Key highlights

- Net revenues of the top 9 Malaysian banks declined by 1.6%, going from USD 19.2 billion in FY-2022 to USD 18.9 billion in FY-2023.

- Average net revenues declined by 1.6% from USD 2.13 billion to USD 2.09 billion.

- Net interest income declined by 6.1% from USD 14.7 billion to USD 13.8 billion.

- Non-interest income increased by 21.1% from USD 4.2 billion to USD 5.1 billion.

- Fee income grew by 3.6% from USD 2.3 billion in FY-2022 to USD 2.4 billion in FY-2023.

- Alliance Bank reported the highest increase in its fee income at 13.4%.

- Net profit increased by 6% from USD 6.9 billion in FY-2022 to 7.3 billion in FY-2023.

- All but Alliance, RHB and Affin Bank reported an increase in their net profits.

- Average NIM (net interest margin) declined by 25 basis points from 2.27% to 2.02%.

- Average NPL (non-performing loan) improved by 2 basis points from 1.58% to 1.56%.

- Average cost efficiency declined by 265 basis points from 46.46% to 49.12%.

- The loan portfolio of the top 9 banks increased by 7.4% from USD 451 billion to USD 484.6 billion.

- On the other hand, deposits grew by 7.5% from USD 490.5 billion to USD 527.1 billion.

Revenue highlights

Net revenues for the top 9 Malaysian banks declined by 1.6% YoY

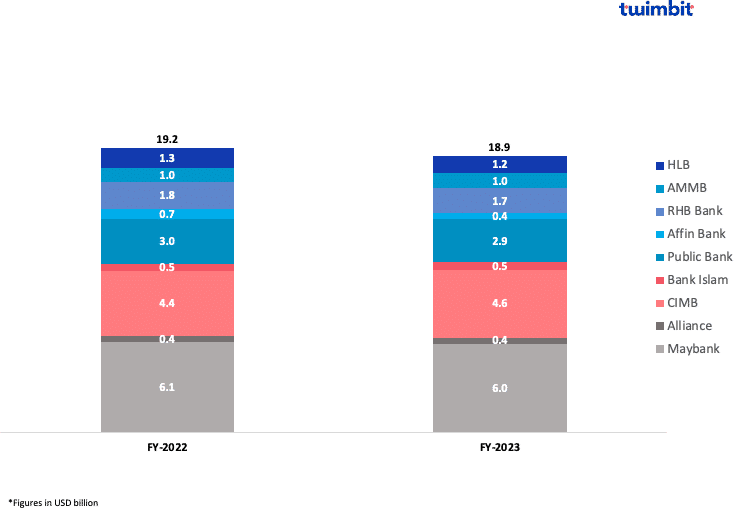

Net revenues declined from USD 19.2 billion in FY-2022 to USD 18.9 billion in FY-2023 (Exhibit 1). Average net revenues declined by 1.6% from USD 2.13 billion to USD 2.09 billion.

Exhibit 1: Net revenues of the top 9 Malaysian banks

- Alliance Bank, CIMB, and Bank Islam reported an increase of 3.7%, 5.9% and 7.2%, respectively

- Affin Bank, RHB, Maybank, HLB, AMMB, and Public Bank reported a decline of 39.8%, 6.5%, 0.9%, 4.7%, 1.4% and 2.6%, respectively

- Bank Islam

- Highest YoY growth at 7.2%

- Net revenues increased from USD 507 million in FY-2022 to USD 544 million in FY-2023

This growth was primarily driven by a 75.9% increase in its non-interest income from USD 51 million to USD 89 million. This was driven by:

- 2.3% increase in fees and commission income from USD 54.5 million to USD 55.7 million

- 214.5% increase in investment income from USD 4.4 million to USD 13.8 million

- 627% increase in foreign exchange income from USD (-3.2) million to USD 17.1 million

- 146.7% increase in unit trust income from USD (-5.4) million to USD 2.5 million

- Affin Bank

- Highest YoY decline at 39.8%

- Net revenues declined from USD 724 million in FY-2022 to USD 436 million in FY-2023.

This decline was primarily attributed to 2 key factors – net interest income and non-interest income.

- The highest decline of 19.5% in net interest income from USD 375.8 million in FY-2022 to USD 302.6 million in FY-2023

- 61.7% decline in non-interest income from USD 348 million in FY-2022 to USD 133 million in FY-2023

- 41.4% decline in net fee and commission income from USD 93.8 million to USD 55 million

- 82.8% decline in other income from USD 240.6 million to USD 41.4 million

- Partially offset by a 170.3% increase in net gains on financial instruments from USD 13.7 million to USD 36.9 million

Profitability

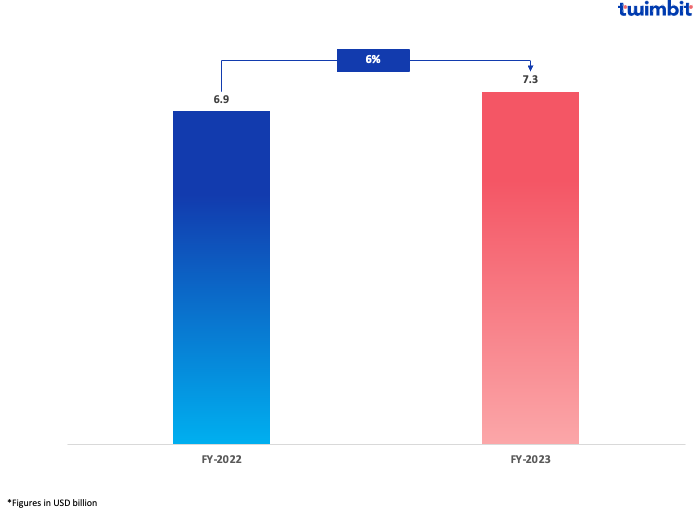

Net profits for the top 9 Malaysian banks grew by 6% YoY

Net profits increased from USD 6.9 billion in FY-2022 to USD 7.3 billion in FY-2023 (Exhibit 2).

Exhibit 2: Aggregated net profits of the top 9 Malaysian banks

- Maybank – net profits grew by 13.5%

- CIMB – net profits grew by 12.5%

- Bank Islam – net profits grew by 12.5%

- AMMB – net profits grew by 10.6%

- Public Bank – net profits grew by 8.7%

- HLB – net profits grew by 5.3%

- Alliance Bank – net profits declined by 1.2%

- RHB – net profits declined by 5.4%

- Affin Bank – net profits declined by 66.6%

All but Alliance, RHB and Affin Bank reported an increase in their net profits.

Fee-based income

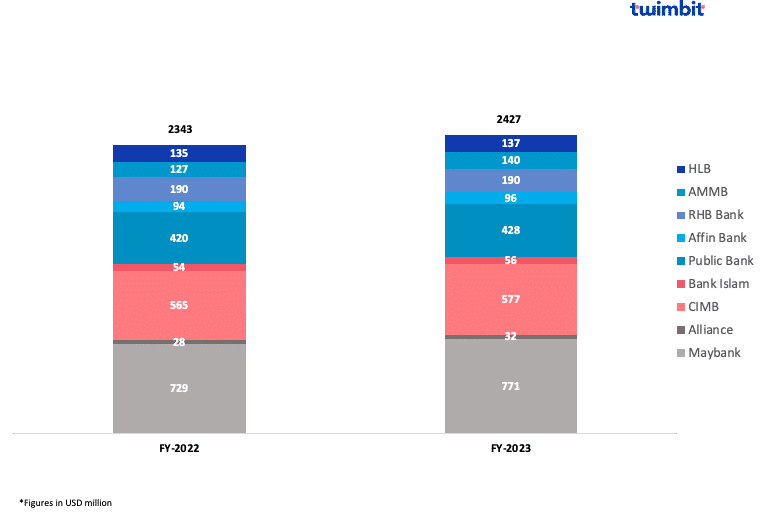

Fee income for the top 9 Malaysian banks grew by 3.6% YoY

The top 9 Malaysian banks witnessed a growth in fee income from USD 2.3 billion in FY-2022 to USD 2.4 billion in FY-2023 (Exhibit 3).

- Alliance Bank

The highest increase in fee income at 13.4% YoY, from USD 27.8 million in FY-2022 to USD 31.5 million in FY-2023. This growth was due to the following:

- 163.1% increase in the bank’s processing fees from USD 1.7 million in FY-2022 to USD 4.6 million in FY-2023

- 251.38% increase in the bank’s other fee income from USD 1.3 million to USD 4.6 million

- Other fee income constitutes income from wealth management, bancassurance fees, FX sales and trade fees.

- AMMB

The second highest growth in fee income was at 10.6%, from USD 126.5 million to USD 139.9 million. This growth was due to the following:

- 48.4% growth in corporate advisory income from USD 3.9 million in FY-2022 to USD 5.7 million in FY-2023

- 75% growth in bancassurance commission from USD 4.9 million to USD 8.6 million

- 16.5% growth in fees on loans and securities from USD 32.8 million to USD 38.2 million

Exhibit 3: Fee incomes of the top 9 Malaysian banks

Net interest margin (NIM)

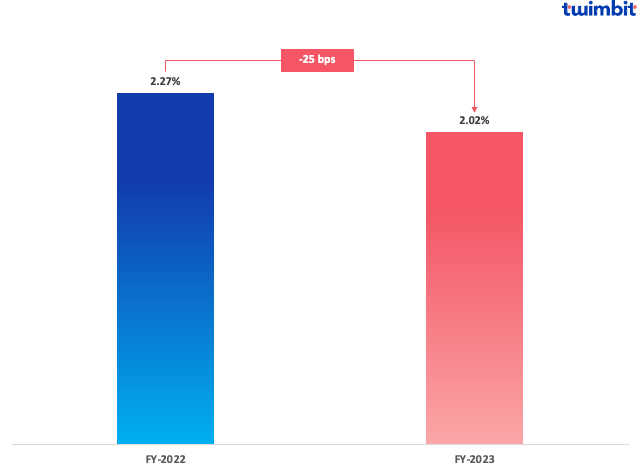

Average NIM declined by 25 basis points in FY-2023

The average NIM dropped from 2.27% in FY-2022 to 2.02% in FY-2023 (Exhibit 4). Malaysian banks tend to have lower NIM compared to the APAC average of 3.37% in FY-2023.

In FY-2023, all the banks reported a decline in their NIMs, with Affin Bank reporting the highest decline from 1.98% to 1.55%.

Malaysia’s NIM is anticipated to have bottomed out by the end of 2023 and will likely remain flat in 2024 due to slower loan growth.

Exhibit 4: Average net interest margin of the top 9 Malaysian banks

The declining NIMs in Malaysia are due to the following factors:

- Rising funding costs – 100 basis points have raised Malaysia’s overnight policy rate (OPR) from 2% to 3%. This has led to higher funding costs for banks, as they must pay more interest on deposits.

- Competition for deposits – Banks compete for deposits, especially in the current rising interest rate environment. This puts downward pressure on deposit rates, squeezing the banks’ margins.

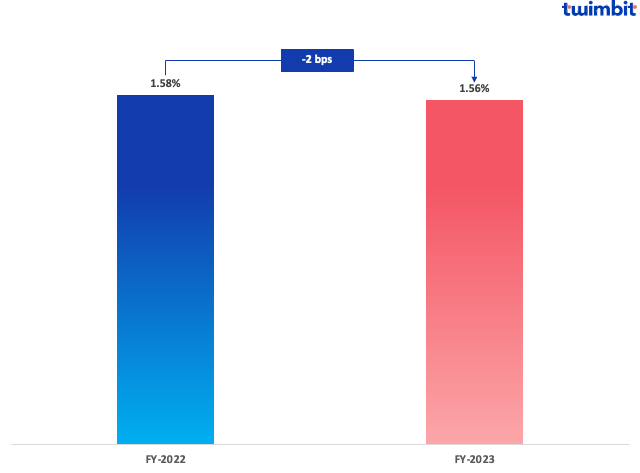

Non-performing loans (NPL)

Average NPL improved by 2 basis points in FY-2023

The top 9 banks in Malaysia reported a minute improvement in the average non-performing loans, from 1.58% in FY-2022 to 1.56% in FY-2023 (Exhibit 5).

Exhibit 5: Average non-performing loans of the top 9 Malaysian banks

- 5 of the 9 Malaysian banks analysed reported declining NPLs

- Maybank reported the highest NPL decline at 18.8%, from 1.37% in FY-2022 to 1.12% in FY-2023

- Public Bank reported the highest NPL growth at 48.5%, from 0.33% in FY-2022 to 0.48% in FY-2023

HLB and RHB reported an increase of 13.8% and 8.3% respectively. However, their current NPLs are low at 0.56% and 1.69%.

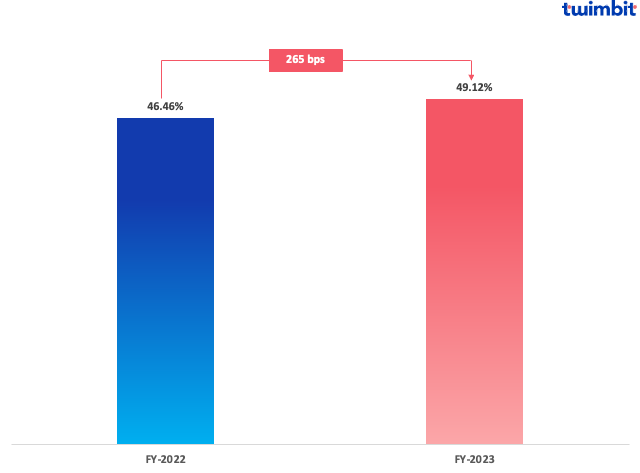

Cost efficiency (CE)

CE for the top 9 banks in Malaysia declined by 265 basis points between FY-2022 and FY-2023

The average cost efficiency for the top 9 banks in Malaysia stood at 49.12 % in FY-2023, up from 46.46% in FY-2022 (Exhibit 6). This indicates operational inefficiencies among these banks.

Exhibit 6: Average cost efficiency ratio of the top 9 Malaysian banks

All the banks analysed reported an increase in their cost efficiency. Affin Bank reported the highest increase of 944 basis points in its cost efficiency.

Bank Islam and Affin Bank reported a cost-efficiency ratio of 60.43% and 72.37%, respectively. All the other banks have their cost efficiency ratio below the threshold value, with Public Bank leading with an impressive ratio of 33.55%.

This lack of operational efficiency could stem from the compressions in net interest margins, resulting in elevated cost-efficiency ratios for these banks.

Outlook for 2024

In the first half of 2024, the banking sector’s outlook is subdued, with profit growth expected at a slower 5% pace. This is attributed to slowing non-interest income growth, marginal net interest margin recovery, and the absence of non-cash charge write-backs. However, favourable domestic economic conditions like low unemployment and stable growth aim to bolster asset quality and reduce NPLs (non-performing loans).

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- The financial year ending for AMMB and Alliance Bank in March (meaning Q4 of these banks is equivalent to the period of January to March of the year).

- The financial year ending for HLB is June (meaning Q4 of this bank is equivalent to the period of April to June of the year.

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to December 2023. The current conversion rate is 1 USD = 0.2195 MYR.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for the top 9 banks in Malaysia.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

To know how the top banks in Australia performed in FY-2023, click here.

To know how the top banks in Thailand performed in FY-2023, click here.

To know how the top banks in South Korea performed in FY-2023, click here.

To know how the top banks in Singapore performed in FY-2023, click here.

To know how the top banks in Indonesia performed in FY-2023, click here.

To know how the top banks in the Philippines performed in FY-2023, click here.