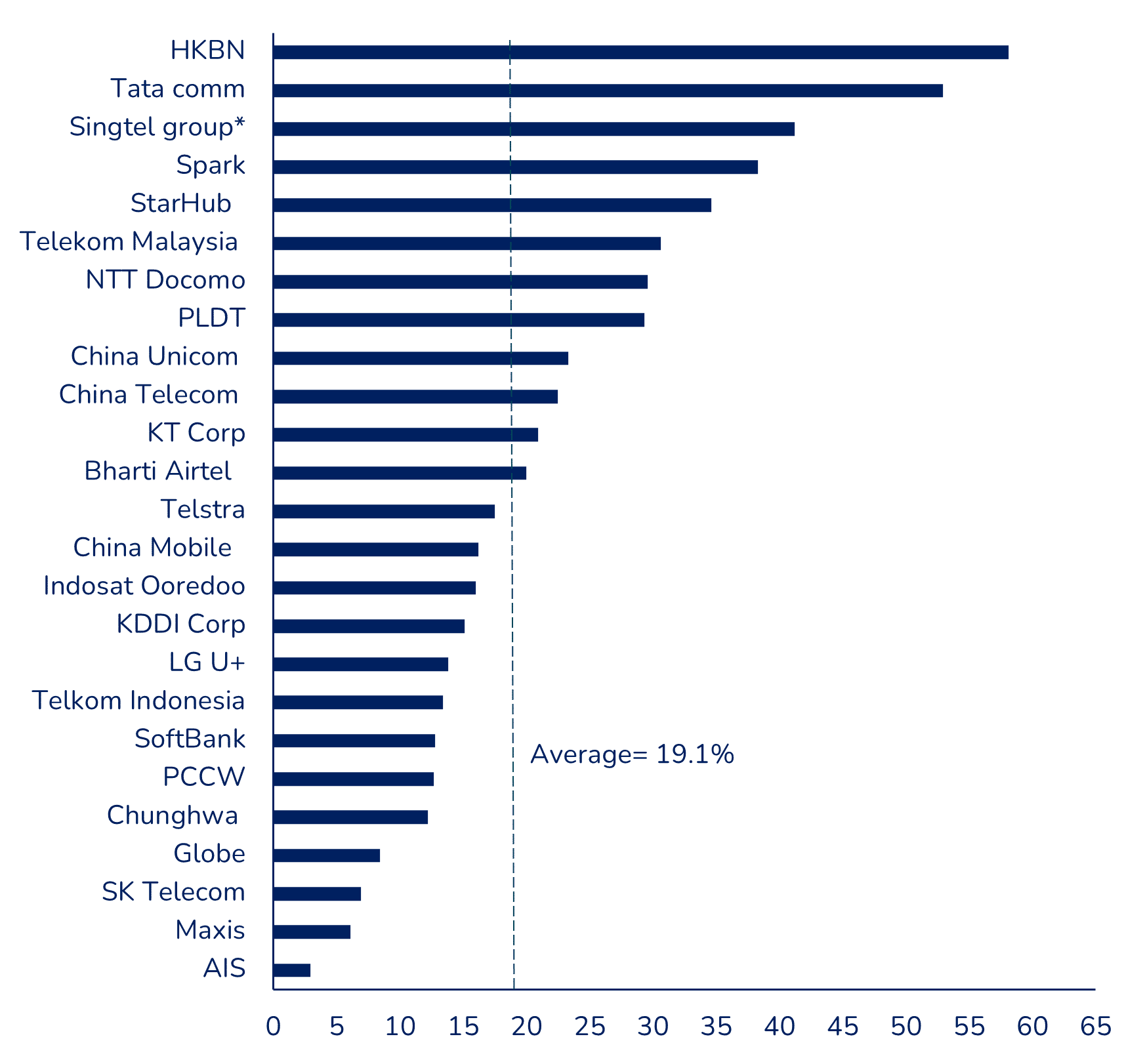

#1 Enterprise revenue grew by 10% as compared with total industry growth of 6.5%

85% of the telcos studied showed a positive change in their enterprise revenue in 2021. The average revenue share for enterprise has increased from 18.5% in 2020 to 19.1% in 2021.

Figure 1: % of enterprise revenues to total revenues 2021

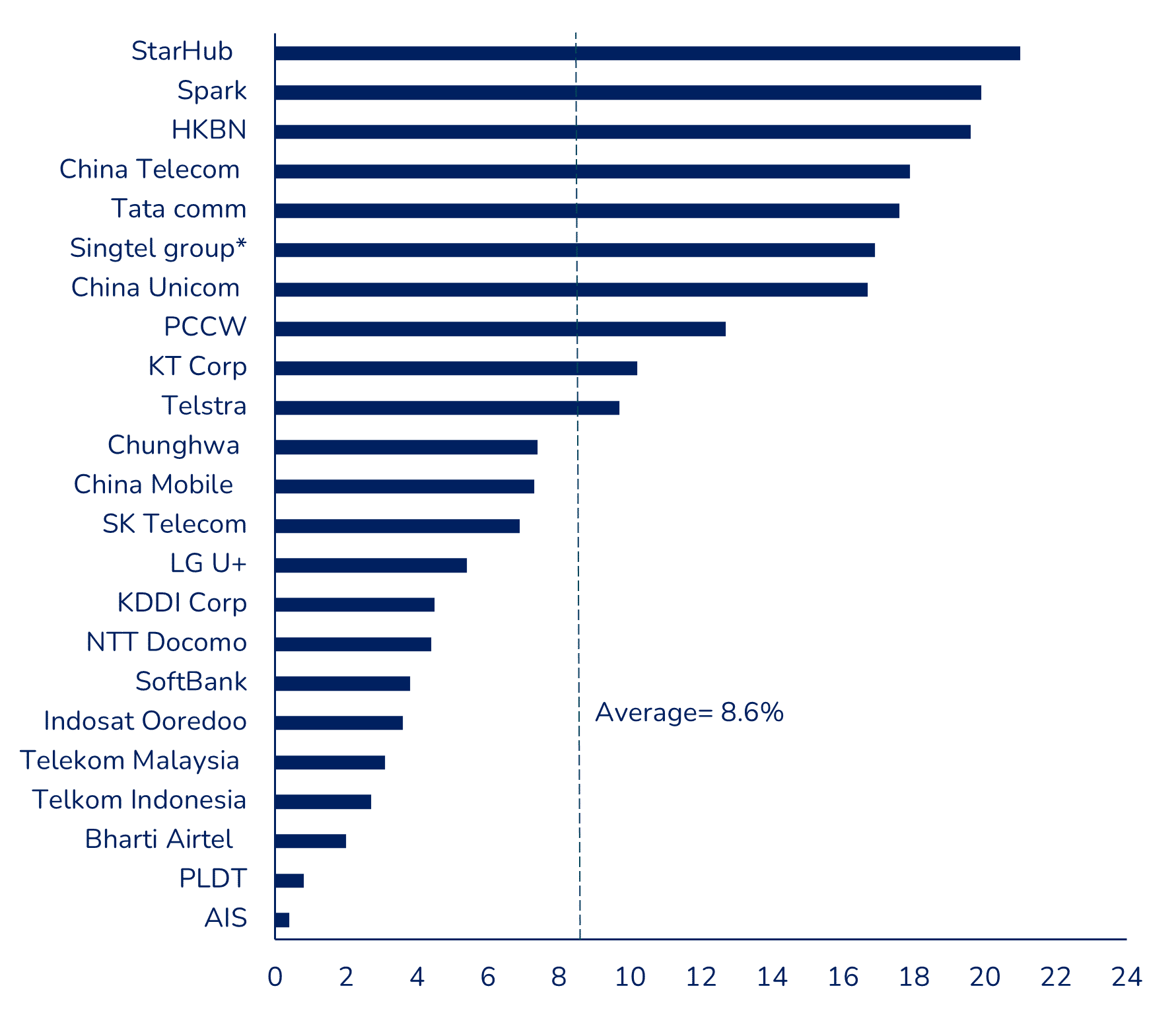

#2 Enterprise non-connectivity revenue records growth of 20%, 2X the overall growth of the total enterprise business

Price competition continues to put tremendous pressure on connectivity revenues. Revenues from non-connectivity will be the key growth engine in the coming decade. Table 2 below showcases the enterprise non-connectivity revenues as percent of the total revenues.

New growth segments such as public cloud are in its still in early stage of market adoption. For example in the South East Asian market, twimbit expects revenues to reach USD 12.5 billion by 2026, growing at a 17.4% CAGR (2021-2026). (Find out more on the South East Asian cloud economy report here.)

Figure 2: % of enterprise non-connectivity revenues to total revenues 2021

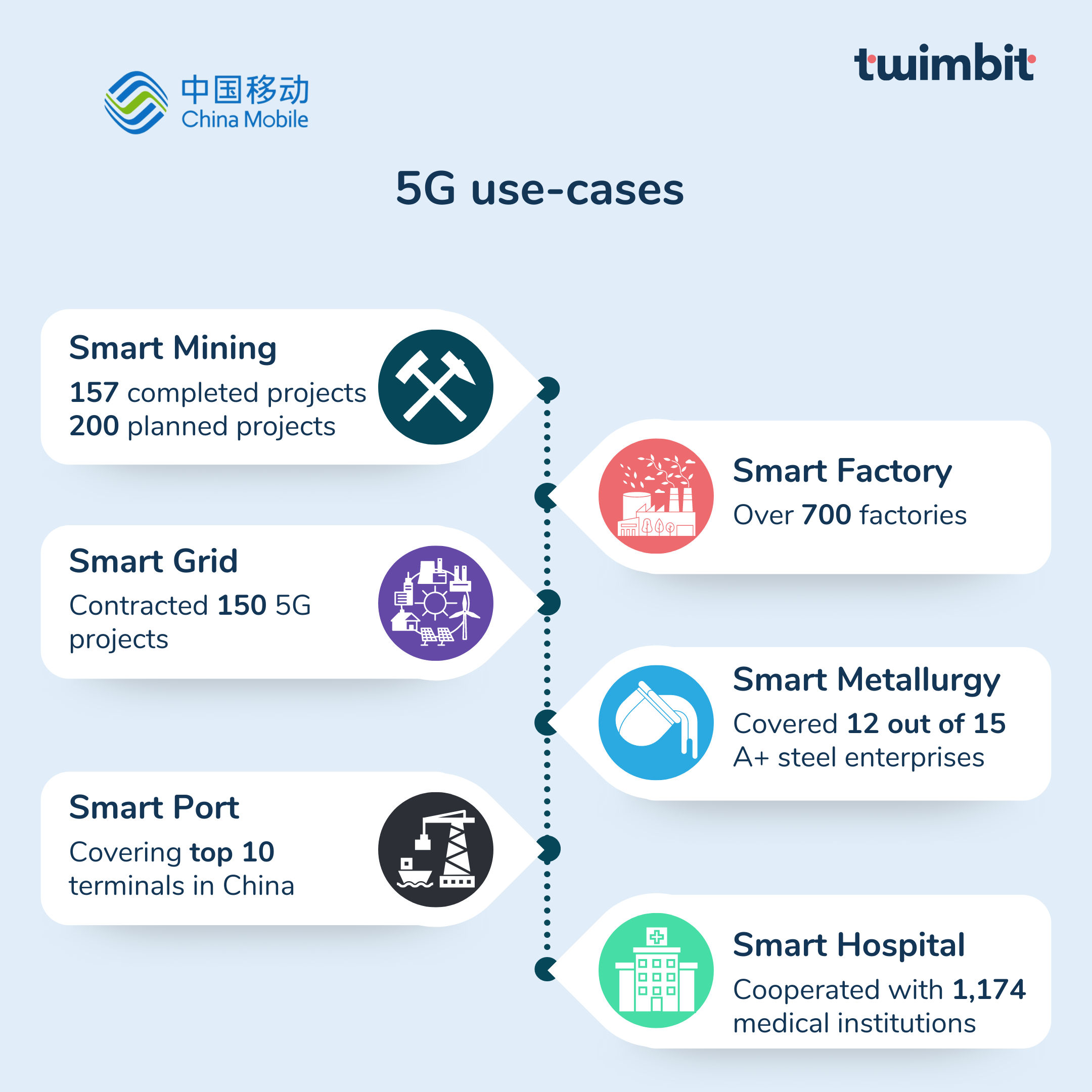

#3 5G industry use cases drive strong growth for China Mobile, is now the benchmark for other service providers

- China Mobile has the largest enterprise business in the region with revenues of USD 20.5 billion (16.2% of total revenue), recording the highest growth of 21.4%.

- The non-connectivity business achieved USD 9.3 billion in revenues, growing at an exceptional rate of 43.2% in 2021.

Figure 3: Enterprise overview of China Mobile

| Component | Measurement | Growth 2021 |

| Corporate customer base | 18.8 million customers | 36.1% |

| Industry cloud revenue | USD 2.8 billion | 110.0% |

| Internet Data Center | USD 3.2 billion | 33.0% |

| Dedicated lines | USD 3.9 billion | 10.0% |

| ICT revenue | USD 2.1 billion | 35.2% |

| IoT revenue | USD 1.7 billion | 21.3% |

- 5G enables the delivery of industry leading projects

- Launched 200 leading 5G showcases, signed agreements with 2,800+ quality commercial projects and developed 1,590 5G dedicated network projects.

- Implemented a wide range of solutions across verticals – smart mining, smart factories, smart grid, smart metallurgy, smart ports and smart hospitals.

- Developed a manageable and controllable 5G dedicated industry network with device cloud integration to cater to the differentiated needs of enterprise customers.

- Spent USD 2.7 billion on research and development (R&D) ~ 2.2% of total operating revenue. Employee related expenses increased by 11.5%, mainly due to higher resource allocation towards R&D talent.

Figure 4: 5G uses cases in different Industries- China Mobile

#4 Partnerships is a growth driver; HKBN aces enterprise business growth on the strength of a strong partner ecosystem

Building the right partner ecosystem is a must for telcos to succeed in the enterprise business. HKBN is a good benchmark and has 58% of total revenues accruing from the enterprise business. It has approximately 106,000 corporate customers with an average enterprise ARPU of USD 370. It has forged a number of partnerships.

Figure 5: Partner ecosystem of HKBN

- StarHub: This partnership is to help scale the 3C’s (Cloud, Cyber Security and Connectivity). Together, the two parties have built connectivity and solution platforms across Singapore and Hong Kong, oriented towards the 3C’s.

- UiPath: HKBN helps regional enterprises drive automation, cut costs, and facilitate innovation.

- Microsoft: helps enterprises with collaboration solutions to support hybrid work environments.

- Cisco: Safeguards SMEs in the digital space by strengthening Internet security and addressing cybersecurity-related issues with cloud security solutions.

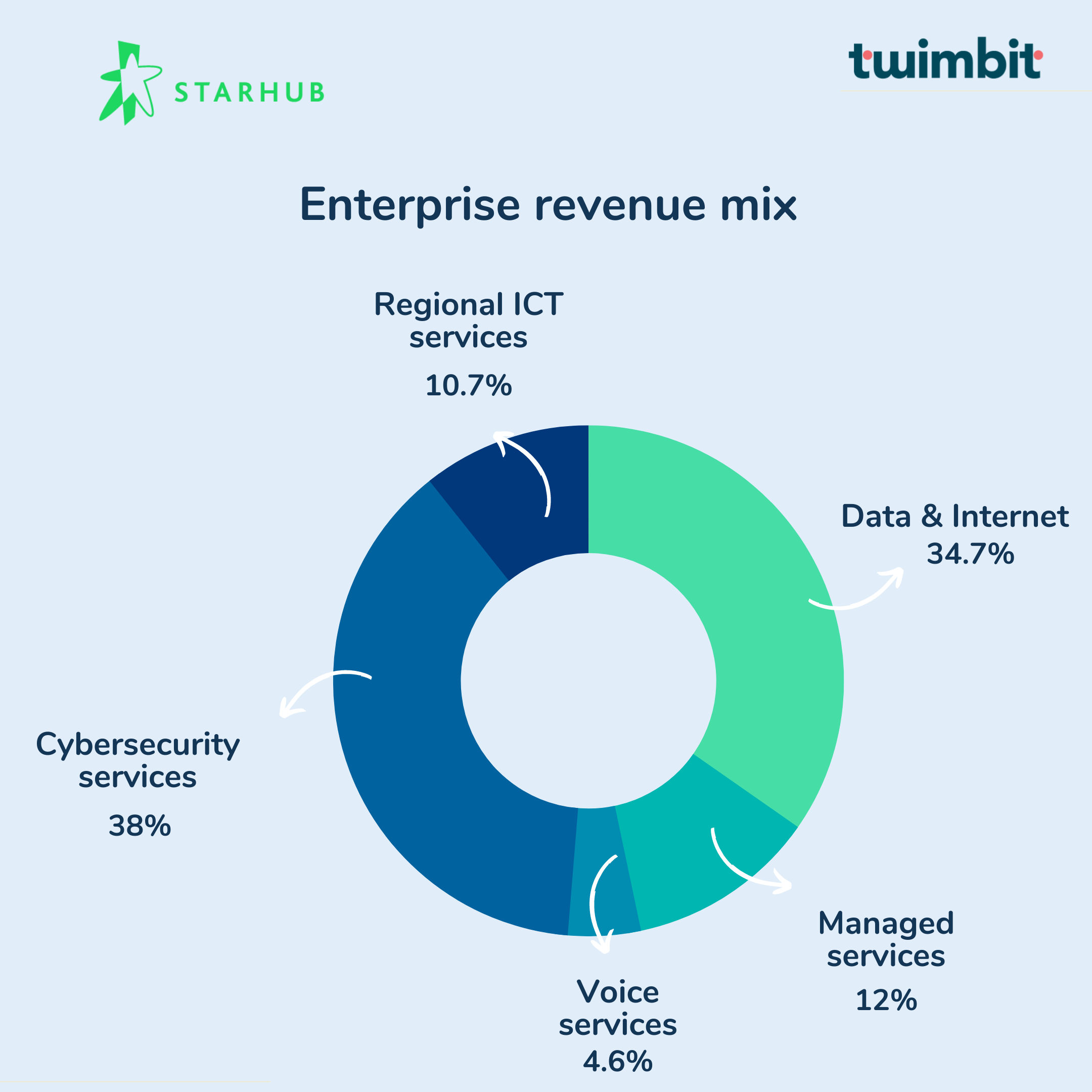

#5 Cloud and Security the growth engines for enterprise leaders; StarHub’s focus on 3C’s – Cyber Security, Cloud, and Connectivity pays off

Cloud and security are the two biggest growth drivers for the enterprise business. Total ICT spending in Singapore is estimated at USD 27.9 billion a year (highest in the SEA region), of which 10.1% was expected public cloud spending in 2021.

StarHub has clear focus on converged platforms to bring together the 3C’s. It intends to invest heavily in this domain, positioning itself well through collaboration with key partners. StarHub is prioritising:

- 5G next-gen network products,

- a managed Secure Access Service Edge (SASE), and

- digital/cloud transformation services.

Figure 6: Enterprise revenue segmentation of StarHub

- Cybersecurity and regional expansion through acquisitions have been the key drivers of growth.

#1 Cybersecurity

- Created a one-stop cybersecurity offering in collaboration with – Ensign InfoSecurity, Palo Alto Networks and Veeam

- Total revenue of USD 195 million, up 21.7% YOY.

- Expanded to Brunei, Indonesia, Myanmar, South Korea, and Vietnam.

- Provides security services across all public cloud environments.

- Delivers 5G and IoT security.

- Possess capabilities around Data science and AI for threat detection.

#2 Acquisitions foster regional expansion

- Acquisition of Strateq and HKBN JOS (In Singapore & Malaysia) spur growth

- Total revenue in 2021 is USD 55 million.

- Focus areas are cloud, managed services, 5G enablement, Enterprise Healthcare, and eCommerce.

- Strateq & HKBN JOS aim to become Malaysia’s number 1 ICT service provider.

#6 Acquisitions help develop new skills and capabilities

Telecom service providers are operating with a sense of urgency to build new capabilities. They are looking at acquisitions as a means to augmenting their teams. Some of the major acquisitions done by telcos in the region are summarized below.

| Telco | Entity acquired and objectives |

| SingTel | ICT arm of SingTel (NCS) made its largest acquisition of USD 238.9 million when it acquired the Dialog group, Australian largest privately owned IT services company to support its public sector and enterprise clients. |

| Starhub | Acquired a 60% stake in HKBN JOS- Singapore & Malaysia for consideration of USD 10.7 million with the objective to lead as a system integrator and solutions provider. |

| Spark | Bought back 50% of the shares in Connect 8, an infrastructure provider to the telecommunications, water, and power sectors. This entity will be wholly owned by Spark to accelerate 5G rollouts and support the uplift in IoT connections. |

| Airtel | Embarked on an initiative to acquired stakes in budding startups as part of its ‘Airtel Startup Accelerator Program.’ – Acquired 25% stake in Lavelle Networks, SD-WAN startup – Bought strategic stake in Aqilliz, blockchain technology startup – Minority stake in Cnergee Technologies, cloud-based networking solutions provider |