Key highlights

- Net revenues of the top 4 banks in the Philippines grew by 21.7% from USD 9.1 billion in FY-2022 to USD 11 billion in FY-2023.

- Average net revenues increased from USD 2.3 billion to USD 2.8 billion.

- Net interest income increased by 24.8% from USD 6.5 billion to USD 8.1 billion.

- Non-interest income increased by 14% from USD 2.6 billion to USD 3 billion.

- Fee income grew by 8.9% from USD 1.8 billion USD in FY-2022 to USD 1.9 billion in FY-2023.

- Union Bank reported the highest increase in its fee income at 34.2% from USD 210.4 million in FY-2022 to USD 282.3 million in FY-2023.

- Net profit increased 24.2% from USD 2.6 billion in FY-2022 to 3.2 billion in FY-2023.

- All but Union Bank reported double-digit growth in their net profits.

- Average net interest margin increased by 53 basis points from 3.98% to 4.51%.

- Average non-performing loans improved by 3 basis points from 2.77% to 2.74%.

- Average cost efficiency improved by 1 basis point from 55.62% to 55.61%.

- The loan portfolio of the top 4 banks increased by 9.1% from USD 113.3 billion to USD 123.7 billion.

- On the other hand, deposits grew by 9.7% from USD 146.7 billion to USD 161 billion.

Revenue highlights

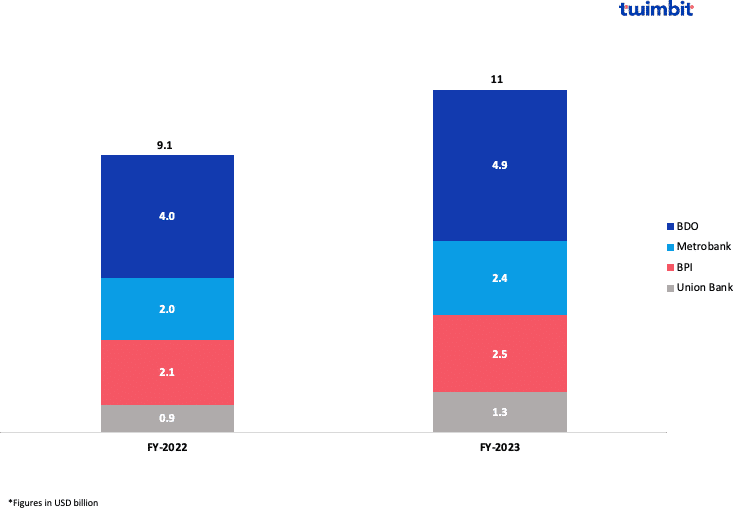

Net revenues for the top 4 banks in the Philippines grew by 21.7% in FY-20923 compared to FY-2022

Net revenues increased from USD 9.1 billion in FY-2022 to USD 11 billion in FY-2023 (Exhibit 1). Average net revenues stood at USD 2.8 billion in FY-2023.

Exhibit 1: Net revenues of the top 4 banks in the Philippines

Union Bank of the Philippines reported the highest YoY growth at 35.6%, increasing net revenues to USD 1.3 billion in FY-2023. This strong growth was attributed to the following factors:

- 33.7% increase in net interest income from USD 700 million to USD 935 million.

- 41.4% increase in non-interest income from USD 239 million to USD 338 million.

- The bank’s loan book expanded by 10.1% from USD 8.5 billion to USD 9.4 billion.

Despite being the smallest, Union Bank of the Philippines recorded the highest growth. It should be noted that all other banks also reported double-digit increases in their net revenues between FY-2022 and FY-2023.

- BPI – 16.6% increase

- Metrobank – 18.9% increase

- BDO – 22.5% increase

Profitability

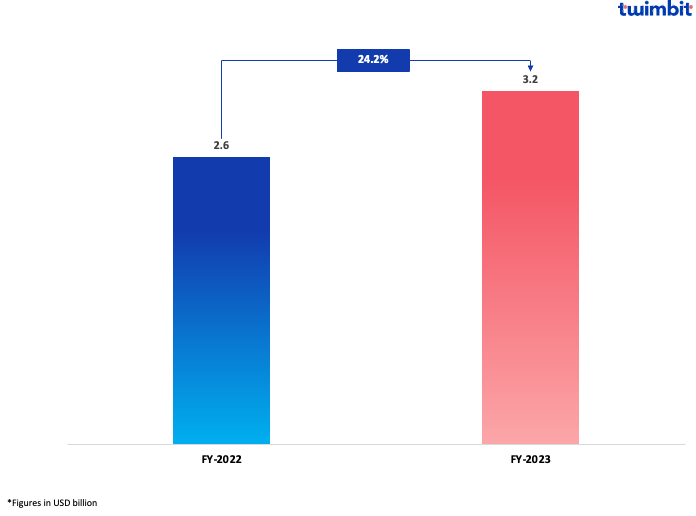

Net profits for the top 4 banks in the Philippines grew by 24.2% in FY-2023 compared to FY-2022

Aggregated net profits increased from USD 2.6 billion in FY-2022 to USD 3.2 billion in FY-2023 (Exhibit 2). Average net profits increased from USD 639 million in FY-2022 to USD 794 million in FY-2023.

Exhibit 2: Aggregated net profits of the top banks in the Philippines

- Metrobank – 29.4% net profit growth

- BDO – 28.5% net profit growth

- BPI – 30.1% net profit growth

- Union Bank – 27.6% net profit decline

Strong BPI net profit growth is driven by:

- 22.7% increase in the net interest income from USD 1.5 billion to USD 1.9 billion

- 1.5% increase in the non-interest income from USD 602 million to USD 611 million

The decline in net profits for Union Bank of the Philippines by 27.6% between FY-2022 and FY-2023 is due to the on-time integration cost of Citibank’s portfolio. Another factor is how Union Bank became the legal owner of Citibank’s consumer business on 1 August 2022. However, this resulted in increased costs associated with the integration till the end of the year.

Fee-based income

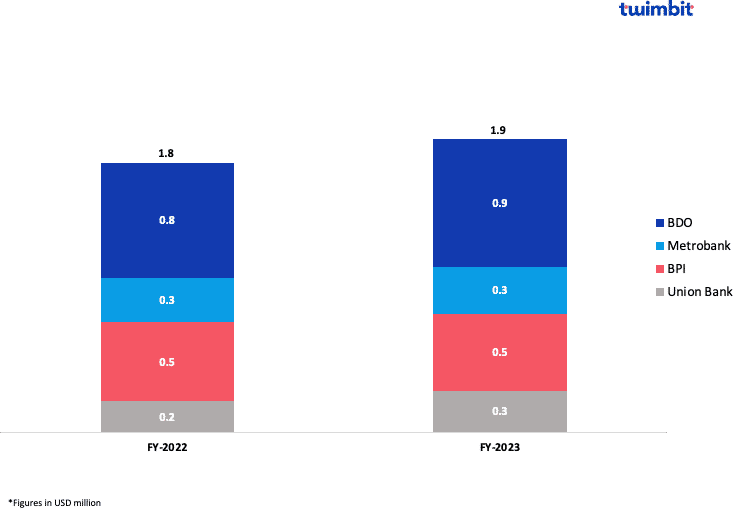

Fee income for the top 4 banks in the Philippines grew by 8.9% in FY-2023 compared to FY-2022

Philippines banks generate most of their fee income from traditional sources. Additionally, many cross-border remittances contribute to the overall fee income, such as the rise in Filipinos working in other Asian countries.

The top 4 banks in the Philippines grew their fee income from USD 1.8 billion in FY-2022 to USD 1.9 billion (Exhibit 3) in FY-2023.

Exhibit 3: Fee incomes of the top 4 banks in the Philippines

The recent popularity of credit cards has led to higher non-interest income growth among banks in the Philippines.

Union Bank of the Philippines reported the highest fee income increase at 34.2% (USD 282 million) between FY-2022 and FY-2023. This growth was due to:

- 48.5% increase in fees from parent customer transactions

- 38.5% increase in fees generated through trust, wealth management and bancassurance

BPI is the only bank analysed that reported a decline in its fee income by 3.1% from USD 534.1 million in FY-2022 to USD 517.8 million in FY-2023.

- Card fees generated 29.9% of the bank’s fee income and reported a 33% YoY growth.

- Wealth management comprised 16.1% of the bank’s fee income and reported a 6% YoY growth.

- Bank service charges comprised 10.1% of the bank’s fee income and reported an 18.1% YoY growth.

- Insurance comprised 9.7% of the bank’s fee income and reported the highest YoY growth at 43%.

Net interest margin (NIM)

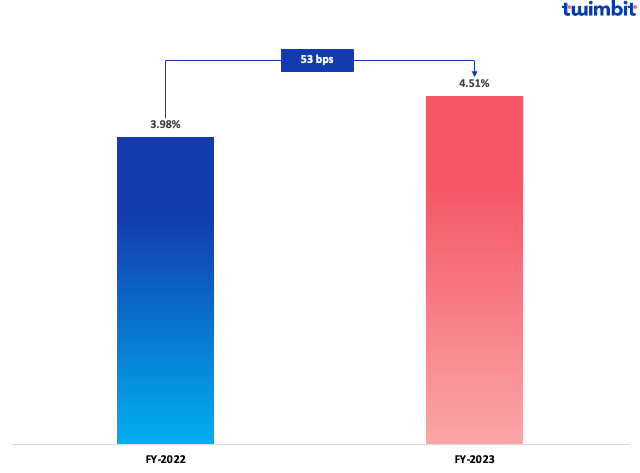

NIM for the top 4 banks in the Philippines increased by 53 basis points in FY-2023 compared to FY-2022

The average NIM increased by 53 basis points from 3.98% in FY-2022 to 4.51% in FY-2023 (Exhibit 4).

Exhibit 4: Average net interest margin of the top 4 banks in the Philippines

BDO reported the highest NIM increase at 63 basis points, from 4.05% to 4.68%. Meanwhile, Union Bank registered the highest NIM at 5.30%, up 53 basis points.

A key factor for these banks’ high NIMs is their high lending and low deposit rates. For instance, the Union Bank of the Philippines reported:

- 10.1% loan portfolio increase to USD 9.4 billion

- 13.5% deposit increase to USD 12.7 billion

- 74.18% loan-to-deposit ratio (LDR)

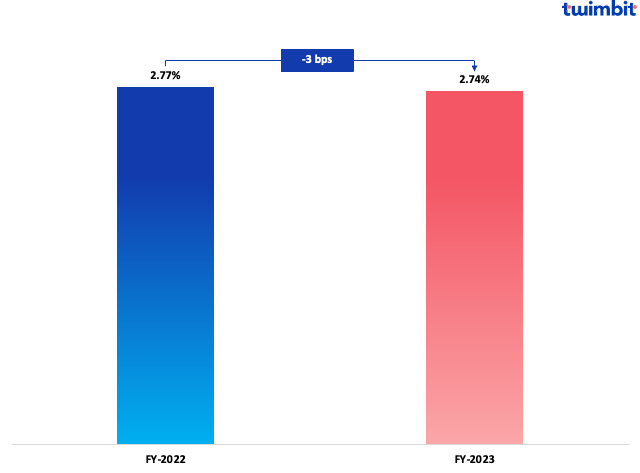

Non-performing loans (NPL)

NPL for the top 4 banks in the Philippines improved by 3 basis points in FY-2023 compared to FY-2022

The average NPL increased from 2.77% in FY-2022 to 2.74% in FY-2023 (Exhibit 5).

Exhibit 5: Average NPL of the top 4 banks in the Philippines

- Union Bank – 68 bps increase from 4.73% to 5.40%

- BPI – 14 bps decline from 2.02% to 1.88%

- Metrobank – 28 bps decline from 2.03% to 1.75%

- BDO – 38 bps decline from 2.32% to 1.94%

The average NPL level is high due to the high NPL of Union Bank, which is at 5.40%. Conversely, the NPLs for all other banks in the Philippines are below 2%.

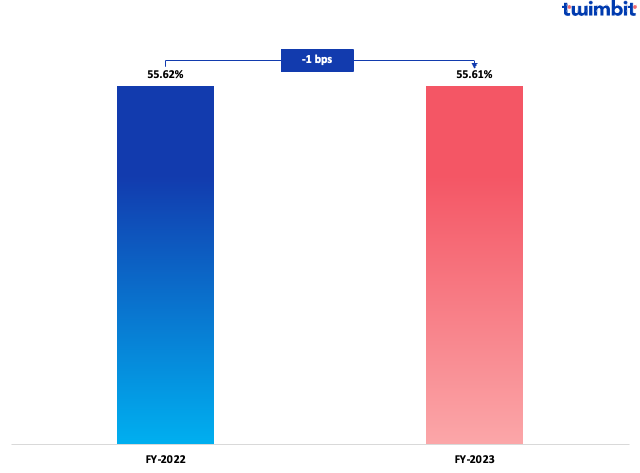

Cost efficiency (CE)

CE for the top 4 banks in the Philippines improved by 1 basis point in FY-2023 compared to FY-2022

Cost efficiency stood at 55.61% in FY-2023 (Exhibit 6), indicating operational inefficiencies. This is a minimal change, as the average cost efficiency in FY-2022 was 55.62%.

Exhibit 6: Average cost efficiency ratio of the top 4 banks in the Philippines

On an individual note, BPI, Metrobank and BDO reported improved cost efficiencies by 66 bps, 198 bps and 243 bps, respectively. However, only BPI has its cost efficiency below the threshold value of 50%.

Conversely, Union Bank reported a decline in cost efficiency from 58% in FY-2022 to 63% in FY-2023. This significant decline in the bank’s cost efficiency is due to the integration and one-off expenses associated with acquiring Citibank’s consumer business. Excluding the integration costs and one-offs, the cost efficiency was 56% in FY-2023.

Furthermore, the integration and one-off costs added USD 88.1 million to the bank’s operating expenses and accounted for 10.9% of these expenses.

Outlook for 2024

With expected improvements in economic growth over the next two years, driven by further moderation of inflation, credit demand is forecasted to rise, particularly in the corporate sector, potentially reaching a growth rate of 10%-12%. The inflation at the end of December 2023 stood at 3.9%, with the year-to-date headline inflation rate of 6%.

Lower inflation and rate cuts are anticipated to support loan repayments in 2024, ensuring asset quality stability. Despite a minor uptick in NPLs in corporate loans and credit cards, overall asset quality remained robust in 2023, with credit costs approaching pre-pandemic levels. Banks maintain strong provisioning, with coverage ratios surpassing 100%.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to December 2023. The current conversion rate is 1 USD = 0.01798383 PHP.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for the top 4 banks.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

- The fee income is net of all fee-related expenses.

To know how the top banks in Australia performed in FY-2023, click here.

To know how the top banks in Thailand performed in FY-2023, click here.

To know how the top banks in South Korea performed in FY-2023, click here.

To know how the top banks in Singapore performed in FY-2023, click here.

To know how the top banks in Indonesia performed in FY-2023, click here.

To know how the top banks in Malaysia performed in FY-2023, click here.