Our top 10 takeaways

- There are 36 neobanks active today.

- ~ Neobanks acquired 350 million customers in 2021.

- Fino Payments Bank became the first neobank in APAC to go public and raised ~ US$150 Mn at ~ US$700 Mn valuation, reporting annual revenue of US$ 128.1 Mn.

- 3 out of the 6 payment banks are profitable, with an average net profit of US$ 3 Mn (2021).

- The highest funding by value for neobanks was recorded in 2021, reaching US$ 1.05 Bn.

- Razorpay and Open are two unicorn neobanks with a valuation of over a US$ 1 Bn.

- Most neobanks spearhead toward the growing millennial/Gen Z population.

- Sponsored banking license for neobanks limits their ability to establish a strong path to profitability.

- Neobanks have performed brilliantly in developing a comprehensive product suite across retail and SME customer journeys.

- Banking-as-a-Service (BaaS) is emerging as a significant growth opportunity for incumbents and neobanks.

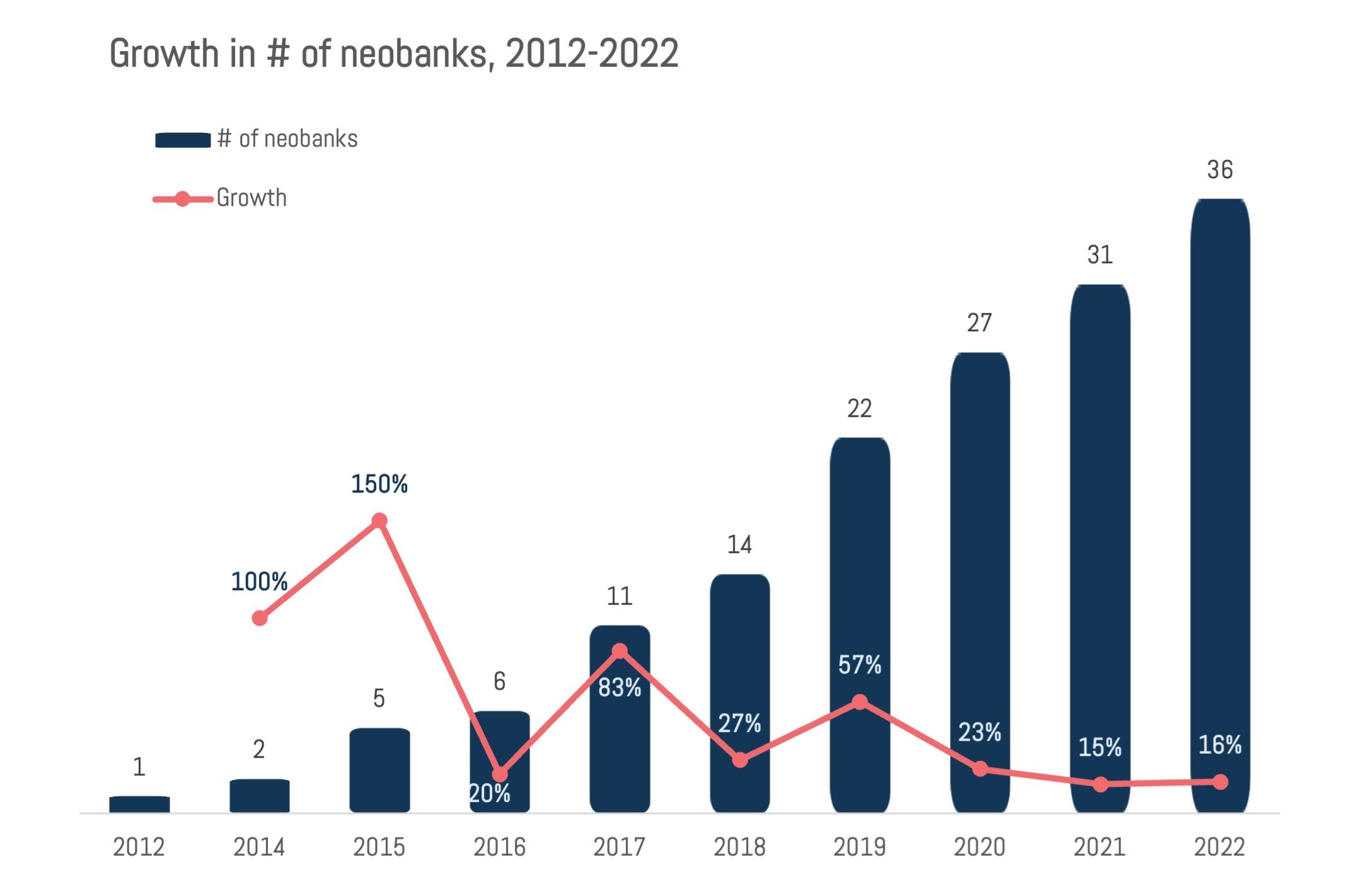

Over the last four years, 36 neobanks have been competing, acquiring customers, and creating a niche in the banking and financial sector. They are growing to 43% CAGR (Compound Annual Growth Rate), establishing a competitive ecosphere in digital banking (Figure 1). In 2021, we estimate that neobanks acquired 350 million customers, with 290 million out of the total customers coming in from 47% of the neobanks.

Figure 1: Growth of # of neobanks

Despite the ground-breaking success of neobanks, India’s significant hurdle is the lack of formal digital-only banking licenses. As a result, standalone digital banks and challenger banks do not exist in the country. At the heart of neobanks in India are sponsored banking licences, which serve to distinguish between the global and Indian neobanking models. Neobanks have partnered with traditional banks and private equity interests, fuelling the growth of India’s neobanking sector.

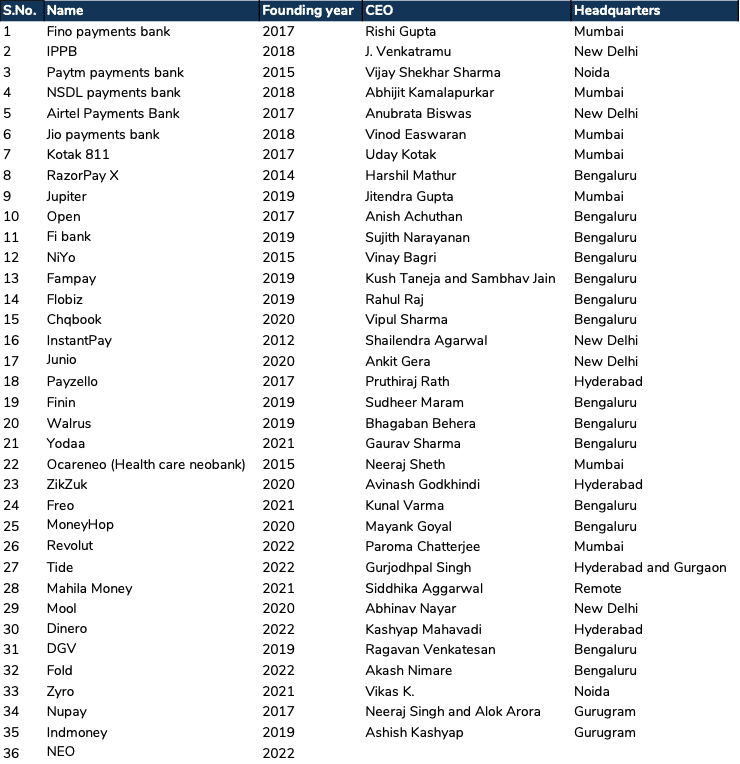

Table 1: Snapshot of Neobanks in India

Indian neobanks have just scratched the surface, setting the stage for explosive growth

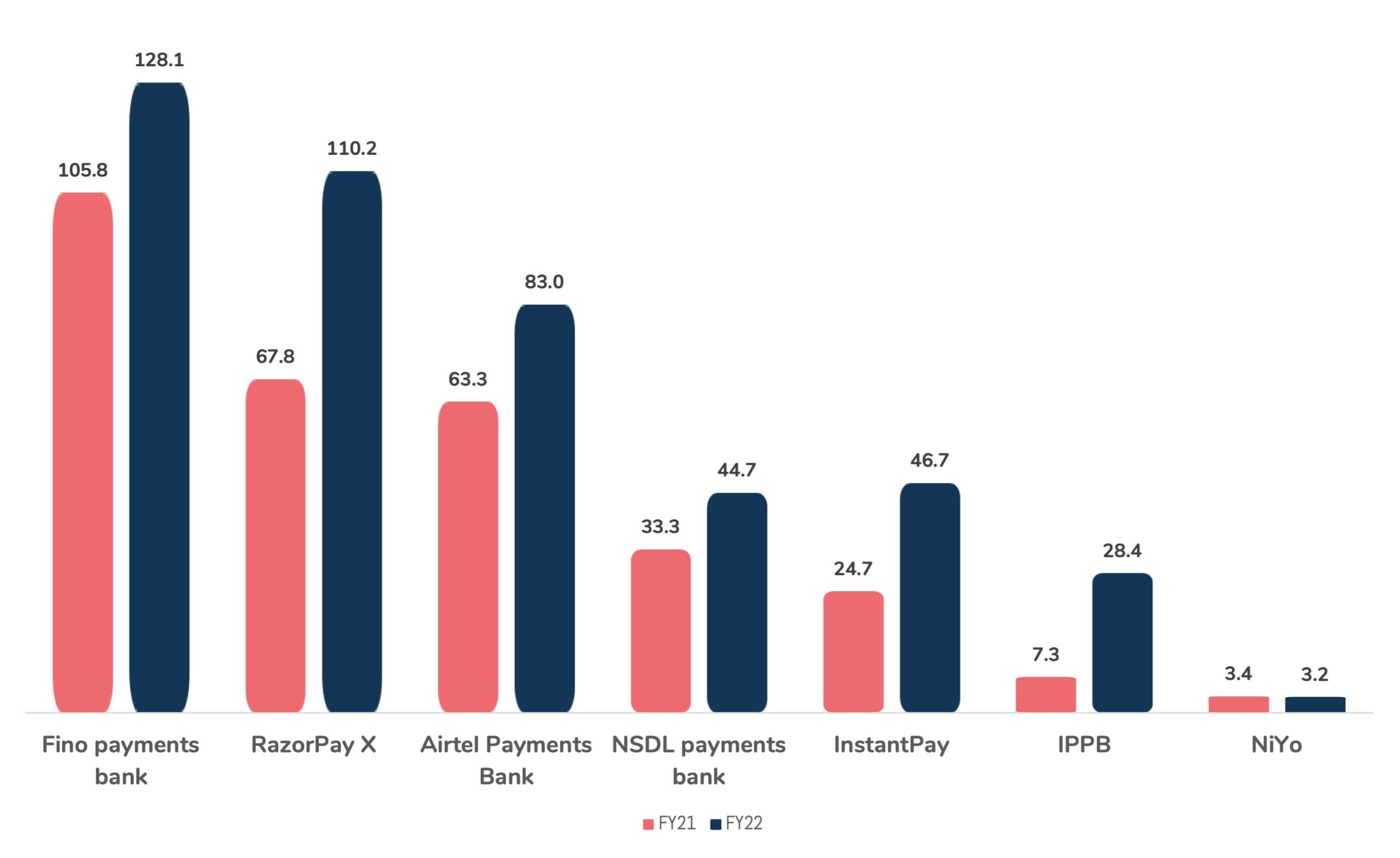

The payment banks buy a sizable disruption to reach the end-users. Nearly 30% of India is unbanked. Hence, payment banks and their last mile connectivity and correspondent networks aim to make banking and financial services available, even in the most remote locations. With their roots as digital banking interfaces, these payment banks have grown, becoming full-fledged, scheduled banks. Fino Payments Bank is a clear example, becoming the first APAC neobank to go public. It successfully raised US$150 Mn at a US$700 Mn valuation and reported annual revenue of US$ 128.1 Mn (2021).

Figure 2: Top 8 neobanks, operating revenue (Mn, USD)

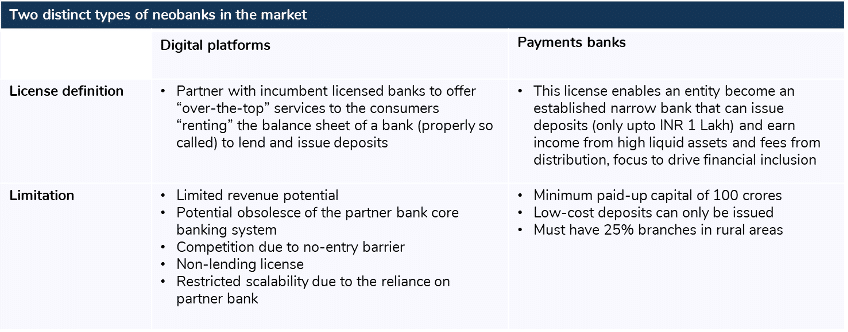

Profitability for neobanks still proves difficult for a majority of them. Most neobanks with a sponsored banking license do not fully own customer ownership and work on revenue-sharing models with incumbents (Table 2), resulting in paper-thin operating margins. Therefore, partnership revenues vigorously benefit these banks, netting positive cash flows. On the other hand, payment banks enjoy greater flexibility and autonomy.

The payment banks can also create a loan book with high CASA ratios, accelerating their revenue contribution. Payment banks report an average net profit of USD 3 Mn. Fino Payments Bank and Airtel Payments Bank earned the highest net profits in 2021, with US$ 2.73 Mn and US$ 5.8 Mn, respectively.

Table 2: Neobank classification based on license type

Note: 4 payment banks have now converted into scheduled banks that enable them to extend credit card facilities and lending services

A hotspot for investors

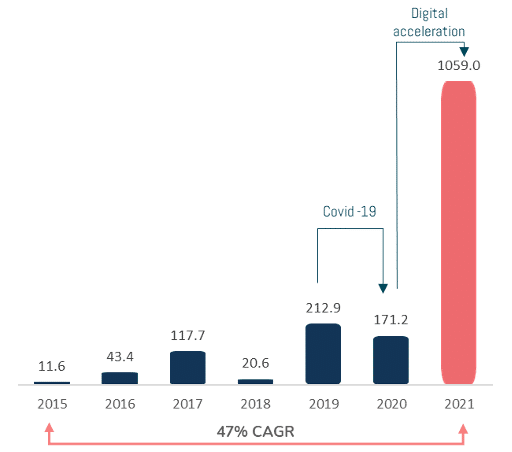

Neobanks can expect a substantial influx of funding to come. By far, the highest funding based on value was US$ 1.05 Bn in 2021 (Figure 3). The most funded neobanks include:

- Jupiter,

- Open Financial Technologies,

- Razorpay,

- Fino Payments Bank,

- and Niyo (Refer to the appendix for details on funding).

In the last 7 years, neobank growth measured approximately 47%, with a slight dip in 2020 and backed by an exponential rise in 2021.

Figure 3: Year-wise funding value (Mn, USD)

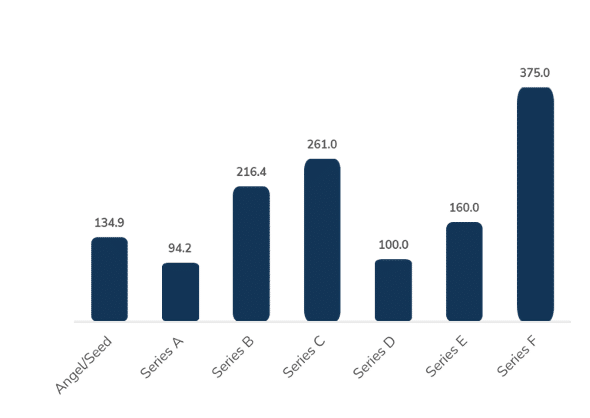

Based on each round, the maximum amount of funding (by value) flows in mid-rounds such as Series B and C. The same trend is observed in Series F at a more mature stage of the neobank (Figure 4). The funding amount coming from Series A-C is mainly used for building the core infrastructure, adding capabilities to the application, marketing and branding, and customer acquisition. Whereas, Series D and beyond work to expand teams as well as acquire related business to diversify and enhance the product portfolio. For example, Open acquired consumer neobank Finin for US$10 Mn to broaden its offerings and deepen relationships with banks.

Figure 4: Series-wise funding 2016 – 2021 (Mn, USD)

Note:

- USD 57.9M raised in Equity Rounds (2016,17) by Fino payments bank; not shown in series funding graph.

- Fino payments bank raised IPO USD 150M, not shown in the series funding graph

- Parent company Revolut has invested USD 45.5M a part of its first tranche of investments in its Indian arm, not shown in the series funding graph

- USD 296.6M worth of funding as unspecified venture capital rounds, not shown in the series funding graph

- Open raised USD 50M in its latest May funding round is not shown in series and total funding graph

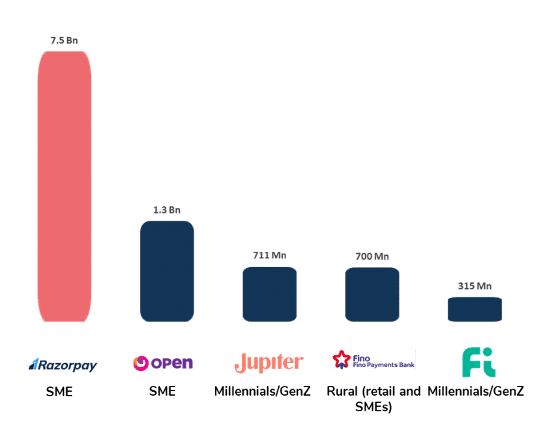

Razorpay and Open, with their aggressive funding strategies and rise in popularity among the Indian population, have become the two first unicorn neobanks with a valuation beyond US$ 1 Bn (Figure 5).

Figure 5: Top 5 neobanks by valuation. 2021 (USD)

Owning specific customer journeys is the way to sustainability

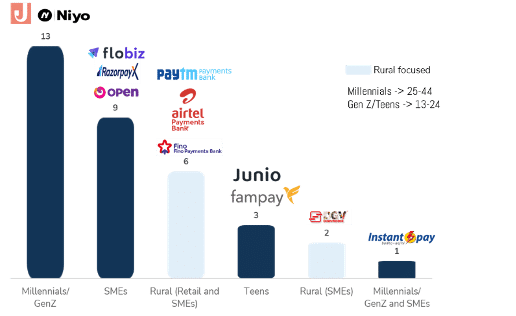

~55% of India’s population are millennials and GenZ population. For neobanks, this proves a large customer segment, brimming with potential for their sustainability – a hotpot. 13 out of the 36 neobanks cater to the young, digital-savvy population. It is because neobanks deliver a heightened customer experience centred on the following:

- Ease of onboarding

- Unique UI/UX

- Transaction feeds

- Personalised notifications

- Games and rewards

- Communities

India also houses 63 million SMEs, contributing approximately 29% of GDP. Supporting SME financing needs beyond current accounts and financing is a significant revenue opportunity for neobanks. The unbanked population stems as a result of;

- Inaccessibility,

- Necessary product suites being unavailable,

- Financial illiteracy and conservatism.

To combat this, all 6 payment banks gear toward financial inclusion. In addition, specialised neobanks exist to manage specific customer categories such as women entrepreneurs, dairy farmers, and street vendors.

Figure 6: Neobank segmentation by customer type

The analysis excludes two neobanks, Dinero and Fold, as they are launched in 2022 and are yet to start operations

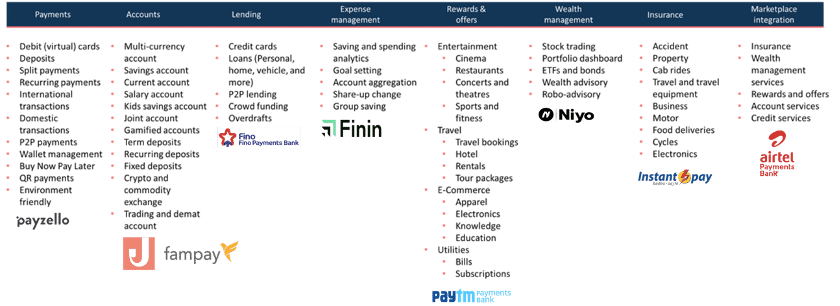

The overall product portfolio for neobanks is vast. They serve across 8-product stack categories. And over 60% of neobanks rely on deposit-taking and payment offerings with limited penetration in the lending market. While own lending products will be subject to regulatory approvals, aggregating them from leading lending institutions and bringing in “Buy Now Pay Later” (BNPL) capabilities is what neobanks are using as a product expansion strategy.

Figure 7: Mapping retail neobanks across 8-product stack categories (illustrative)

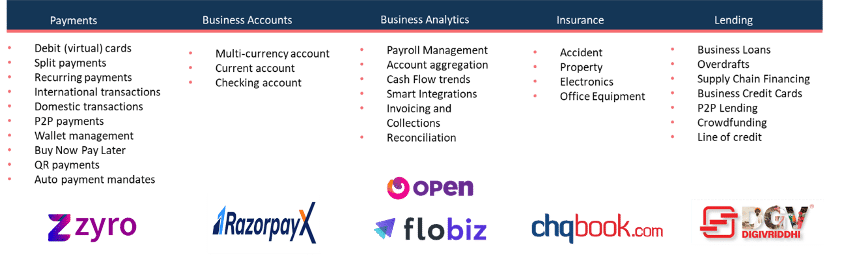

Also, most SME-focused neobanks help merchant owners gain access to more working capital and trade finance through their digital lending partners. They also assist SMEs with;

- business analytics tools,

- cash flow management,

- reconciliation,

- and invoicing.

For example, Digivriddhi (DGV) is a neobank dedicated to creating financing channels for dairy farmers. DGV established communities to enable dairy farmers to gain more knowledge and generate easy access to cattle loans, cattle insurance, and productivity enhancement tools.

Figure 8: Product stack for SME neobanks (illustrative)

Market drivers for neobanks In India

These 6 key drivers fill the gaps of conventional banking and usher in a new age for digital platforms to improve the customer’s life. Among these 6 key drivers, financial inclusion, open banking technology and data monetisation have matured in India.

- Financial inclusion

- Access to multiple financial products and services at a low cost

- Avenue to seek financial credit based on personal need and capability

- Generate annualised interest income over and above the core means to earn money

- Regulatory initiatives

- Create a favourable environment for entities to establish and operate digital banks in the country

- Bring stability and economic prosperity by promoting the creation of jobs in IT, banking, and fintech domains

- Open banking technology

- Allow ease of data sharing with third-party providers to build an efficient banking marketplace

- Enable financial service providers (insurance, wealth) to attach their services to the core banking products

- Data monetisation

- Use population data based on social media presence, e-commerce activity, and payments/remittances to build personalised products

- Integrate centralised databases with banking interface for secure and accurate customer remediation

- Non-traditional competitors

- Low to no-entry barriers for non-banking players to establish a digital bank

- Influx of telecom, big techs, and fintech companies in the banking and financial service industry

- Create a stiff competitive marketplace driven by product innovation and customer experience

- Cloud technology

- Enable divestiture from monolithic legacy infrastructure to agile, scalable platforms

- Allow quick and secure access to the core banking platform’s backend and frontend interface

Neobanks are thriving on partner ecosystems

Banking as a service (BaaS) is now a strong revenue strategy for incumbents, who are white labelling their financial solutions. Meanwhile, neobanks are building products and services over these solutions with a strong revenue strategy based on freemium, fee-based, and revenue from third-party merchant partnerships.

The sponsored traditional banking license allows the neobank to open accounts, establish UPI and QR-based payment channels, and accept deposits. To further enrich the product portfolio, they rely on strategic partnerships with Insurance and lending companies. For example, its top insurance partners are Bharati AXA, Tata AIA, Aviva, Birla Sun Life, Punjab National Bank, Kotak Life Insurance, ICICI Prudential Life Insurance, and Bajaj Allianz.

Table 3: Key traditional banking license partners

| Name | Banking partners |

| Fino payments bank | Wholly owned subsidiary of Fino Paytech |

| Paytm payments bank | Induslnd Bank , Suryoday Small Finance Bank (FD) |

| NSDL payments bank | Wholly owned subsidiary of NSDL |

| Airtel Payments Bank | 80-20 partnership between Bharti Airtel Banking and Kotak Mahindra |

| Jio payments bank | 70-30 partnership between Reliance Industries and SBI |

| Kotak 811 | Digital spinoff of Kotak Mahindra Bank |

| RazorPay X | RBL Bank |

| Jupiter | Federal Bank, NPCI |

| Open | Axis Bank, Yes Bank, ICICI Bank, SBM Bank, Equitas Small Finance Bank, Kotak Mahindra Bank, NPCI |

| Fi bank | Federal Bank |

| NiYo | Niyo Retail Savings Account – Equitas Small Finance Bank Niyo Global Account – DCB, SBM Bank Niyo Bharat Salary account – ICICI, Yes Bank, and DCB Bank |

| Fampay | IDFC FIRST Bank |

| Chqbook | ICICI Bank |

| InstantPay | ICICI Bank, Axis Bank, Induslnd Bank and Yes Bank |

| Junio | RBL Bank |

| Payzello | Laxmi Vilas bank and Yes bank |

| Finin | SBM Bank |

| Walrus | RBL Bank |

| Yodaa | Owned By Atlantis |

| ocareneo (Health care neobank) | Decentro, Yes Bank |

| ZikZuk | HSBC, Development Bank of Singapore, ICICI bank, YesBank, IndusInd bank |

| Freo | Equitas Small Finance Bank |

| MoneyHop | SBM Bank |

| Tide | RBL Bank |

| DGV | Federal Bank |

| Zyro | ICICI, RBL, HDFC |

| Nupay | IndusInd Bank and Yes Bank |

| Indmoney | SBM Bank |

Appendix

Regulatory framework

We have covered the regulatory neobank environment in our previous article. Please find the link in the card below:

India, the new hub of neobanks

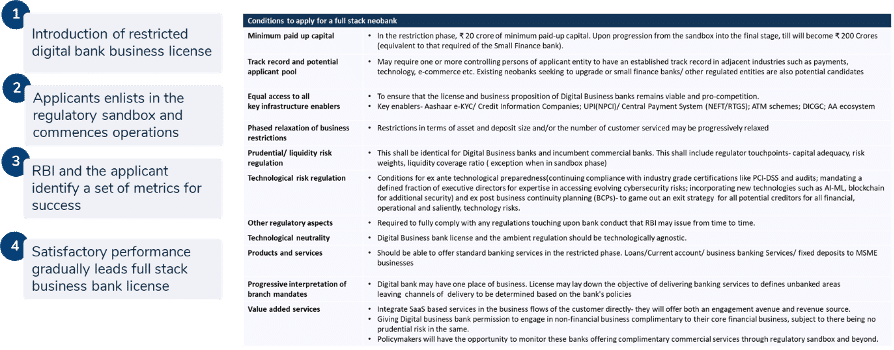

Beyond the coverage in our previous article, Neeti Aayog came up with a draft licensing policy that will allow RBI to grant digital banking licenses. This policy is still under review, and we expect a formal policy to be released end of this year.

Figure 9: Draft regulatory proposal for licensing neobanks

Detailed funding rounds for each neobank

| Name | Round | Year | Amount | Total funds raised |

| Fino payments bank | Equity round 1 | 2016 | USD 37.6M | USD 1.3B |

| Equity round 2 | 2017 | USD 20.3M | ||

| Equity round 3 | 2021 | USD 72M |

| Name | Round | Year | Amount | Total funds raised |

| Paytm payments bank | Funding round | 2017 | USD 37.6M | USD 1.3B |

| Venture round | 2017 | USD 20.3M | ||

| Venture round | 2021 | USD 72M |

| Name | Round | Year | Amount | Total funds raised |

| Airtel payments bank | Initial investment | 2020 | USD 29M | USD 29M |

| Name | Round | Year | Amount | Total funds raised |

| NiYo | Seed capital | 2016 | USD 1.15M | |

| Series A | 2018 | USD 13.2M | ||

| Series B | 2019 | USD 35M | ||

| Corporate Round | 2020 | USD 6M | USD 55.35M |

| Name | Round | Year | Amount | Total funds raised |

| Open | Seed capital | 2018 | USD 2.4M | |

| Series A | 2018 | USD 5M | ||

| Series B | 2019 | USD 30M | ||

| Series | 2021 | USD 100M | 137M |

| Name | Round | Year | Amount | Total funds raised |

| Razorpay | Seed capital | 2015 | USD 2.6M | |

| Series A | 2015 | USD 9M | ||

| Venture Capital 1 | 2016 | USD 100K | ||

| Series B | 2019 | USD 20M | ||

| Series C | 2019 | USD 75M | ||

| Venture capital 2 | 2019 | USD 28M | ||

| Series D | 2020 | USD 100M | ||

| Series E | 2021 | USD 16M | ||

| Series F | 2021 | USD 375M | 769.7M |

| Name | Round | Year | Amount | Total funds raised |

| InstantPay | Seed capital | 2016 | USD 4.6M | USD 4.6M |

| Name | Round | Year | Amount | Total funds raised |

| Jupiter | Seed capital | 2019 | USD 24M | |

| Venture capital | 2020 | USD 2M | ||

| Series A | 2020 | undisclosed | ||

| Series B | 2021 | USD 45M | ||

| Series C | 2021 | USD 86M | USD 155M |

| Name | Round | Year | Amount | Total funds raised |

| Fi | Seed Capital | 2020 | USD 13.2M | |

| Series A | 2021 | USD 12M | ||

| Series B | 2021 | USD 50M | USD 75.2M |

| Name | Round | Year | Amount | Total funds raised |

| Fampay | Pre seed | 2019 | USD 150K | |

| Pre seed | 2020 | USD 4.7M | ||

| Series A | 2021 | USD 38M | USD 42.9M |

| Name | Round | Year | Amount | Total funds raised |

| FloBiz | Seed round | 2019 | undisclosed | |

| Series A | 2020 | USD 10M | ||

| Series B | 2021 | USD 31M | USD 41M |

| Name | Round | Year | Amount | Total funds raised |

| Chqbook | Seed round | 2017 | undisclosed | |

| Series A | 2020 | USD 5M | ||

| Debt Financing | 2021 | USD 1M | ||

| Pre-Series B | 2021 | USD 5M | USD 11M |

| Name | Round | Year | Amount | Total funds raised |

| Junio | Seed round | 2020 | USD 3M | |

| Seed round | 2021 | USD 669K | 3.6M |

| Name | Round | Year | Amount | Total funds raised |

| Walrus | Pre seed | 2020 | undisclosed |

| Name | Round | Year | Amount | Total funds raised |

| Nupay | Pre seed | 2020 | undisclosed |

| Name | Round | Year | Amount | Total funds raised |

| Kaleidofin | Seed Round | 2018 | USD 2.8M | |

| Series A | 2019 | USD 5.06M | ||

| Series B | 2022 | USD 9.8M | USD 17.9M |

| Name | Round | Year | Amount | Total funds raised |

| Zyro | Pre seed | 2020 | USD 20K | |

| USD 20K |

Key investors

| Company | Investors |

| Fino payments bank | Fully owned subsidiary of Fino Paytech; Bharat Petroleum, The Blackstone Group, Indian Bank, Union Bank of India, LIC, intel Capital, Corporation Bank |

| Paytm payments bank | Backed by Alibaba, Berkshire Hathaway and SoftBank. The investments of $140 million by Blackrock and $126 million by CPPIB are also the largest by institutional investors in an Indian IPO. Abu Dhabi Investment Authority, Dutch pension investment firm APG, City of New York, Texas Teachers Retirement, NPS Japan, University of Texas, NTUC Pension out of Singapore, University of Cambridge, UBS, Mirae Asset and Standard Life Aberdeen also participated in the anchor round |

| RazorPay X | TCV, Lone Pine Capital and Alkeon Capital, salesforce ventures, GIC, Sequoia Capital, Rbbit Capital, Tiger Global Mangement |

| Jupiter | Tiger Global, QED, Sequoia Capital India, 3one4 Capital , Matrix Partners, Nubank Global Founders Capital, Mirae Assets Venture, Addition Ventures, Tanglin VC, Greyhound, 314 Capital and Beenext. |

| Open | Unicorn India Ventures and Recruit Co. Ltd, Tiger Global, Temasek, Google , 3one4 capital |

| FI bank | Ribbit capital, Sequoia capital, Falcon Edge Capital and B Capital, Hillhouse capital |

| NiYo | Accel and Lightrock India, Prime Venture Partners, JS Capital and Beams Fintech Fund |

| Fampay | Pioneer Fund, Sequoia Capital India, Soma Capital, Venture Highway, Vladimir Tenev and Y Combinator, GREENOAKS, Rocketship.vc, General Catalyst, Elevation Capital, GFC |

| flobiz | Sequoia Capital, Elevation Capital, Greenoaks Capital, Beenext and Think Investments |

| Chqbook | Aavishkaar Venture Capital, Rajiv Dadlani Group, InnoVen Capital, YWC Venture Capital, |

| InstantPay | RB Investments and Kaleden Holdings |

| Junio | angel investor Cred founder Kunal Shah, BharatPe CEO Ashneer Grover and Policybazaar’s Yashish Dahiya |

| Payzello | jiogennext, axilor accelerator, iii consulting |

| Finin | Angellist, Astir ventures, Unicorn India Ventures, pointone |

| Walrus | RAGHUNANDAN G, Better Capital, Y combinator, Raveen Aastry, Brijesh Thakkar |

| DGV | Infoedge ventures, omnivores |

| Nupay | Venture Catalysts, Navin Puri and ValueFirst founder and CEO Vishwadeep |

| kaliedofin | Oikocredit, Silicon-based venture capital firm Flourish, impact investment firm Omidyar Network India, Blume Ventures, angel investor Shlomo Ben-Haim and the Bharat Inclusion Seed Fund |