Key highlights

- Indonesia’s GDP growth is to ease slightly to an average of 4.9% over 2024-2026 from 5% in 2023. Inflation is expected to be at 3.2% in 2024 compared to an average of 3.7% in 2023.

- Private consumption is anticipated to be the primary driver of growth in 2024. Business investment and public spending are also expected to pick up due to reforms and new government projects.

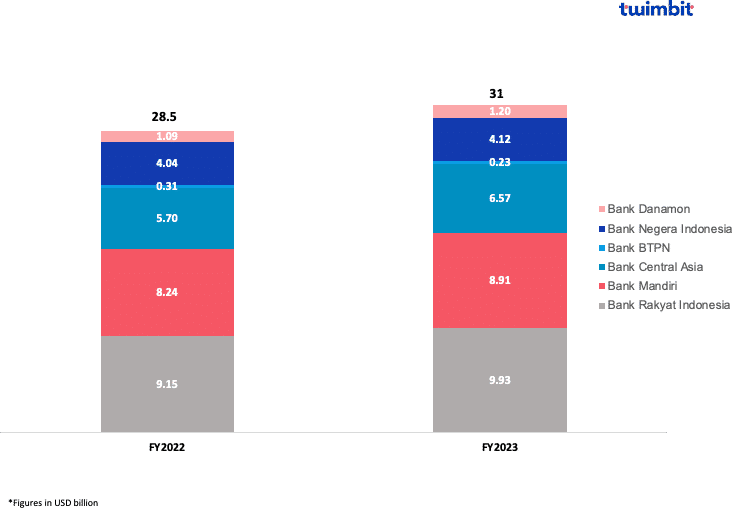

- The net revenues of the top 5 Indonesian banks grew by 8.5% from USD 28.5 billion in FY-2022 to USD 31 billion in FY-2023.

- The average net revenues increased from USD 4.8 billion to USD 5.2 billion.

- Net interest income increased by 9.1% from USD 22.6 billion to USD 24.6 billion.

- Non-interest income increased by 12.5% from USD 8 billion to USD 9 billion.

- Fee income grew by 7.5% from USD 4.5 billion in FY-2022 to USD 4.8 billion in FY-2023.

- Bank BTPN reported the highest fee income increase at 15.9%.

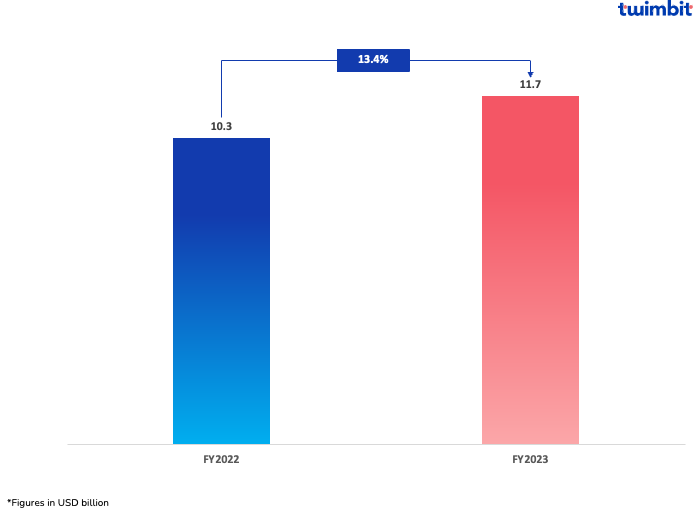

- Net profit increased by 13.4% from USD 1.7 billion in FY-2022 to 2 billion in FY-2023.

- All but Bank BTPN reported net profit growth.

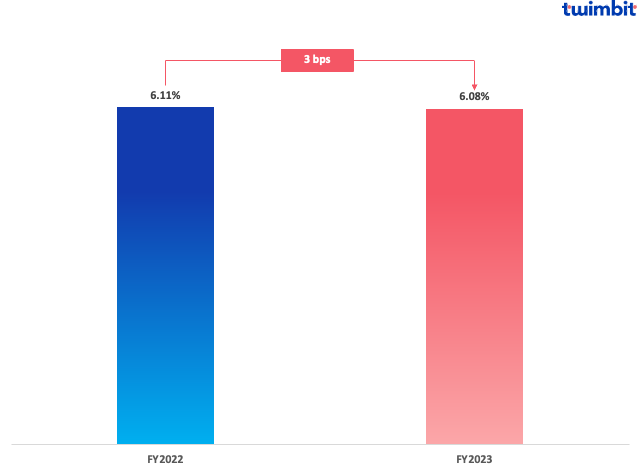

- The average net interest margins declined by 3 basis points from 6.11% to 6.08%.

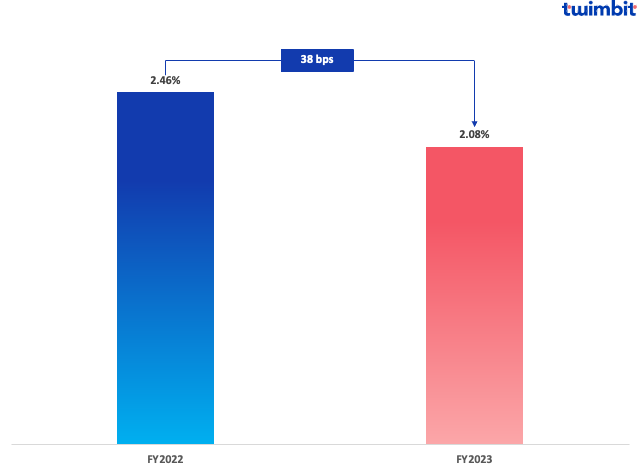

- The average non-performing loans declined by 38 basis points from 2.46% to 2.08%.

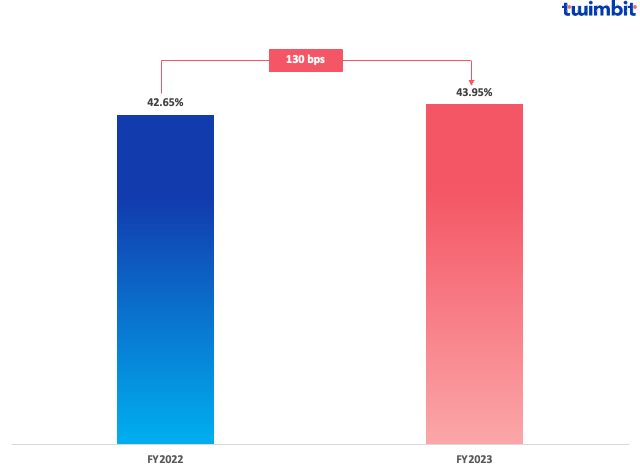

- The average cost efficiency declined by 130 basis points from 42.65% to 43.95%.

- The loan portfolio of the top 6 Indonesian banks expanded by 12.8% from USD 262 billion in FY-2022 to USD 296 billion in FY-2023.

- Deposits grew by 5.2% from USD 319 billion to USD 336 billion during the same period.

Revenue highlights

Net revenues for the top 5 Indonesian banks grew by 8.5% YoY

Net revenues grew from USD 28.5 billion in FY-2022 to USD 31 billion in FY-2023 (Exhibit 1).

- BCA

- The highest YOY growth in net revenues stood at 15.3% in FY-2023

- Net revenues increased from USD 5.7 billion in FY-2022 to USD 6.6 billion in FY-2023

- 17.6% increase in net interest income from USD 4.2 billion to USD 5 billion

- 5.3% increase in non-interest income from USD 1.5 billion to USD 1.6 billion

- 3.4% increase in fee income from USD 1.4 billion to USD 1.5 billion

- 45.4% increase in the trading income from USD 72.2 million to USD 105.1 million

- Loan portfolio of the bank increased by 13.9% from USD 46.7 billion to USD 53.2 billion

- BTPN

- The only bank that reported a decline in its net revenues despite a 2.6% increase in the net interest income and a 5% increase in the non-interest income

- Net revenues declined by 25.7% YoY from USD 305.9 million to USD 227.3 million

- The decline was due to a 5.6% increase in the bank’s operating expenses

- Led by a 10.4% increase in personnel expenses from USD 223.5 million to USD 246.7 million

- 65.7% increase in provision for impairment losses from USD 120.8 million to USD 200.3 million

Exhibit 1: Net revenues of the top 5 Indonesian banks

Profitability

Net profits for the top 5 Indonesian banks grew by 13.4% YoY to USD 11.7 billion

The top 5 Indonesian banks aggregated net profits from USD 10.3 billion in FY-2022 to USD 11.7 billion in FY-2023 (Exhibit 2). The top 3 – Bank Mandiri, BCA and BNI reported combined net profits of USD 7.8 billion (67% of overall net profits) in FY-2023.

- Bank Mandiri increased net profits by 20.4%

- BCA increased net profits by 19.3%

- BNI increased net profits by 14.2%

- BTPN reported a decline of 26.1% in net profits

In 2023, BTPN opted to boost its loan provisioning in line with its risk management strategy. This decision was made in anticipation of the conclusion of the POJK’s relaxation policy on credit restructuring by March 31, 2024. As a result of this supplementary provision, credit costs surged, impacting Bank BTPN’s net profit after taxes.

Exhibit 2: Aggregated net profits of the top 5 Indonesian banks

Fee-based income

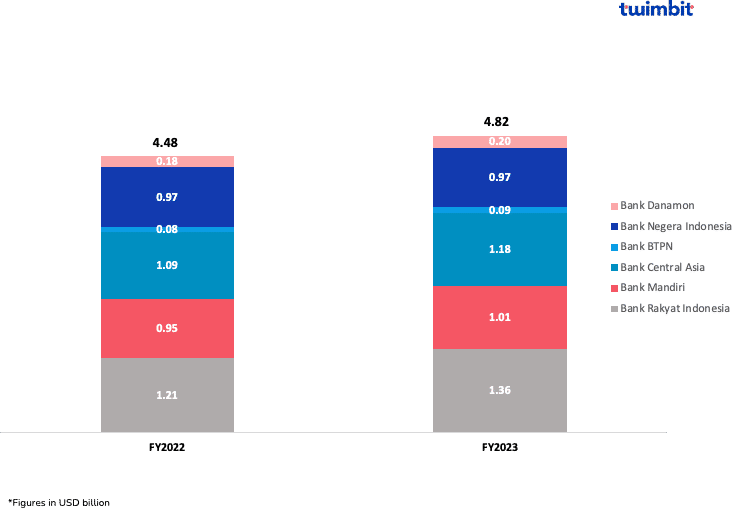

Fee income for the top 5 Indonesian banks grew by 7.5% to USD 4.8 billion in FY-2023 compared to FY-2022

- BTPN

- Highest growth at 15.9% YoY from USD 80.6 million in FY-2022 to USD 93.5 million in FY-2023, driven by:

- 40.2% increase in income from the recovery of written-off loans from USD 16 million to USD 22.4 million

- 44.1% increase in loan commission income from USD 12.7 million to USD 18.3 million

BRI reported the second-highest growth at 12.3%, from USD 1.2 billion to USD 1.4 billion.

Exhibit 3: Fee incomes of the top 5 banks in Indonesia

Overall, the top 5 banks in Indonesia have witnessed an increase in their fee incomes due to the following factors:

- Digital transformation – The shift to digital centricity continues to unlock new opportunities for banks to generate fee revenue. Banks can now charge fees for digital services, such as mobile banking transactions, online bill payments, and digital financial products.

- Growing middle class – Indonesia’s substantial and expanding middle-class population drives financial products and service demand, fuelling the need for financial offerings. This encompasses fee-generating products and services, such as credit cards, investment opportunities and insurance.

- Rising incomes – Rising income levels in Indonesia are driving fee income growth. This growth encourages higher-earning consumers to purchase more using credit cards and BNPL services. It also incentivises consumers to buy bancassurance and invest in wealth management. All of these services attract fees.

Net interest margin (NIM)

NIM declined by 3 basis points to 6.08% in FY-2023

- Bank Mandiri reported a 20 bps increase in its NIM to reach 5.44%

- Danamon reported a 15 bps increase in its NIM to reach 8.15%

- BRI reported an 86 bps increase in its NIM to reach 7.92%

- BCA reported a 25 bps increase in its NIM to reach 5.55%

- BNI reported an 11 bps decline in its NIM to reach 4.59%

- BTPN reported a 155 bps decline in its NIM to reach 4.80%

Exhibit 4: Average net interest margin of the top 5 Indonesian banks

Indonesian banks tend to have high NIMs when compared to other APAC regions due to the following factors:

- High loan rates – Indonesian banks charge higher interest rates on loans than banks in other countries due to the country’s high risk of default and high cost of funds.

- Low deposit rates – The large savings pool in the Indonesian banking sector gives banks more flexibility, as they do not need to compete as aggressively for deposits. This allows the banks in Indonesia to pay lower deposit rates than banks in other countries.

The difference between the high loan rates and low deposit rates in Indonesian banks has helped them best position to boost their margins.

Non-performing loans (NPL)

NPL for the top 5 Indonesian banks improved by 24 basis points in FY-2023, resulting in a current NPL of 2.22%

- NPL for Bank Mandiri improved by 79 bps YoY, from 2.31% in FY-2022 to 1.52% in FY-2023

- NPL for BNI improved by 70 bps YoY, from 3.13% in FY-2022 to 2.43% in FY-2023

Exhibit 5: Average NPL of the top 5 banks in Indonesia

Cost efficiency (CE)

CE for Indonesian banks declined by 130 basis points in FY-2023 compared to FY-2022

The average CE for the top 5 banks in Indonesia stood at 43.95% in FY-2023 (Exhibit 6). Compared to its APAC peers, Indonesian banks generally operate at better efficiency levels. However, it should be noted that these banks experienced better CE in FY-2022 when the average CE stood at 42.65%.

Exhibit 6: Average cost efficiency ratio of the top 5 banks in Indonesia

4 of the 6 banks analysed have CE ratios below the threshold value of 50%. However, BTPN and Danamon reported CE ratios of 52.70% and 54.73%, respectively, above the threshold value.

Outlook for 2024

Bank Indonesia (BI) is expected to maintain its key policy rate amid stable inflation and currency conditions. The first-rate cut is expected to come in Q3-2024, following consecutive months of inflation within the target range. Governor of BI, Perry Warjiyo, affirmed the policy rate would remain unchanged, aiming to sustain inflation within the 1.5%-3.5% target for 2024, with a potential cut as the next move, aligning with forecasts suggesting a 50 basis-point cut by Q3-2024.

Research methodology and assumptions

- Data collection has been done based on secondary research about the information provided by the respective banks through their investor presentation and quarterly financial statements. Twimbit follows the calendar year approach for the analysis in this report (meaning Q1 is equivalent to the period of January to March of the year).

- For fair representation and analysis, we have considered a constant currency rate for conversion from local currency to USD value. The USD conversion rate is the average calculated value from January to December 2023. The current conversion rate is 1 USD = 0.0000656666666666667 IDR.

- The report analyses net revenue, net profit and fee income, net interest margin, non-performing loan and cost efficiency for the top 6 banks.

- The revenue figures for all the banks analysed are net of interest and non-interest expenses.

To know how the top banks in Australia performed in FY-2023, click here.

To know how the top banks in Thailand performed in FY-2023, click here.

To know how the top banks in South Korea performed in FY-2023, click here.

To know how the top banks in Singapore performed in FY-2023, click here.

To know how the top banks in the Philippines performed in FY-2023, click here.

To know how the top banks in Malaysia performed in FY-2023, click here.