The growth momentum continues for the APAC telcos in 3Q 2021. 86% of the operators enjoyed positive revenue growth. In this report, we evaluate and summarise the performance of 37 APAC telcos for the third quarter (3Q 2021) of 2021.

#1 Industry revenue growth at 6.8% compared to 2.7% in 3Q 2020

- 37 telcos added USD 8.3 billion in revenues in 3Q 2021; this number was at USD 3.2 billion at the same time last year. Top 5 telcos of the twimbit Growth Index contributed 77% of the total net additions, i.e., USD 6.3 billion.

The revenues for APAC operators declined 3.9% quarter-on-quarter (Q3 2021 vs Q2 2021), but the year-on-year growth continues for the third consecutive quarter this year. Check out our previous quarterly updates here (2Q 2021 & 1Q 2021)

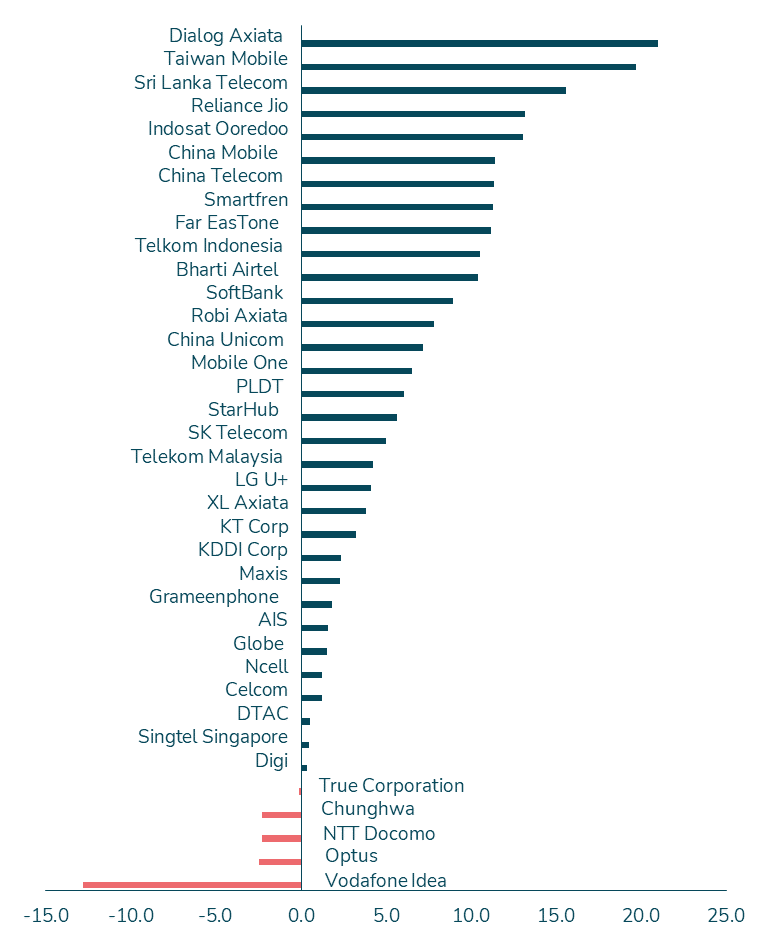

Figure 1: Revenue change (%) for APAC telco operators, 3Q 2021

- Dialog Axiata had the highest growth in revenue, yet again. The growth is driven by subscriber additions in almost every segment of its business. Fixed-mobile and household TV subscribers grew by 12% and 9% (Y-o-Y), respectively. The Sri Lankan operator made a notable change in its CAPEX spending, focusing on 4G capacity upgrades and broadband infrastructure. We discuss the CAPEX spendings of telcos in the subsequent segment of the article.

- The launch of iPhone 13 this quarter fuelled the sale of equipment for Taiwan Mobile. The bundling of services from its telecom to cable TV services complemented the growth. Also, its e-commerce segment, Momo, saw a surge in revenue and EBITDA, increasing the number of transactions by 44% Y-o-Y.

- Subscriber traction in connectivity business continued to drive quarterly revenue for Reliance Jio. The company’s customer base had the highest gross subscriber addition in the last seven quarters.

- NTT Docomo and Optus both faced challenges in equipment sales. NTT Docomo provided discounts in equipment sales impacting profitability, while Optus faced supply shortages and lower footfall due to the pandemic.

- Vodafone Idea continued to face a setback because of AGR dues, which impacted liabilities. However, the recent government reform package is a positive development for the operator. The telco has no government dues payable towards spectrum and AGR over the next four years, except for spectrum instalment.

#2 EBITDA growth stable at 3.5% compared to 3.1% in 3Q 2020

- In 3Q 2021, the industry added USD 1.5 billion in incremental earnings (Y-o-Y), which were at USD 1.3 billion same time last year.

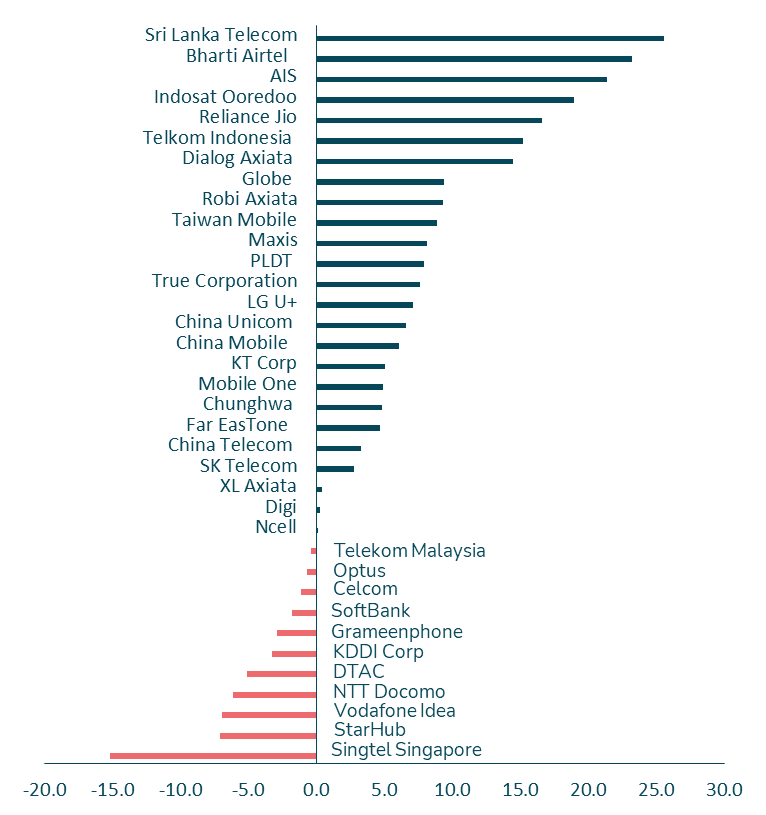

- Sri Lanka Telecom had significant revenue growth coupled with the highest EBITDA change. This was made possible by a customer-centric marketing strategy, which resulted in demand for fibre connectivity from residential and business clients. The group’s investments in submarine cable networks and domestic transport networks yielded positive results, enhanced the quality of digital connectivity in Sri Lanka.

- Bharti Airtel and AIS have diversified with growth in the financial services industry. Airtel Payments Bank, a Bharti Airtel subsidiary launched in 2017, provides financial services in India. It recorded more than a billion financial transactions this quarter and has 115+ million users. AIS invested USD 8.9 million in a joint venture with Siam Commercial Bank (SCB), a bank for digital lending business. The services of the joint venture will commence from the first quarter of 2022 to provide credit facilities to AIS customers with a good credit history.

- Indosat Ooredoo continued its growth momentum and additions in customer base. The Indonesian telco announced its merger with CK Hutchison on September 21, making them the second-largest telco. Listen to their growth story in our conversation with Vikram Sinha, Director & COO, Indosat Ooredoo, here.

- StarHub saw a decline in pay-TV subscribers and commercial TV revenues because of lower spending on advertising by business customers. For Singtel, the Singapore consumer segment noted a negative change of 1.3%, mainly caused by a 7.9% reduction in mobile equipment sales. This was due to global chipset shortages causing supply interruptions.

Figure 2: EBITDA change (%) for APAC telco operators, 3Q 2021

#3 CAPEX grew by 5.7% compared to 2% in 9M 2020

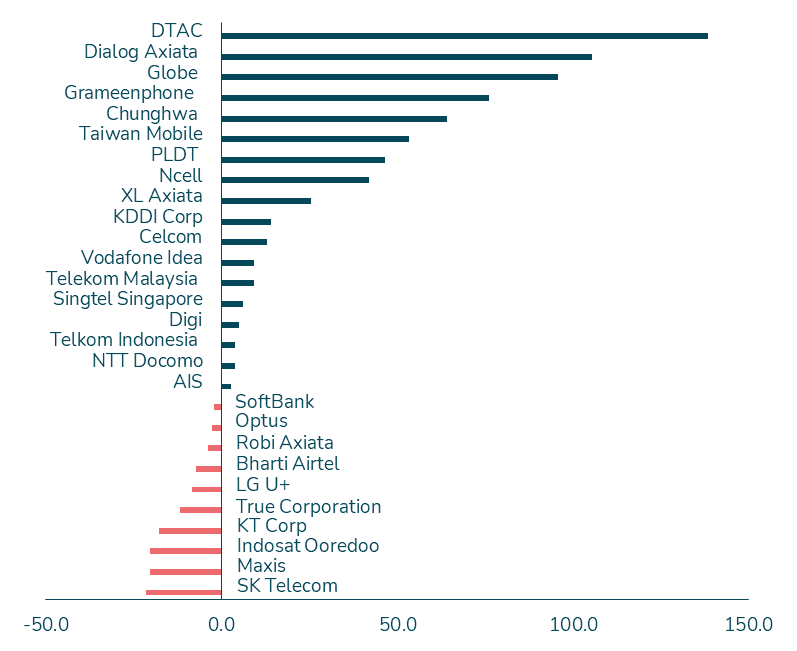

- Almost 65% of telcos increased their spending in 9M 2021. The majority of the investments done was to develop the 5G infrastructure in the region.

- For Dtac, CAPEX spending focused on the accelerated low-band rollout and capacity expansion. As of September 2021, Dtac installed a total of 21,200 nodes of 4G- 2300 MHz.

- Dialog Axiata also focused its spending on network capacity and coverage in the country. As a result, 4G and fixed LTE coverage reached 93% and 70%, respectively. These investments have worked very well for the telco in top-line and EBITDA growth.

Figure 3: CAPEX change (%) for APAC telco operators, 9M 2021

#4 Trends in ARPU

- Chinese and South Korean telcos continued with steady growth momentum in mobile ARPU mainly because of the rising penetration of 5G. User migration to 5G plans is expected positively impact ARPU growth.

- In Thailand, the government has offered subsidies to support consumers. COVID-19 restrictions were uplifted later in the quarter, including re-opening telecom shops in malls. AIS positions 5G as a premium product, and its 5G subscribers reached 1.5 million as of September 2021. These subscribers are paying a premium to enjoy the greater benefits of 5G. All these factors are leading to an increase in ARPU.

Figure 4: mobile ARPU change (%) for APAC telco operators, 3Q 2021

#5 China Mobile, Reliance Jio, China Telecom, Taiwan Mobile and SoftBank ace twimbit’s Growth Index

The twimbit’s Growth Index recognises the leaders based on two parameters with an equal weightage to:

- Absolute change in revenue

- Percentage change in revenue

Figure 5: Net addition and % change in revenue for top 5 telcos, 3Q 2021

| Telco | Country | Change (USD million) | % Change (Y-o-Y) |

| China Mobile | China | 3,143 | 11.4 |

| Reliance Jio | India | 298 | 13.1 |

| China Telecom | China | 1,679 | 11.3 |

| Taiwan Mobile | Taiwan | 221 | 19.7 |

| Softbank | Japan | 1,030 | 8.9 |

| All APAC | – | 8,306 | 6.8 |

| Top 5 | – | 6,371 | 11.1 |

- All three Chinese telcos reported net gains in the number of mobile users mainly because of higher demand for second SIM cards amid increased dual-SIM device adoption. China Mobile scaled its 5G business remarkably. The 5G package customers and 5G network customers touched 331 million and 160 million respectively at the end of the third quarter. For China Telecom, the number of mobile users increased by 18.6 million to a total of 370 million by September 2021.

- Average data and voice consumption per user per month has continued to increase for Reliance Jio. The telco also announced that it has plans to release the Jio phone next, in partnership with Google. With its wide availability through the Jio Mart Digital network and industry-leading specifications, Reliance Jio would be able to accelerate digitalisation and provide its customers with a unique experience.

- Taiwan Mobile enjoyed a monthly fee uplift from customers upgrading to 5G to the tune of about 26% in the quarter. It also plans to participate in the metaverse universe, as mentioned in recent reports to capitalise on the new opportunities that come with 5G.

- SoftBank is applying a multi-brand strategy to support a diverse customer base. There are several brands under this strategy, including:

- SoftBank: Provides high-volume flat-rate data plans to customers

- Y!mobile: Provides low monthly communication charges

- The LINEMO: an online-only brand

- From August 2021, the company eliminated the need for customers to issue Mobile Number Portability (MNP) reservation codes when switching between SoftBank, Y!mobile and LINEMO brands, making SIM unlocking processes immediate. This move allows buyers to choose the best brand for their needs.