Introduction

Bad customer experiences are costing businesses around US$4.7 trillion every year, worldwide1. The situation, on the contrary, stands that it costs customers almost nothing to switch to a business that truly cares about them.

The rise of digital payment platforms and fintech disruptors are showing customers that their experiences are relevant. They are providing customers with what they want – efficient and hyper-personalised experiences, delivered through digital mediums. Traditional financial institutions need to show customers that they care to maintain customer satisfaction and ultimately customer loyalty. Retail banks that prioritise improving customer experiences see a growth 3.2 times faster than their peers that don’t2.

twimbit based this defining CX report on primary research with leading Malaysian banks. It outlines the top initiatives taken by these banks across three customer experience milestones to build long-term relationships.

The report aims to help people like you — Chief Executive Officers (CEO), Chief Experience Officers (CXO), Chief Marketing Officers (CMO), Chief Operating Officers (COO), Chief Information Officers (CIO) and business leaders in the banking industry— create a journey that customers love.

Methodology

Step 1

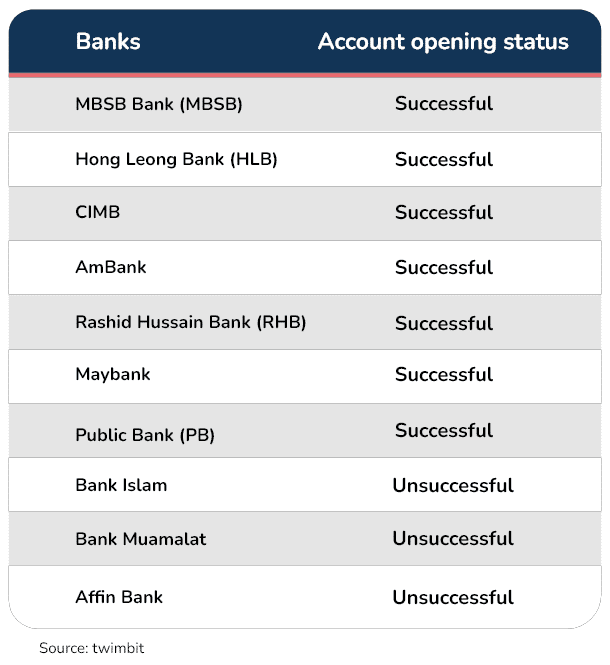

We attempted the savings account opening process with 11 of Malaysia’s local banks from November 2021 to January 2022. However, we successfully opened bank accounts with only seven banks (Table 1).

Note: Bank Islam, Bank Muamalat, Bank Rakyat and Affin Bank agents informed us that they only accept applications if a person is still schooling or for salary purposes.

Step 2

We recorded the account opening process, from searching for information regarding different bank accounts to application and activation.

Step 3

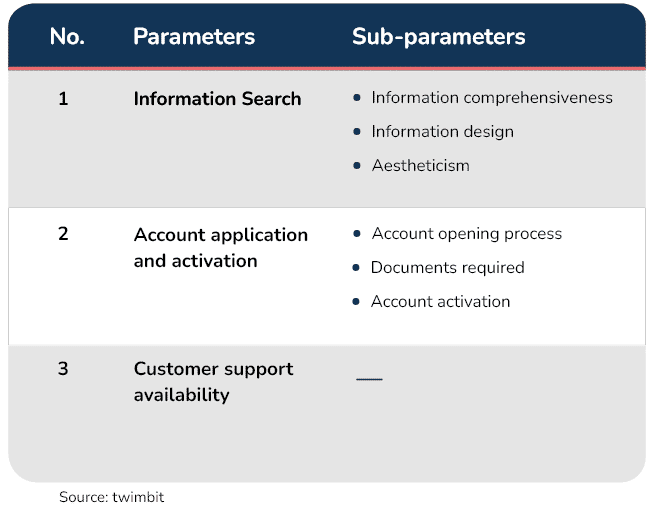

From our observations, we developed a framework to evaluate the process. The framework below assesses how a bank performed based on three parameters and six sub-parameters across the account opening journey (Table 2).

Step 4

We scored each bank that we successfully opened a savings account with on a scale of 1 to 5 according to these parameters. 1 represents the lowest score in the parameter and 5 represents the highest score.

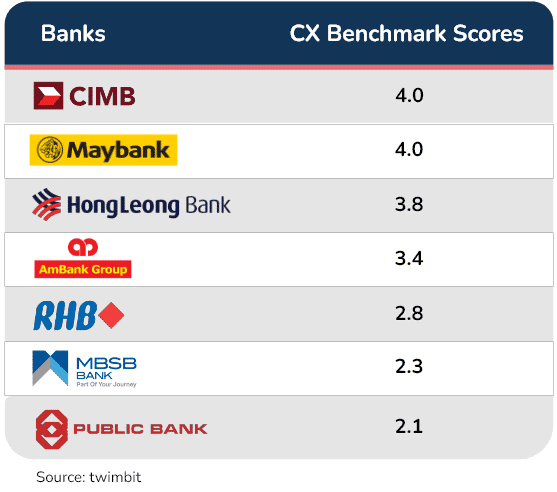

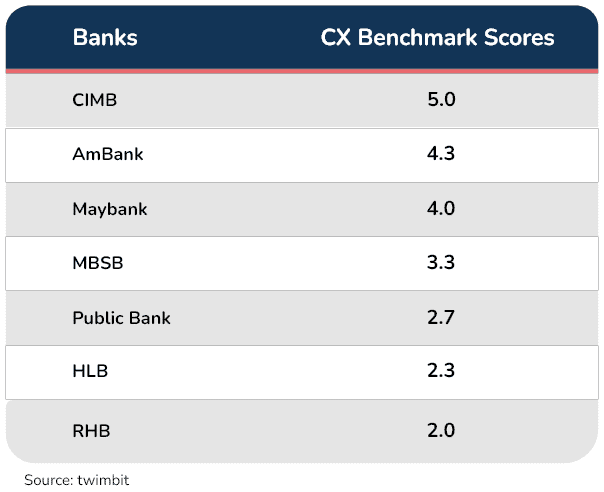

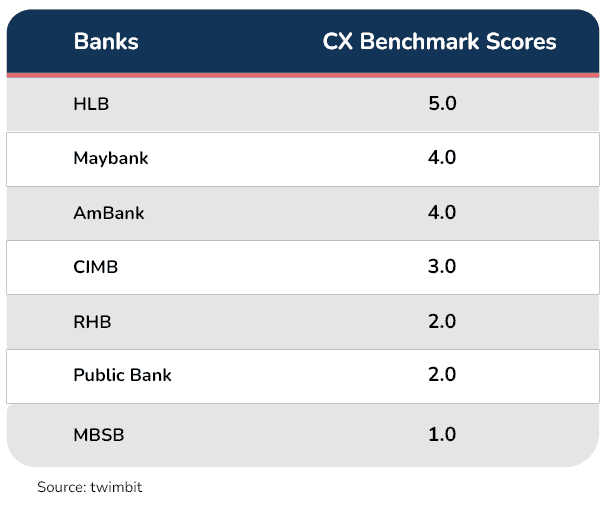

Customer experience benchmark of the top 7 banks

Customer experience analysis for each parameter

1. Information search

1.1 Information comprehensiveness

This section looks at the type of information provided on the bank’s website and how comprehensive it is.

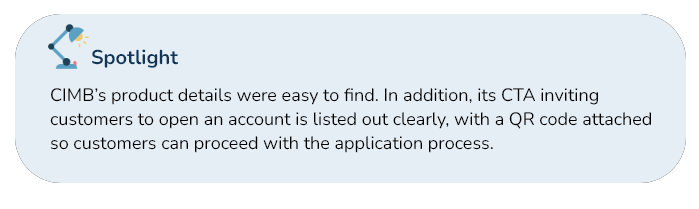

We see all banks list out basic, crucial information, such as the eligibility criteria, minimal balance required and bank rates. While most banks presented their fees (including debit card fees and charges) and standard services available (e.g. ATM facilities, account statements etc.), it’s not the case for MBSB, CIMB and PB. MBSB did not clearly state its fees, CIMB’s OctoSavers account did not state the services available, and PB missed out on the accessibility of bank statements.

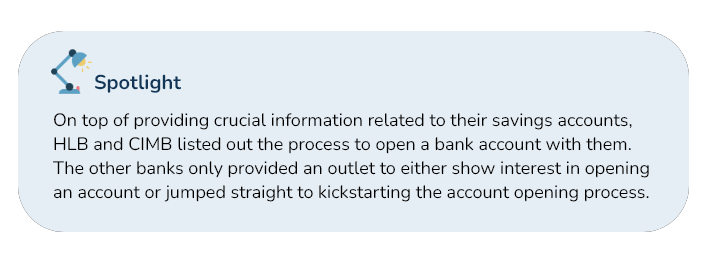

In the case of documents required to open a bank account, MBSB and PB did not provide this information on their websites. Only HLB, CIMB and Maybank laid out the steps to open an account with them. Other banks either kickstart the account opening immediately, ask customers to indicate their interests, or request customers to contact the branch. We note that PB did not provide any of the options above.

1.2 Information design

Information search should be intuitive and easy, with a clear call-to-action (CTA). Only CIMB and RHB have excellent information flow. While MBSB and HLB have well laid out details on their savings accounts, the CTA is on another page. This means customers may need to search for the next steps in another section of the website instead of proceeding immediately. For the other banks, we notice that either the product allocation or details are hard to access, or they lack a CTA.

1.3 Aestheticism

It’s not just essential to have good products; it’s equally crucial to ensure that the mediums where customers get to know and interact with your brand are captivating. In this case, it’s your banking website or app.

Currently, all seven bank websites have clear readable fonts, while most have clear website layouts. Only CIMB has bright, attractive colours, whereas HLB, RHB, PB and Maybank spot clear icons, reducing the usage of texts. Only CIMB, RHB and Maybank have good usage of illustrations or pictures.

2. Account application and activation

2.1 Account opening process

We are in the middle of a pandemic and the era of ultimate convenience. In this section, banks with a fully digital account opening process will come up top.

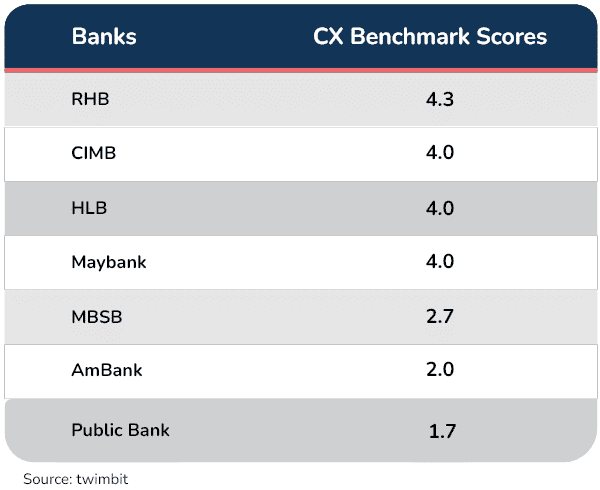

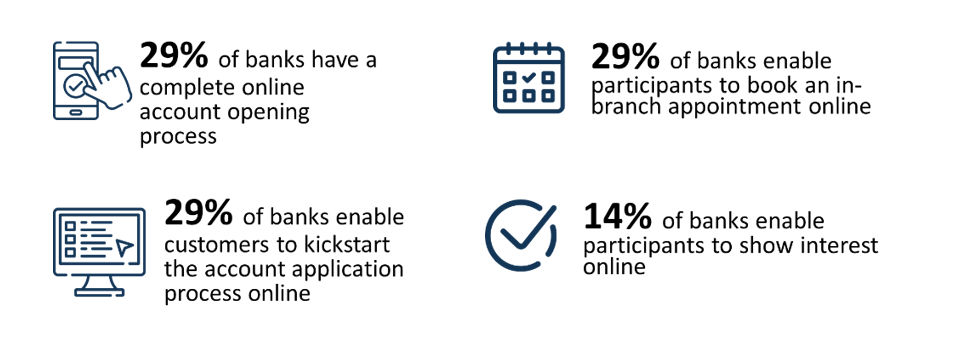

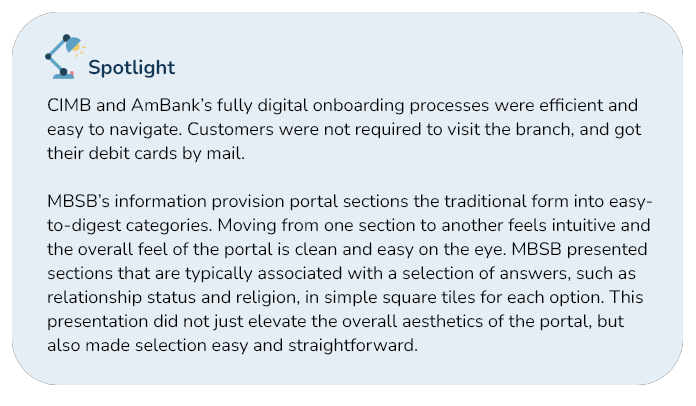

CIMB, AmBank and HLB offer end-to-end digital journeys. However, we proceeded with the in-person branch experience for HLB after facing verification errors. CIMB’s app usage experience was smooth, whereas AmBank’s was buggy.

Even though it’s not a complete digital journey, MBSB and Maybank enable customers to kickstart the journey online and have an online booking system for branch visits. This allows customers to complete the in-person know your customer (KYC) process without spending time in a queue. Contrarily, RHB lets potential customers only state their interest online*. Also, PB does not offer any online methods to kickstart the account opening journey nor the ability to show interest.

We assessed different information provision portals from banks with an end-to-end online or hybrid experience. We completed the full/partial application forms or showed our interests using these bank portals. All portals have a clear, readable font, with clean layouts. However, Maybank’s form felt like a digitalised version of the traditional information provision form. Its form provided all categories in one single spread, had drop-down menus with convoluted selections and was least aesthetically pleasing. In comparison, MBSB and RHB have clear sections designed with a minimalistic aesthetic approach.

*We note that during the in-branch account opening process, the RHB bank agent showed us that we could indeed kickstart the process online by leaving our details in their online portal. However, this portal is under the RHB online banking login page, RHB Now. There were no prompts on the main RHB group website that led us to the RHB Now page. Thus, we were not aware of the said portal.

2.2 Documents required

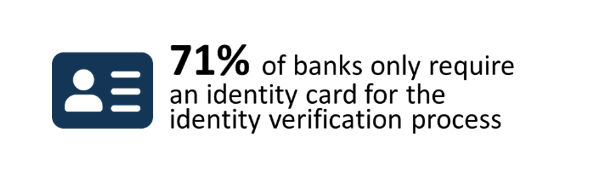

Requiring a minimal number of documents as part of the customers’ KYC process should be a priority for all banks. Five (i.e. CIMB, HLB, AmBank, PB, Maybank) out of 7 banks only required customers’ identity cards (IC) in our study.

2.3 Account activation

This parameter looks at customers’ activation experience, starting from the account opening process.

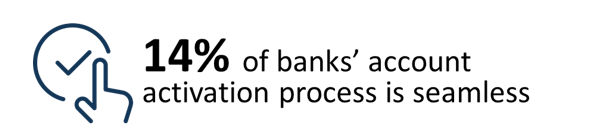

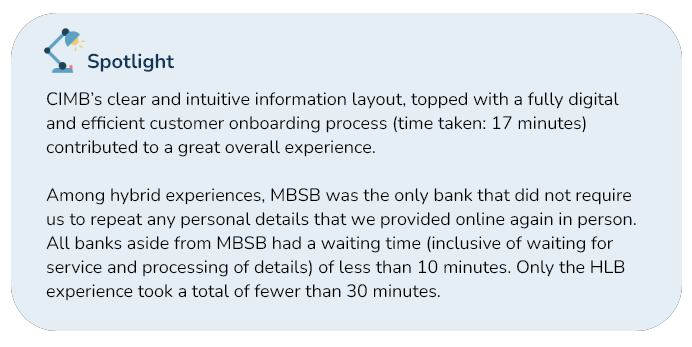

Only CIMB’s account opening process was seamless, as it was a complete online customer onboarding experience that took 17 minutes. The other bank with an end-to-end digital account opening process, AmBank, took around 25 minutes. By looking at the time required to complete the online onboarding process, we measured the bank’s Onboarding Efficiency, specifically the “Self-Service Onboarding Duration”, based on the “Temenos model of measuring digital success”3.

MBSB came in second for activation seamlessness, given that it required a longer waiting time (around an hour, due to system outage, as explained by the bank agent) for the in-branch process. AmBank, PB and MayBank’s processes had some minor friction along the way, whereas HLB and RHB’s overall experiences were not very pleasant.

For banks with hybrid experiences, 15 minutes or fewer is the gold standard for the average time taken to complete the KYC process. HLB required less than 30 minutes, Maybank took around 45 minutes, whereas RHB’s KYC procedure occupied more than an hour.

3. Customer support availability

Banks offer a multitude of customer support mediums. The banks with the most variety of interaction methods will lead the category.

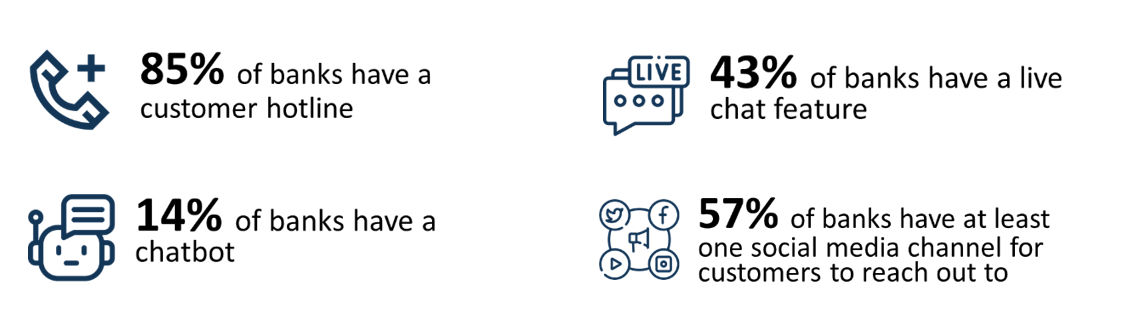

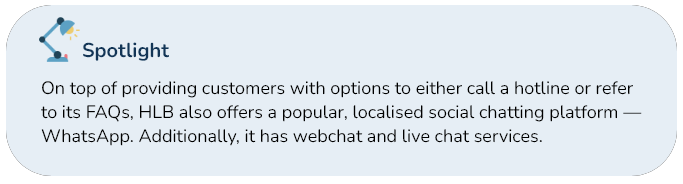

All banks have a Frequently Asked Questions (FAQ) tab that supports common customer queries. Only MBSB do not have a customer support hotline. Maybank, CIMB, AmBank and HLB have adopted at least one form of social media platform as an additional medium that customers can reach out to. HLB, AmBank and Maybank also support live chats, whereas only HLB has a chatbot.

Analyst critique and recommendations

Overall, most of these banks need to improve customer experiences, especially their digital channels. Less than half of the banks presented their account opening process clearly on their web pages. This step is crucial as informing customers of what to expect beforehand can significantly enhance the experience.

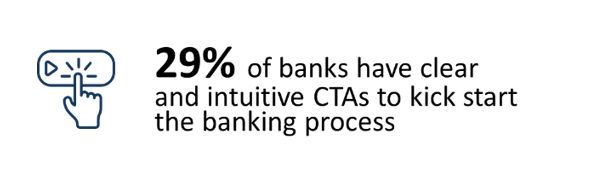

Less than 30% of banks have an end-to-end online customer onboarding journey. While this means that the other banks require customers’ physical presence to complete the onboarding process, only 29% of banks allow customers to book in-branch appointments. For the rest, customers need to wait in the queue, with potentially long waiting times before receiving service. On the other hand, 71% of banks only need customers’ identification cards in the KYC process, which is a huge plus point. More than half of these banks also provide customer support on social media channels.

Checklist to elevate your bank’s customer experience:

Product information – Customers should be able to find all important information related to opening and maintaining the chosen bank account and the services that come with it on the bank’s website.

- Crucial details to include – eligibility criteria for account opening, the minimal balance needed to maintain the account, charges and bank rates

- Services provided with the account – internet banking possibilities, frequency of bank statements, debit card or ATM services

- Documents needed to open an account

- Exact steps to take to open an account

Information design – We all like things that come easy; this applies to getting information too. Customers should not have to dig for details regarding your products.

- Information should be readily available, intuitive to search for

- Include a clear call to action (CTA) for customers. Make it easy for customers to proceed with the account opening process.

Aestheticism – If fintech disruptors have one thing in common, it is the trendy design of their websites. While its crucial to have good products, ensuring that the mediums where customers get to know and interact with your brand captivate them is also equally important – in this case, it’s your website or app.

- Must-haves – Clear fonts in readable sizes, with clean website layouts

- Enhancers – Usage of fun graphics and small gamification points throughout the website

Account opening process – Normalised by neobanks in neighbouring countries, a fully digital customer onboarding process can elevate your customers’ experience. Considering that we are in pandemic times, having the option to complete this process digitally allows customers to feel safe. If that is unachievable at the moment, consider:

- Allowing customers to kickstart the account application process online – this includes filling in all details needed for the account.

- Enabling a branch appointment system – provide customers with certainty and eliminate unneeded queuing time

Documents required – Bringing a bunch of documents to the bank is at best a hassle, at worst, an annoyance. In Malaysia, consider a KYC system that only requires a customer’s IC for locals.

Customer support – When customers require support, there is a good chance that they are feeling frustrated and would like immediate assistance. Therefore:

- Other than traditional options, include self-service mediums (such as chatbots), and

- Adopt up-and-coming social media channels to provide help

The right metrics to track CX success – As the customer onboarding process is shifting to digital, consider tracking the Onboarding Efficiency of your digital account opening system. A few measures to consider are:

- The abandonment rate against total onboarding attempts

- Time required to complete the digital self-service account opening process

Endnote

1Qualtrics (2022). 2022 Global Consumer Trends: What your customers need you to know for the year ahead. https://www.qualtrics.com/ebooks-guides/2022-cx-trends/

2Forrester (2021). Fear and confusion over data hinder retail banks’ ability to optimize customer experiences. https://www.kameleoon.com/sites/default/files/kam/Kameleoon_Banking_OSnap.pdf

3Temenos (2021). Digital bank of tomorrow: Part 2 Missing measures of digital success. https://www.temenos.com/insights/white-papers-reports/missing-measures-of-digital-success/.